x 0 x 0

x 0 x 0

|

Every dog has its day - take comfort that it pays decent dividends at 5-6% yield despite profit decline and the net cash buffer of $3b+. Hopefully 1Q reports a decent operational update on y/y performance. I would love to see them continue with their share buyback which was undertaken previously when stock was trading below 70c pre ex d.

belugacat ( Date: 01-May-2026 14:09) Posted:

| Take dividend and run stock. Don' t fall in love with the stock. Like woman, always elusive. |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

The license is one of the causes but it was also the decline in profit in FY25 as the new installations were being relaunched and took time to ramp up so hopefully we can see the recovery in EPS from FY26 on a lower base. The positive was that GENS maintained the DPS at 4c for the year despite the profit decline and with a 5-6% yield supported by strong free cash flow generation and the net cash of > $3b, that will anchor share price as seen around the high 60s/low 70s. Just need the catalyst of recovering EPS from 1Q and the license renewal update in due course for the price to re-rate. MBS had the benefit of GENS downtime with the RWS 2.0 to capture more market share so relatively speaking, they outperformed but will be a matter of time for GENS to catch up and the dynamics to normalize. DYODD.

|

|

Good Post

Bad Post

|

x 0

x 0

|

Any followers of this stock at all? One of the few rare healthcare stocks that has a good growth story, > 80% gross margins and solid ROE of > 35% yet continues to trade under ipo price. Is market mispricing the stock or is it another case of good stock listed on the wrong exchange?

|

|

Good Post

Bad Post

|

x 1

x 0

|

Apart from A2B acquisition, not sure the other two acquisitions back in 2024 of CMAC and Addison Lee are driving the returns for the group. The y/y growth seen in 2025 is largely from the acquisitions so as we normalize growth with a higher baseline, how will that look like this year?

Guzman ( Date: 28-Apr-2026 19:56) Posted:

| Strong headwinds against CDG in 2026 (1) SBST Revenue will drop with handing over of Tampines package to new operator (2) VICOM profits will drop as OBU installation is near its end (3) Taxi fleet will continue its decline with mass contract renewal in May (4) Australian acquisition a2b is in trouble, not delivering as promised. All provisions made previously have been released. No more bullets left. DYODD..... Sell after XD! |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Market will want to know whats the special divs that will be given back to shareholders!

JurongW ( Date: 27-Apr-2026 19:51) Posted:

Most of the good news may have been priced in when share price gap up on 16 Apr due to the sale of olam agri to Salic, pending one more approval.

This piece of news just confirmed the completion of the sale. Upside maybe limited.

Let' s see if it can clear the resistance at 1.09 tomorrow.

trader1970 ( Date: 27-Apr-2026 19:08) Posted:

| Thanks. It should gap up tomorrow.. : |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Will we see dividend effect buy-in by insti funds ahead of ex d for 2c dividend on 30 Apr?

|

|

Good Post

Bad Post

|

x 0

x 0

|

Share price seems to have rebounded off lows of $1.30 to be slightly above IPO price. Anything interesting from the AGM for those who might have attended?

|

|

Good Post

Bad Post

|

x 0

x 0

|

Agreed. Not sure if many noted but they recently issued a $400m bond at 2.95% which will help lower the cost of debt for the outstanding debt stack. That will bring savings which will be eps accretive.

JurongW ( Date: 24-Apr-2026 22:07) Posted:

