|

Latest Posts By aragosta

- Supreme

|

|

| 16-Apr-2026 11:13 |

Others

/

Masters of the SEAS: KEPPEL, SCI, SEATRIUM, YZJSB

|

||||||||||||||||

|

|

No no no.... u read wrongly or misunderstood.... I only don' t believe in half last six chartists.... charts are fine for certain stocks like Reits which don' t have much surprise catalytic developments every now and then ..... for stocks like AEM, where forward acceleration trends are ongoing, and the AI business they are in, is moving at a supersonic pace, and there' s a surprise catalytic development every other month, the charts certainly have no effects, because charts only tell you what already happened, they tell you only what you feed into them........ in short, they tell the past.... they can' t tell you the movements and moments of the future....... they can' t tell you when and how the BBs and syndicates are going to move the stock based on their insiders info or tacit coordinated attacks ........ for high tempo, high octane stock of the moment, like AEM, and very soon Semby, the charts can never be accurate..... you should be thinking of every thing going forward, and not the current fundamentals or figure even...... Sembcorp' s forward trends are aggressively brewing.... the authorities know it and are placing a lot of weight on it, for example, according to the black market, their top guys were in the meeting with the PM delegation when they met the Aussie PM recently to discuss about renewables strategy and cooperation, that' s high regards for you to think.... because of the Iran war conflict, their renewable expertise will be in GREAT demand and in the acceleration pace ...Semby already has a high profile presence in UAE and Oman,,,,,, regardless of the outcome of the Iran conflict, and whether they will be involved in the Iran reconstruction or not, Semby could and should be EXPANDING ITS FOOTPRINT AND FOOTHOLD IN RENEWABLE ENERGY AND WATER INFRASTRUCTURE ACROSS THE ENTIRE MIDDLE EAST REGION.....not only their foot, but their entire body and face will be noticed and recognisable........The mafia' s financial experts have been observing and studying this, and I have made several comments on it.....by the time the market (and the highly paid analysts) and YOU GUYS realise and start talking about it, the black market people are already a quantum step ahead.... whether believe or unbeliever, IT IS IMPORTANT IF YOU WANT TO READ THIS COMMENT, YOU SHOULD READ EVERY WORD OF IT! |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 15-Apr-2026 22:26 |

Others

/

Masters of the SEAS: KEPPEL, SCI, SEATRIUM, YZJSB

|

||||||||||||||||

|

|

As of March 2026, the following " Unmagnificent Seven" brokerage firms (often grouped by market observers as those with the most bullish outlooks) have assigned Sembcorp Industries a price target of at least $7.00:

With the black market now setting a short-term target of $8.00 ~ driven by ongoing corporate movements and business developments expected to come to fruition, which only they know ~ you would expect these brokerages to copycat that $8.00 target based on the gangsters insiders insights.

UOBKH was the first to blink, raising its target price to $8.06 per share juz this week. Soon, one by one, the others will likely start calling for a more than $8.00 target......you can' t make this up! ...... before the mafia' s bold prediction, nobody, no analyst, NO ONE was targeting eight......

In fact, if the market suddenly realizes that what the black market has been weighing, is right all along, you can expect many to start to toss aside current fundamentals and technicals to chase the forward acceleration trends of the company. They' ll start writing beautiful songs about it, even though these business developments are already happening.......juz that they are afraid to say it......

From the onset, the gangs have been saying, or selling to me, Semby could potentially hit $10.00. I have been highlighting this whenever possible (go read them, the posts are still here).......It looks like the forest we are seeing from afar is actually a plantation of durian trees....... maybe if I' m in a good mood, and nobody disturb, I may post the internal insights why the black market people were thinking what the y were or are think ing, even before the market even know it' s possible ........ dyodddd anyway, gangsters are always good in story telling..

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 15-Apr-2026 00:48 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

I was reading this passage again.... " AEM now bridges the two most important zip codes in tech: the United States, the global brain of the semicon industry, where high-value design and software are born, and Taiwan, the ' Silicon Island' that is globally famous for being the unmatched leader in semicon manufacturing. By partnering with both the designers in Silicon Valley and the makers in Silicon Island, AEM is officially where the ideas meet the iron." I thought it was an excellent literacy piece , but I thought also the uneducated gangsters could not have possibly written this.... so i google and asked AI Gemini to help.... and it seems it was written by some EX-AEM people including the ex-CEO..... so I made a check again and found out that both Ex-CEO, still have substantial shares in the company.... so I checked further, this time with the mafia people.... what they told me was something very interesting, and intriguing... the structure of share holding is a very important element now, which I shall share later... which bring us to Temasek..... have they been asking their cronies and proxies to " buy" ? Are they planning to add more, or have a similar arrangement as ASE?....... something seems to be going on!.... because if ASE ends up with 10% and possibly more, they cannot be sitting still, because DPM seems to be promoting AEM, wherever he goes!....... anyway, believe or unbeliever, please remember these are gangsters stories , so dyodddd please.... but then price has been shooting up, but who' s been buying as price has gone up so much?.... can' t be those timid retailers, right? Think, think, think la......... |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 14-Apr-2026 22:28 |

