x 0 x 0

x 0 x 0

|

Citi wrote a note about 2025 being a year of non-gaming assets refresh and 2026 a year of gaming assets refresh so the earnings recovery will realistically be a 2027 play off 2-3 years of low base/

|

|

Good Post

Bad Post

|

x 0

x 0

|

The banks would typically sell it back to the issuing company or principals anyway unless they are underwriting the deal with their own balance sheet, which I doubt so

shk363 ( Date: 23-May-2026 17:26) Posted:

| stabilizing agents buying cheap... |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

It is Malaysia Genting not GENS.

https://mothership.sg/2026/05/singaporean-woman-reportedly-wins-record-jackpot-genting/

luckyguy3 ( Date: 23-May-2026 17:43) Posted:

| --- Post Removed by User --- |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

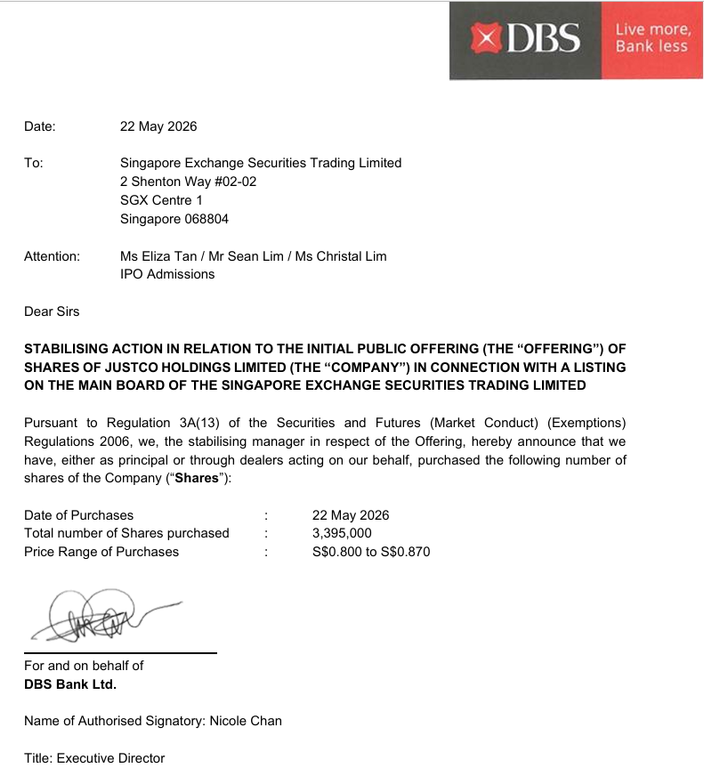

This is 60% of their allocated volume for stabilisation. Wonder the direction of travel from next week onwards...

JurongW ( Date: 22-May-2026 22:21) Posted:

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Should be Feb 2027 since the last renewal was done Feb 2025?

JurongW ( Date: 22-May-2026 17:12) Posted:

When will the existing license expire?

sgng123 ( Date: 22-May-2026 17:04) Posted:

| Wait for breakout news hope gov can fast paced casino licence renewal in 2h. |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Singtel sets the benchmark. Bought back 25.5m shares for ~$122m in one day. That is a blue chip flexing its muscles and showing how its done!

sgng123 ( Date: 21-May-2026 19:44) Posted:

| 4mil SBB today.

I wanna see those big SBB 10mil one. |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

This stock has nothing to do with AI, at least for now. They are trying to expand into a platform business in due course with this AI element but fundamentally, it is just selling ink/dye. They basically supply wholesale and dont need to export as able to have local suppliers hence decentralizing the model. My layman understanding of the model. Please correct me if im wrong!

dexterderc ( Date: 21-May-2026 15:54) Posted:

| Ultragreen.AI TP set by FIs is based on their claimant of using AI blah blah blah. But in actual fact, most of the revenue comes from sale of it's fluorescence dyes.. nothing to do with AI or what it claims.. unless they are able to sell their AI story.. this stock is better left alone for now.. |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Thanks for sharing. Disappointing stock since IPO. Have cornerstone investors also given up on the stock?

|

|

Good Post

Bad Post

|

x 0

x 0

|

The key difference is both are fundamentally different offerings - RWS is more of an " integrated resort" with all the significant capex on family-related offering with USS, Oceanarium, etc in addition to a casino. MBS is essentially a high-end shopping mall + casino. RWS probably deserves an " experience premium" but market only rewards or penalizes share price based on financials.

sgng123 ( Date: 21-May-2026 01:22) Posted:

Might be but currently it don make sense to see such a big difference between duopoly casinos.

We could only find what is different between the two.

Connectivity and casino licence duration.

plu MBS not listed so we don know their expense, impairment etc.

Physically visit both casino don find much difference, |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

A step in the right direction if they can do daily sbb to slowly support the share price but certainly they can buy more than $1m value!

JurongW ( Date: 20-May-2026 18:07) Posted:

SBB today - 1,469,200 shares bought at 58.5 to 59 ($866,932) |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

The DPS of 4c will provide a yield backstopper at some level. Current price is almost 7% yield - of course the caveat is while management had committed to defend it, it is not a dividend policy.

Checkerman ( Date: 20-May-2026 07:33) Posted:

Next 6 month will be gloomy for Genting.

Won?t be surprise to see price trading between 51-55

sgng123 ( Date: 19-May-2026 21:40) Posted:

Hit by bad sentiment over loss of market share due to shorter casino licence.