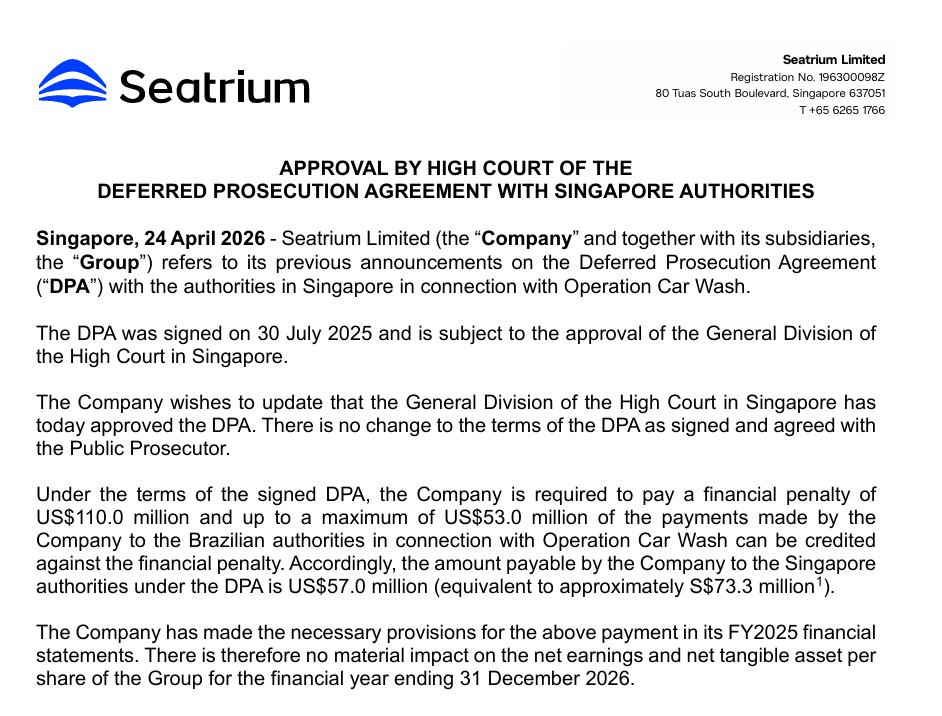

Yup, finally there is closure. The High Court really took a long time to approve the DPA.

The document must have run into thousands of pages for vetting before final approval.

n3wbie ( Date: 24-Apr-2026 20:09) Posted:

| Since the provision was made last year, guess no impact for FY26 and the read out is that the overhang is now finally cleared |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Since the provision was made last year, guess no impact for FY26 and the read out is that the overhang is now finally cleared?

JurongW ( Date: 24-Apr-2026 17:44) Posted:

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Thank you for sharing the TA. Based on the responses to shareholders questions ahead of AGM, it seems like the business had limited impact from the recent Iran war and if so, the current correction in share price is a good buy-on-dip opportunity. Look forward to what they share at AGM and also 1Q business update on 5 May.

JurongW ( Date: 21-Apr-2026 20:40) Posted:

I placed this counter under my watchlist as it caught my attention when Nicky Tan continue buying shares as well as share price hitting the previous bottom.

The recent bearish candlestick closed below the 5EMA, with share price testing critical support near ~1.30, further downside would be implied if that level breaks.

Today close at $1.40, up 9 cents, suggests smart money may be stepping in to catch the bottom.

The price is now kissing the upper channel, the key question is whether it can break past this resistance. Tomorrow price action will provide the answer.

n3wbie ( Date: 20-Apr-2026 22:20) Posted:

| Under watch list for a bull or bear setup |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

They are proposing a new share buyback mandate at upcoming AGM. Unfortunately have a conflict but would otherwise pressure them to support the share price given the growth prospects of the business since its trading 10% below IPO price now. That would be more meaningful ammunition to drive sustained re-rating than a director doing small purchases.

|

|

Good Post

Bad Post

|

x 0

x 0

|

Under watch list for a bull or bear setup?

JurongW ( Date: 20-Apr-2026 22:16) Posted:

Under watchlist

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Hitting all the buzzwords but isnt a 25% discount to last market close price quite a steep discount?

|

|

Good Post

Bad Post

|

x 0

x 0

|

Thanks for sharing! Saw that price broke above 70c today, was wondering if anything material or interesting being shared at today session.