Hong Leong Asia

/

Runaway Train powered by 3 catalytic factors

|

||||||||||||||||

|

|

No , this write up is not about what' s driving up the price today.... juz posting for fun...... ' anyway, can smell the brew already...... hehe it' s here ! ==== The proposed spin-off and listing of Guangxi Yuchai Marine and Genset Power Co on the Hong Kong Stock Exchange is a transformative move game changer for Hong Leong Asia. Greedy people would think, if I' m not getting free shares, why should I be excited? Well.think again, this listing drives value, earnings, and growth for HLA and its shareholders, in many ways...... 1. Enhancing HLA' s Value ~ Unlocking Hidden Treasures: MGP is HLA' s crown jewel, boasting a 15% net margin ~ nearly four times higher than the group' s overall average. A separate listing allows the market to value MGP independently, likely at a much higher P/E multiple than a traditional industrial conglomerate. ~ Once MGP is listed in Hong Kong, HLA' s stake will have a transparent market value. This often forces a re-rating of the parent company' s stock as investors realize the sum of the parts is worth more than the current share price. 2. Boosting Earnings & Future Growth ~ Very much AI-relevant and Capturing the Data Centre Boom: MGP is the #1 supplier of power generation engines in China. It is perfectly positioned to provide backup power for the massive rollout of AI data centres, a sector expected to grow by nearly 19% annually through 2030. ( Now, you BEGINNING to understand, why list in HK!) ~ High-Margin Marine Sector: As the #2 player in China&rsquo s marine engine market, MGP is riding the wave of shipping fleet renewals and the shift toward greener, high-tech engines. ~ Financial Independence: As a standalone entity, MGP can raise its own capital for R& D and factory expansion. This keeps MGP aggressive in the market without draining HLA' s cash reserves, allowing HLA to grow its other businesses (like building materials) simultaneously. 3. Strategic " Trump-Proofing" & Market Focus ~ China Market Dominance: The listing solidifies MGP' s brand in China, making it the " go-to" provider for critical domestic infrastructure. ~ Tariff Insulation: By listing the engine business in Hong Kong, HLA creates a " China-for-China" and " China-for-ASEAN" growth engine. This isolates these high-growth assets from potential U.S. trade tariffs, as MGP' s primary customers are in the AI, data centre, and regional maritime sectors rather than the U.S. consumer market. 4. Ultimate Benefits for HLA Shareholders ~ Dividend Potential: With MGP funding its own growth, HLA' s balance sheet becomes leaner. Analysts anticipate this could lead to higher payouts, with forecasts suggesting a 25% increase in dividends (up to S$0.05 per share). ~ Share Price Recovery: The recent drip" in price below S$3.00 is largely due to regulatory delays and a localized probe. The actual listing acts as a clearing event ~ once the IPO is approved, it removes the uncertainty discount currently weighing on the stock. ~The spin-off includes management incentive schemes. When MGP&rsquo s leadership performs well to drive their own share price, HLA shareholders win because HLA remains the ultimate parent. Why YOU should be EXCITED, very excited The market is watching for a " Value Unlock." HLA is currently viewed as a slow-moving industrial giant after the listing, it will be seen as the parent of a high-tech, high-margin power leader at the heart of the AI revolution. |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 13-Apr-2026 15:41 |