MBS also faced same thing in 2027, they need heavy capex to start work on 4th tower and if sg gov wanna push them just give a shorter licence.

the u see reversal of fortune loh. |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Pretty depressing for a blue chip to be hitting multi-year lows when STI is at ATH.

sgng123 ( Date: 19-May-2026 21:29) Posted:

Ttypical malaysian businessman tactic, everything cloak and dagger aka act blur till ask.

That why kanna 2 years licence, MBS proactive so get 3 years licence and market share.

That 2 years licence start the profit rot till now, losing high roll customers to MBS.

The connectivity issue partially solved in jul when new ccl stations link harbourfront and bayfront

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Honestly, they should be more commited with their capital returns strategy and announce a $x share buyback program - if it doesnt get fully utilized if and when the share price re-rates, that' s fine. It will deter shortists and show that the management and board are willing to put their capital to work that will be accretive for shareholders. The buyback program now feel haphazard and adhoc.

JurongW ( Date: 19-May-2026 18:34) Posted:

2,261,000 shares bought at 58.5 to 59.5 ($1,332,518)

sgng123 ( Date: 19-May-2026 18:13) Posted:

SBB 2.2mil today, need to wait till volume die down still quite a bit of shorting though not aggressive.

part and parcel of casino stock drama , it worse this year as casino licence renewal in 2026.

Everyone siam till coast is clear, hopefully genS get normal renewal till 2030 3 years licence.

Just don bother abt profit in 2026, would be profitable but sub par yty.

Enjoy ur dividend coming next tuesday. |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Previous announcement for the casino license renewal was in Nov 2024 for the 2 years renewal to take effect from Feb 2025. Doesnt seem from the AGM minutes that there are hint of when they are expected to hear back on the casino renewal timeline. Hopefully sooner rather than later to remove the overhang.

sgng123 ( Date: 19-May-2026 21:06) Posted:

Stock price go down to recession level hopefully might just be temp else big correction might be coming for overvalued sgx counters.

genS stock price heavily manipulated after the 2 years licence, casino market share basically tank.

This coming casino licence renewal in 2026 very imp hope no more surprise from sg gov.

Basically genS had done everything sg gov ask them to do, spent $2b alrdy and $4.8b following till 2030. |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Recalled when the stock first went underwater after IPO, the chairman bought some shares and it rebounded strongly. That is probably a stronger vote of confidence coming from chairman directly. Surprised that with their cash, and the share buyback mandate that they had secured at the AGM that they havent thought or done it yet. It is not just about share price support, it is investors confidence.

alexvar ( Date: 19-May-2026 04:56) Posted:

no buyers, many sellers ?

Nicky Tan should buy more, and Dollar-cost averaging (DCA) down.

the management should start SBB asap!

otherwise, reaches $1 soon ?

dydd |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Margin call?

LexLut88 ( Date: 18-May-2026 17:23) Posted:

| any idea what happen to the last min big drop ? |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

The challenge is to understand what the eventual revenue split might look like in 5 years time if we look at combined revenue of the gaming business for MBS and GENS, the pie is actually continuing to grow but the problem is MBS gaining market share at a quicker pace. The non-gaming can catch up but given the investments, depreciation will also impact in the near-term (although non-cash) - then the next question is the margin profile of the business.

This is common for any business undergoing transformation. As another kaki here shared, you need a long-term horizon to be able to sit through this.

JurongW ( Date: 16-May-2026 14:56) Posted:

Genting should not worry about paying higher taxes since they are cash rich and afford to pay 4 cents annually.

Higher profits translates to higher share price.

Have u work out the fair value of Genting in base, bull and bear case scenario once RSW2.0 is fully operational 5 years later, bearing in mind it is still competing with MBS for gaming revenue.

sgng123 ( Date: 15-May-2026 21:41) Posted:

They reporting lower profit to pay lower taxes.

RWS2.0 no1 priority as it tied to casino licence renewal.

casino is their ATM.

Once they secured licence, they start to put back operating free cash to net profit to prop up stock. |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Recalled reading that Analog Devices, Murata, Abbott UK, and Jabil have been publicly referenced as customers.

Top 3 customers of the company drive majority of the business and with all Analog Devices (semi-con) play leading the way, can this stock see further re-rating with the earnings turnaround?

|

|

Good Post

Bad Post

|

x 0

x 0

|

Who else would put in the kind of capex and commitment to support Singapore tourism?

alexvar ( Date: 13-May-2026 14:12) Posted:

pathetic company, getting totally decimated by Las Vegas Sands Corp MBS in Singapore.

a real risk that Singapore govt will not renew its gaming license anymore.

dydd |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Dont think SP can be compared - it suffers from operating in a structurally declining industry. I genuinely cant recall when was the last time I used postal services. Yes, they have the e-commerce etc but they are basically now living off property rental income as a lifeline for the otherwise loss making business.

GENS has a growing non-gaming business and yes gaming has declined y/y, at least got something to hope for with RWS2.0 while being paid to wait with decent dividends for the transformation to materialize.

luckyguy3 ( Date: 14-May-2026 22:14) Posted:

What if every quarter profit drops yoy??? after 5 years no bones left if really every quarter drops

u see Singpost.. last time used to be $2.. but becos every quarter profit drops, now only around 40 cents.

sgng123 ( Date: 14-May-2026 21:30) Posted:

| genS investment just treat it like 5 years SGS bond 5=6% coupon yield |

|

|

|

|

|

Good Post

Bad Post

|