Newbie2025 ( Date: 15-Apr-2026 15:28) Posted:

Sir, can spend it at Chaterbox, Foodmall etc

Eat full and wait for dividends..😂

JurongW ( Date: 15-Apr-2026 14:21) Posted:

I thought the practice of giving out cash vouchers had been stoppped at company AGMs

Genting is still rather generous in giving voucher. Are they supermarket vouchers |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Finally there is an update on dividend ex date on 30 Apr and payment of dividends on 26 May. Unable to join the AGM tomorrow, hopefully there are kind khakis able to share key highlights from boss Lim.

|

|

Good Post

Bad Post

|

x 0

x 0

|

DBS just published a note on this sleepy and overlooked stock -

Lodging powerhouse re-emerges

- Market under appreciating FEOR&rsquo s new 2030 framework to unlock value and focus on its asset light business

- Potential for divestment and unlocking of non-core SG properties to crystallise gross proceeds of up to SGD2.20/ share

- Vision to grow its lodging platforms by > 50% from 72k beds to 110k beds by 2030 will reinvent its earnings profile from an asset heavy one (c.2 &ndash 2.5% asset yield) to asset light platforms (c.8 &ndash 10% ROE)

- Our SOTP analysis shows a fair valuation of SGD2.00 / share at a c.30% discount to RNAV, implying upside of c.68%

The Business

Lodging operator within &lsquo essential&rsquo lodging sectors. Far East Orchard Limited (FEOR) is a Singapore-listed lodging platform focused on long-stay accommodation, with core capabilities spanning PBSA investment, hospitality management and fund management. Backed by Far East Organization (c.63.6% stake), FEOR is the only fully vertically integrated lodging platform on the SGX, capturing value across the entire lifecycle from asset origination to management and eventual exit, with exposure to structurally resilient &ldquo essential&rdquo lodging segments.

The Stock

Transformation into an asset light operating model Exit of non-core SG assets to crystallise up to SGD 2.2/share (gross). Deep value counter with fair value of SGD2.00 / share. We see a glide-path towards its 2030 vision with the group executing a decisive pivot towards an asset-light model, anchored by the potential divestment of c.SGD1.1bn of non-core Singapore assets (c.SGD2.20/share, gross) in the immediate term. This should unlock value and provide dry powder for reinvestment. Under its 2030 framework, the group targets > 50% growth in PBSA beds (from c.72k to 110k), scaling its fee-based operating and fund management platform. This transition is set to structurally enhance returns, shifting earnings from low-yielding asset ownership (c.2&ndash 2.5% returns) to higher-quality, capital-efficient income streams (c.8&ndash 10% ROE). We see a clear pathway for NAV gap closure, driven by asset monetisation, capital recycling and platform expansion, with our SOTP valuation of SGD2.00/share implying c.68 upside.

|

|

Good Post

Bad Post

|

x 0

x 0

|

For the patient capital, its fine, just sit and collect the divs of almost 6% at present. Good that the boss hasnt cut the DPS despite the drop in profits so this should provide downside protection. The catalyst is whenever they deliver the growth.

|

|

Good Post

Bad Post

|

x 0

x 0

|

Unfortunately havent seen any action since shareholders approved the share buyback. Boss doesnt think its undervalued or cheap enough yet?

For_The_Next_Leg ( Date: 06-Apr-2026 09:37) Posted:

Seems like the shares will run soon.

https://www.minichart.com.sg/2026/04/01/yangzijiang-maritime-development-ltd-egm-2026-share-buyback-mandate-approval-shareholder-qa-and-capital-management-insights/

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Given that they are now < 5%, the disclosures are under Temasek - not sure if anyone is aware of how many more shares that KEP has to divest?

JurongW ( Date: 06-Apr-2026 19:07) Posted:

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Anyone following this stock? Positive news with divestment of US$375m but market doesnt seem to react

https://www.theedgesingapore.com/news/ma/olam-sell-it-services-unit-wipro-us375-mil

|

|

Good Post

Bad Post

|