Hong Leong Asia

/

Runaway Train powered by 3 catalytic factors

|

||||||||||||||||

|

|

Since there' s interest, and since you asked, I shall talk a little..... remember, if you want real news and sensible predictions , stay with the gangsters views, and not some roadside peddlers wild speculations.... Last year, the black market predicted price would hit three only in the first quarter THIS YEAR (the posts are still here and in the other thread, go read them), yet when the stock was getting hotter and hotter towards last quarter of LAST YEAR , many roadside mercenaries were peddling Three dollar in October, November, December ..... what happen?.... anyway, below is the view from the coffee shop to your concern...... it is not from the black market people which is more stylo and tokkong, but that' s all I got for the time being, but I think good enough..... when the green light is given, I will talk why four is potentially possible, I think I know why but now not the time to talk..... ========== To have an complete understanding for a long term interest, it is essential to note the regulatory overhang that has caused Hong Leong Asia' s share price to soften recently. While the business fundamentals remain strong, specific events in China have introduced a layer of risk that has temporarily cooled investor enthusiasm. The Regulatory Overhang: Why the Price Dropped after a short surge in anticipation of good results The primary reason for the recent share price drip to below S$3.00 is not a lack of profit, but rather governance uncertainty in China: ~ In October 2025, authorities in China detained Wu Qiwei, a director of HLA' s main subsidiary (China Yuchai), and the former chief accountant of the operating unit, for " serious violations of discipline and law" . This news caused an immediate 20.6% plunge in HLA' s shares. ~ Although HLA' s daily operations remain uninterrupted, the fact that a key leader is under disciplinary review by Chinese authorities has created a persistent regulatory overhang. Investors are naturally cautious about potential broader implications or further management changes. ~ Market Sentiment vs. Earnings: Interestingly, HLA reported a 48.6% surge in net profit for H2 2025, yet the share price continued to fall. This reflects a market that is currently prioritizing " headline risk" and regulatory clarity over financial performance. (This one actually copied from the Business Times. Why the Guangxi Yuchai Marine and Genset Power (MGP) Listing is Stalling The listing of Guangxi Yuchai Marine and Genset Power (MGP) is currently navigating a stricter regulatory environment: ~ As of April 2026, the China Securities Regulatory Commission (CSRC) has requested supplementary materials regarding the company' s controlling shareholders and controllers. This is part of a broader trend where Chinese regulators are tightening the criteria for mainland firms to sell shares in Hong Kong to ensure higher deal quality. But to my mahjong kaki, it' s no problem la. In fact he told us to pang sim la. ~ While the application was filed in January 2026, the vetting process is taking longer than some investors anticipated due to these additional information requests. Consolidated Value & Growth Roadmap for Shareholders Despite these hurdles, the long-term case for HLA remains anchored in the " Value Unlock" Why the market should (eventually) get excited: The current price dip offers a potential entry point for those who believe the internal probe is localized and the listing will proceed. Once the CSRC clears the supplementary materials and the IPO date is set, the regulatory overhang is expected to lift, shifting the market' s focus back to HLA' s record-breaking earnings. Sometimes, people like the newbies cannot see the forest, focusing instead only on the tree. While they are selling, the coffee shop uncles are quietly accumulating. There is always a reason why the mafia bosses are enjoying lobster, birdnest and abalone meals, and why you guys can only afford hawker foods..... |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 13-Apr-2026 10:51 |

Hong Leong Asia

/

Runaway Train powered by 3 catalytic factors

|

||||||||||||||||

|

|

Could be earth shattering movements coming ...... according to my mahjong kaki, over four is potentially possible by latest august ( I also don' t know why he mentioned August) ..... anyway, if the road side half past six peddler don' t disturb me and try to be kay kiang, I may try to finding out more and talk a little..... |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 12-Apr-2026 15:18 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

This beauty didn' t hit $4.84 in 10 days.... But it was close enuf, it did it in 15 days......so in another 10 days, can we expect the same pattern? Maybe, if it coincides with the convincingly ending of the conflict......and that' s not all, if the gangsters are to be believed, besides the brewing development that has nothing to do with a contract win, and which I mentioned earlier, there is also another news of a possible incoming new customer, with the help of a partner........ there' s not much interest in here anyway, so I shouldn' t be talking too much on this,... in any case, write so much, also nobody read, also one-ime dissident ah tong has been doing an excellent job promoting and selling......don' t want to steal his thunder.... btw, I also asked you to look out for Sembcorp' s unusual movements, and as it happened, it is actually crying out to you, it could reach eight as early as this month (impossible, right?), if not, by latest next month.... don' t ask me why, I also don' t know why...... but you know the mafia .... they don' t play games.....

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 05-Apr-2026 19:37 |

UMS

/

Scaling new HEIGHTS with new catalysts

|

||||||||||||||||

|

|

THE JAPANESE ARE COMING! THE JAPANESE ARE COMING!

Microsoft charts US$10 billion of outlays in AI-eager Japan https://www.businesstimes.com.sg/companies-markets/telcos-media-tech/microsoft-charts-us10-billion-outlays-ai-eager-japan Not now, but when the coast is clear, I will explain a little why post this news which has no direct relevant to UMS.... meanwhile would UMS be another DYNA-MAC ? Would Luong even allow it to happen? |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 05-Apr-2026 13:28 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

As I said, there' s a war going on, so it' s difficult to take every message, every story, every reporting at face value. In any case, my posts are meant " to entertain" (depending on how you interpret its meaning)....... I won' t be making any post for the time being, unless I am 100% cock sure the development will happen within a 3 months window period, or I may come in to correct a misconception, juz like the case below......The March 26th transaction is not the same as the March 18th trade, which just didn' t get its own notification. It' t not " fake news" ~ there were just specific reasons why a notification wasn' t required at that time. Here is a simple coffee shop explanation (not written by me hor) to help break it down: Transaction Timeline for AEM (March 2026 trading transactions) Based on recent disclosures, JPMorgan (JPM) has been " trading the volatility" of AEM shares ~ buying and selling quickly to capture price swings. Here' s how their reporting actually works and why some trades (like the 1.225 millions share purchase on 18 March) appear " hidden" at first glance. The Logic Behind the Disclosures SGXNet filings can be quite confusing. Here' s why you don' t always see a separate notice for every single trade:

1. The 18 March Transaction & The " Correction" ~ On 18 March 2026, JPM became a substantial shareholder by crossing the 5% threshold (buying 1,225,400 units at SGD 3.72), requiring a SGX update notification ~ While an initial notice went out on 19 March, a Replacement Announcement (Ref: SG260319OTHRECDC) was issued on 20 March. This was a critical correction to ensure the public record accurately reflected the massive 1.2 million unit acquisition from 18 March. ~ However, JPM' s substantial shareholder status was brief. By 19 March, they trimmed their stake back down to 4.9%, meaning they were no longer required to report their daily trades until they hit 5% again. 2. The 26 March Transaction: A Fresh Entry ~ On 26 March, JPM bought 1,794,400 shares for roughly $8.95 million. This pushed their stake from 4.98% back up to 5.18%. ~ Because they crossed that 5% line again, it triggered a brand-new legal requirement to file a disclosure. ~ This trade on 26 March was entirely separate from the earlier 18 March activity. Anyway, these buy and sell transactions relating to such large institutional investment funds are not so critically significant here, the point I&rsquo m trying to make is ... It is important to view these disclosures as standard market activity rather than a shift in institutional sentiment. JPMorgan functions as a global investment house, often acting as a custodian or nominee for a wide range of institutional and high-net-worth clients. Consequently, many of these transactions are client-driven rather than proprietary trades made with JPM' s own capital. When a sale occurs, it typically reflects a client' s decision to take profits, rebalance a portfolio, or reallocate funds to another asset ~ much like a retail trader would ~ rather than a lack of confidence by JPM in the company' s long-term value.

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 29-Mar-2026 22:15 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

The reason why I wrote the following summary when I said I would not post the black market price analysis now, is to ensure that people like the newbies would not to read too much into AEM physical assets and cash position....or trying to use charts to help them make sense of AEM current behavior...... like " how come the price keeps surging?" .....

If you keep focusing on the traditional NAV and PE, you' ll miss the real AEM stoy...... and the plot behind it.... As I said, in this AI era, Intellectual Property is the only real asset that matters...... AEM' s true book value does not sit in its factories or office equipment or cash in the bank it resides in its patented technology, the thermal brain that it pioneered, the industrial bridge through technology partnership that it builds....... In this respect, it simply means that charts and technicals are irrelevant&hellip in short, they are useless....it&rsquo s not like crossing the road where green means go, red means no go.... you' ll get killed crossing like that&hellip &hellip read deeper into what AEM is growing and going into, it' s future growth, it' s forward PE, it' s next horizon.... Charts and technicals tell you the past, it cannot tell you the future in this instance.....that' s why when the syndicates, the gangsters play, they based on their forward instinct and insiders info, never on the shadows and candle stocks beautifully drawn by the analysts..... of course no analyst will tell you that, because charts and TA are their oxygen........ trust me, throw away those circles diagrams and bar charts for this stock, they only mislead you..... see you in a week!

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 29-Mar-2026 17:42 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

In case there are doubts of a black market report on the possibility of AEM' s price surge to eight, I shall post a snippet of it, a short summary...... but it is to be used for future reference only, because when the No Horse Run truly starts, it will be too late for you to do anything........ believe or unbeliever, don' t blame anyone...... as I said, there' s a war going on, but AEM has shown remarkable resilience in the face of all the ballistic missiles raining on it....... if you don' t know already, that' s the characteristic of a TRULY AI relevant stock......... ========== The Executive Summary: Is AEM' s price today " Expensive" or still " Early Days" ? While the NAV looks high, in the AI era, Intellectual Property is more valuable than physical assets. AEM' s worth isn' t found in its factories or its cash: it is found in the 2,000-watt thermal barrier it has broken, the SLT brain it has perfected, and the Taiwanese Lab-to-Fab bridge it has built. This " Triple-Pillar Moat" , that balance sheets can' t capture, is its true book value. If AEM can raise its Net Margin from the current ~4% toward the industry standard of 15% to 20%, the $8.00 target isn' t just possible: it' s supported by the same math that drove iFAST to surge from $1 to $10 in under one year. And here' s the scary part: the black market thinks AEM is " More Valuable" than iFAST on current form. While iFAST' s surge was remarkable, AEM' s structural setup is arguably more robust. AEM possesses significantly more positive drivers than iFAST did at its inflection point ~ iFAST is a platform (it connects people to products). ~ AEM is a bottleneck (the products cannot exist without their tech). Investors pay much higher P/E multiples for " Bottlenecks" than they do for " Platforms" . So, in summing up, if you judge AEM by the weight of its physical assets, it looks expensive. If you judge it by its role as the indispensable gatekeeper of the AI supply chain, it is still early days. This isn' t just a hardware play it is the AI Quality-Assurance Standard for the next decade. dyoddd, please.....

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 29-Mar-2026 12:39 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

I wrote not too long ago, there would be a new development, didn' t knoe it would be so soon..... in any case, I wrote again below, there could be another development, (this is a separate one) and I can confirm this one got nothing to do with a contract win....... I decided against posting the black market' s lengthy analysis on the possibility of AEM hitting eight, or even the chance of doing an iFAST style of price surge..... But there' s a war going on, with the degree of unpredictability increasing as of now......Like, what if a nuclear bomb is dropped.... besides, I will be travelling.....not forgetting it is not my business to feed the mercenaries......so maybe, some time later..... if there' s interest....... In any case, my advice to the shortists still remains: do not try to short this stock like it' s your hobby...... all things being equal before the war, the stock would have been half way to the moon by now.......fortunately the AI Boom would mitigate all the negatives of the US/Iran conflict, and so even in the midst of an ugly war, AEM will still look pretty........ Meanwhile, do look out for the unusual movement of Sembcorp......The gangsters are not playing a fool with their numbers...... this could be another surprise packet coming out from the rumbles of the war.......

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 29-Mar-2026 01:04 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

The New Strategic Map of AEM: Stretching from US to Taiwan We have another tokkong saying in the Black Market: " It' s not just WHO your buyers are, but WHERE your buyers are from." AEM now bridges the two most important zip codes in tech: the United States, the global brain of the semicon industry, where high-value design and software are born, and Taiwan, the ' Silicon Island' that is globally famous for being the unmatched leader in semicon manufacturing. By partnering with both the designers in Silicon Valley and the makers in Silicon Island, AEM is officially where the ideas meet the iron. AEM has undergone a fundamental transformation in early 2026, transitioning from a company historically reliant on a single US anchor customer (Intel) to a diversified global power in the AI and High-Performance Computing (HPC) testing space. The recent strategic partnership with ASE Technology, the world' s largest Outsourced Semiconductor Assembly and Test (OSAT) provider, marks the validation of AEM' s technology as an industry standard. 1. The Pivot: Beyond the US Big Tech Giants For years, AEM' s strength lay in its pillar customers from the United States: Intel, Micron, AMD, and Broadcom. While these relationships established AEM' s reputation, the March 2026 partnership with ASE Technology from Taiwan provides the missing link: Global Manufacturing Scale. a) Geographic Significance: By bridging the gap between US design and Taiwan' s manufacturing dominance, AEM has positioned itself at the heart of the global supply chain. b) The " Weight" of ASE: ASE serves over 90% of the world' s electronics companies. This partnership provides AEM with a foothold in Taiwan and access to a massive pool of potential new clients. 2. The Twin Pillars of Product Excellence AEM' s competitive moat is built on two specialized services that are equally critical to the AI revolution: a) System Level Testing (SLT) ~ The " Brain" : SLT ensures complex AI chips function in real-world environments before shipment. ~ The Value: It is the primary service attracting US tech giants, ensuring long-term customer retention through deep integration into their production cycles. b) Advanced Cooling: The Life Support for AI ~ The Problem: Extreme Heat: Next-gen AI chips get incredibly hot ~ pumping out as much heat as a large space heater (2,000 watts). Without a way to cool them down instantly, these expensive chips would melt during testing. ~ The Solution: AEM' s PIXL&trade Technology: AEM' s patented system acts like smart air conditioning for a chip. Instead of cooling the whole thing at once, it targets specific hot spotswith different temperatures. ~ The Competitive Edge: This technology is brand new to the market. AEM is currently about one full generation ahead of its main rivals, like Teradyne or Advantest, giving them a massive head start. 3. The Catalytic Value of the ASE Partnership The collaboration with ASE is more than a sales agreement it is a financial and strategic integration: ~ Financial Alignment: ASE committed to a S$12 million private placement, which could lead to a ~10% ownership stake in AEM. ~ Revenue Triggers: The deal includes 28.1 million warrants tied to hitting revenue milestones of S$30M and S$50M from ASE-introduced business. ~ Synergy: ASE gains the Lab-to-Fab bridge ~ moving chips from engineering labs to high-volume manufacturing faster ~ while AEM gains massive operational scale. 4. The Next Horizon: Driving Revenue Through New Frontier AEM' s FY2026 revenue guidance (S$460M &ndash S$510M) was issued before the ASE deal was finalized, suggesting a high probability of an upward revision later this year. a) Customer Diversification: AEM is not sitting still with its historical partners. The company is rapidly pivoting toward the world' s most demanding AI/HPC powerhouses. A second major AI/HPC customer is projected to become AEM' s largest client by the end of 2026, overtaking Intel. b) Pioneering New Niche Product Frontiers: AEM' s constantly scouting for untapped technical niches where high-precision testing is a non-negotiable necessity: ~ High-Bandwidth Memory (HBM): AEM is currently validating final test handlers for HBM, the essential backbone of AI servers. This move into the memory market represents a massive new product frontier. ~ Quantum Computing: Looking toward the " next frontier," AEM is already established in cryogenic testing through partnerships with leaders like Bluefors. This positions AEM at the ground floor of the quantum revolution, far ahead of traditional competitors. c) Unstoppable Momentum and Value Discovery: Despite a stock price increase of over 100% YTD, the market is only beginning to price in AEM' s long-term trajectory. Major analysts continue to raise target prices, citing a massive earnings recovery cycle. This reinforces the view that AEM' s future performance will not be limited by its current market cap or past performance records. The Weight of the Matter AEM Holdings has successfully moved from being a specialized equipment supplier to a mission-critical infrastructure provider for the AI era. With its thermal Golden Goose, its new Taiwan-based partnership, and a diversifying client list of global titans, the company is no longer just participating in the market ~ it is helping define its limits.

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 25-Mar-2026 17:36 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

Since the there is interest again. I shall post a series of posts over this weekend including the partnership with ASE Technology whose AEM' s initial issue of shares and WARRANTS to them were viewed as uninteresting by the newbies and promoted by mercenaries as fake negatives ...... Well I hope you all know who Jason Chang is! I will also post the why coffee shop uncles' eight may not be a joke....... by next month, there will be another TOKKONG development that will be mind blowing , and it has nothing with do with a contract win, or another angmoh pillar clients.......also if you are not lazy to read thru all the gangsters long winded messages, you may be able to spot an alert or two of their speculations ..... I will be also be shifting the furniture of UMS in this thread to its own thread, in anticipation of the next big tech wave.... as I said, believe or unbeliever, up to you.... otherwise, just watch the believers HUAT will do! |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 22-Mar-2026 14:07 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

FROM THE BLACK MARKET' S NOTICE BOARD There&rsquo s a famous saying in the Black Market: It isn' t just in WHO is buying, but WHAT they are buying. " A Generational Pivot: The TCS Evolution. While AEM' s expanding clientele portfolio of Big Tech partnerships in well-documented, the true transformation lies deeper. The segment shift isn' t merely in WHO is buying, but in the fundamental nature of WHAT they are buying: moving from standalone hardware to mission-critical, integrated Test Cell Solutions (TCS)." The Test Cell Solutions (TCS) segment isn' t just a business unit for AEM it' s their " generational pivot." It marks the transition from being a provider of standalone machines to becoming the indispensable architect of the entire semiconductor testing environment. Here is the breakdown of why TCS is the secret (magic) sauce defining AEM' s future: 1. What exactly is TCS? a) TCS is an integrated cell that combines three critical components into one automated process: Active Thermal Control (ATC), System Level Test (SLT), High Parallelism Automation. a) Think of a " Test Cell" as a complete, integrated ecosystem. Instead of just selling a handler (the robot that moves chips), TCS provides the full stack: the thermal control systems, the high-speed electronics, the contactors (sockets), and the software that manages the " handshake" between the chip and the tester. It' s a turnkey laboratory-in-a-box. 2. Is it AEM' s forte and niche? a) Absolutely. AEM is considered one generation ahead of its competitors in the SLT space. Their specific niche is solving the thermal challenge of AI chips. b) While competitors often specialize in just one component (like only sockets or only testers), AEM' s forte is System Level Test (SLT) integration. They own the niche of " Massively Parallel Testing," where hundreds of complex chips are tested simultaneously under extreme thermal conditions. No one else integrates these moving parts as seamlessly at scale. 3. The Margin Secret from the Magic Sauce a) AEM' s value proposition is shifting. By 2026, the Test Cell Solutions (TCS) segment is expected to represent 70% of total revenue (up from 63% in 2025), effectively transitioning the company from a hardware builder to a high-margin tech partner. This segment leverages proprietary PiXL thermal technology, an essential requirement for testing the next generation of high-power AI chips. b) The Recurring Revenue Model: The magic sauce is the shift from one-time machine sales to a high-margin consumables model. Every chip design change requires new, specialized contactors and change-over kits. AEM isn' t just selling the " printer" they have become the exclusive provider of the " high-precision ink" required for the life of the machine. 4. How important is it to current and future clients? a) As chips get smaller and more powerful (think AI and 5G), they generate immense heat and are prone to infant mortality (failing early). Clients can no longer rely on simple tests they need the deep, environmental stress testing that TCS provides. For a client like Intel or next-gen AI chipmakers, TCS is the insurance policy that their $1,000 chips won' t fail in a server farm. b) Future Necessity: As chips move toward 2.5D/3D packaging (stacking multiple chips on top of each other), the chance of a hidden defect increases. Testing each layer individually is too expensive. Big tech companies must move to System Level Testing (SLT) to catch these defects, and AEM currently owns the most advanced automated factory-ready version of this tech. 5. Why it is difficult to copycat? a) You can' t the just copy a test cell. It requires a rare marriage of mechanical engineering, thermal science, and high-speed signal integrity. AEM has decades of proprietary data on how materials behave at -40° C to +150° C while carrying massive electrical loads. That institutional knowledge is a massive barrier to entry. b) AEM holds a deep portfolio of patents protecting their thermal control and handler designs. Even if a competitor builds a similar machine, AEM' s software and hardware are already baked into the manufacturing lines of its biggest customers, making it very expensive and risky for a client to switch 6. Keeping the Magic Sauce secret a) What is a Plan of Record (POR)?: It means the customer has designed their entire manufacturing floor around AEM' s machines. Once AEM is written into a customer' s Plan of Record, they are locked in for the entire lifecycle of chip generation (usually years). Switching vendors would require re-validating the entire testing process, costing millions in delays. b) The AI Anchor Lock-in: As AI chips become more complex, AEM' s software becomes the brain of the factory floor. This creates a digital lock-in the more data the TCS collects, the better it gets at predicting failures, making AEM' s ecosystem impossible to rip out without blinding the manufacturer. Sticking with AEM: Brewing Long-Term Gains that keep flowing a) In short, TCS transforms AEM' s revenue from a lumpy hardware business into a sticky, recurring stream. It' s the " Nespresso Model" of the semiconductor world: the world-class machine gets you through the door, but the high-margin, proprietary pods (the consumables and integration services) keep the revenue flowing for a generation. b) When analysts like JPMorgan or DBS look at a company, they love " sticky" revenue. ~ With 70% of revenue tie to TCS, AEM is no longer just selling a product they are selling an indispensable service. ~ As AI chips get more powerful (and hotter) in 2027 and 2028, the demand for this specific thermal niche will only intensify. Essentially, AEM has found the one thing AI chip makers must have to ensure their chips don' t fail, and they' ve patented it. |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 22-Mar-2026 13:22 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

WOW! didn' t see that coming! Welcome on board anyway, ah tong.... Even mini man is getting into the act https://www.minichart.com.sg/2026/03/20/aem-stock-analysis-ai-tailwinds-customer-growth-and-upside-potential-in-2024-2027-12/ https://simplywall.st/stocks/sg/semiconductors/sgx-awx/aem-holdings-shares https://sgwealthbuilder.com/category/stocks/ |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 21-Mar-2026 17:40 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

I was observing my previous post (below) and in less than 2 hours, it garnered more than 200 views! My other threads couldn' t even get 200 views in one single day........ Which means there seems to be a lot of interest in this stock, so I have to be careful and responsible in what I post! Otherwise, a lot of newbies and less experienced investors might be misled, if they follow the wrong sentiments of the stock. The true highlight of yesterday' s news developments was actually the confirmation of the Intel " Epic Supplier" award, a move previously speculated upon by the black market. However, retail sentiment was largely distracted by announcement of JPMorgan' s purchase of AEM' s shares and its subsequent emergence as a substantial shareholder. I was also caught up in this retail euphoria and made posts relating to it, but it is important to clarify that this could send the wrong signal. JPMorgan' s purchase does not represent a proprietary trade using their own capital. Instead, they are facilitating trades on behalf of institutional clients, acting as a nominee and custodian ~ similar to other brokers like UOB Kay Hian, CGSI. Therefore, their " purchase" does not necessarily mean the bank is taking a larger directional stake conversely, a future " sale" may not indicate liquidation, though both are easily misinterpreted by new and seasoned traders alike. This shouldn' t be treated with great significance, but as normal transactions. We should instead refocus on the Intel award as a primary catalyst. The resulting publicity and goodwill serve as a powerful testimony to attract other Big Tech firms. This could potentially transition companies like Meta and Nvidia from indirect beneficiaries into full-scale anchor clients for AEM. Also, we should be more excited with AEM' s capture of a second major AI/HPC client which is expected to contribute to the bottom line by the end of this fiscal year. These factors should bolster earnings over the next two quarters and provide upward momentum for the stock price. I would not be surprised to see a formal upward revision in revenue guidance, which could further act as the next major catalyst. Remember June last year, AEM experienced a 14.52% share price jump in a single day following the company' s announcement that it was raising its revenue guidance for the first half of FY2025? Imagine, if they do it again before the next half yearly results!

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 21-Mar-2026 11:32 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

JPMorgan Adjusted Transaction Log REPORTED IN SGX FILING Date of acquisition of or change in interest: 16 March 2026 Purchase 555,000 units at average price of SGD 3.35 per unit via market transaction. Increase of 77,400 units pursuant to the Prime Brokerage Agreement Final interest (Direct plus Deemed) 5.183% (up from 4.982%) Date of acquisition of or change in interest: 17 March 2026 Sale of 910,200 units at average price of SGD 3.53 per unit via market transaction Increase of 22,300 units pursuant to the Prime Brokerage Agreement Final interest (Direct plus Deemed) 4.901% (down from 5.183%) YET TO BE REPORTED IN SGX FILING Date of acquisition of or change in interest: 18 March 2026 Purchase 1,225,400 units at average price of SGD 3.72 per unit via market transaction. Decrease of 15,800 units pursuant to the Prime Brokerage Agreement Final interest (Direct plus Deemed) 5.286% (up from 4.901%) Note: Substantial shareholders have 2 business days to report changes therefore, a transaction occurring on 18 or 19 March might not appear on the SGX central portal until the following Monday or Tuesday. The above UNDISCLOSED info came from the coffee shop uncles, which I overheard while having my kopi-o sui tai. Please do not shoot me, if I overheard wrongly hor....... IMPORTANT TO NOTE! The explicit mention of the Prime Brokerage Agreement in these filings confirms these are client-driven activities and are not proprietary trades by JPMorgan (using their own cash). They are facilitating the trades of institutional clients, likely hedge funds, or high-networth clients (I kept telling you this until I got no saliva! Yet gongkias newbies would panick when they see a sales by JP Morgan). JPMorgan Chase & Co. typically files as a Substantial Shareholder because the aggregate of its clients' holdings (for which it acts as a nominee/custodian) exceeds the 5% threshold. |

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 20-Mar-2026 16:03 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

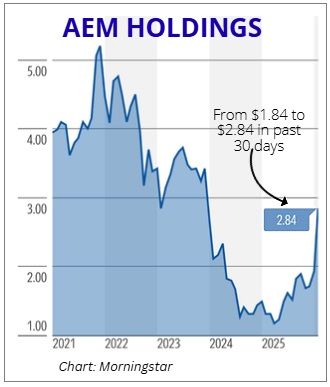

Saw this picture..... someone was trying to make a joke out of it.... except it may not be not a joke....... yesterday price hit $3.84 intraday high... so if you follow the logical money trail.... In 30 days, AEM' s price went from $1,84 to $2.84 In 20 days, AEM' s price went from $2.84 to $3.84 in 10 days? whatever it' s in mind, don' t bet against it, now is $4 plus..... takes another 70c plus ===== btw, I was trying to post my previous post BEFORE LUNCH' . ....and managed to go thru only a while ago, so the sting of the message was lost in the delay.....

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| 20-Mar-2026 15:06 |

AEM SGD

/

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||

|

|

Whole day I was walking up and down 52 Serangoon North Avenue 4, hoping some one would recognise me and come up to me..... But alas there were none, it' s like some people just have a nice meal at a 5 star Michelin restaurant and leave with out paying, pretending nothing' s doing...... but it' s okay because I myself was pretending (very hard) too, trying to be humble and try not say a thing to sound like bragging....... but I tell you, it' s very very hard..... very very difficult to stay humble when the stuffs you anyhow talk, somehow turn up to be true!........btw, it hits four now in case you pretending not to notice Any way, to those very shy believers, I got another coming great news for you, another tokkong development is likely on the way that will rocket this gem even further away from those unbelievers who brag they sold @$3, @$3.38......, this may come as early next month&hellip today, the news seems to be on JPM, but I tell you, Temasek is working very hard not to be overshadowed......heard it is trying to get another big tech company, in which it has a big stake to join as a high value partner of AEM....this one in fact, the black market is 99% confident will happen soon&hellip .. On another note, THIS FOLLOWING PIECE IS DEDICATED TO JURONGWEST, one of the few black market believers ...... basically addressing his confusion and concern....... For those who are too lazy to read my lengthy statement below, you may just read the following summary which provide the gist of it...... A LAZY SUMMARY JPMorgan Chase & Co. became a substantial shareholder in AEM Holdings on March 19, 2026, increasing its stake to 5.19% (16,307,735 shares) following a market acquisition. A significant portion of this holding is managed under a Prime Brokerage Agreement, which allows clients to leverage and borrow shares for trading, yet requires institutional disclosure. JPMorgan' s increased investment indicates strong conviction in AEM' s AI-driven growth trajectory, with FY2026 revenue guidance of S$460M - S$510M and a forward P/E of ~29.4x, suggesting resilience against patent litigation with Advantest. Furthermore, AEM presents a value opportunity, trading at a 25~35% forward P/E discount to industry leaders Advantest and Teradyne. ========= Here is a structured breakdown of the latest developments regarding JPMorgan' s investment in AEM Holdings as of today, March 20, 2026. 1. The Transaction & Current Stake On March 19, 2026, JPMorgan Chase & Co. officially crossed the 5% Substantial Shareholder threshold. ~ The Buy: Purchased 555,000 shares in the open market. ~ The Price: An average of S$3.35 per share. ~ Pre-Transaction Stake: 15,629,935 shares (4.97%). ~ AFTER YESTERDAY' S TRANSACTION: Current Stake: 16,307,735 shares (5.19%). ~ Note on Accuracy: The figures from the March 19 SGX Filing are the definitive legal record. Previous higher estimates likely included non-notifiable or " right-to-recall" shares that hadn' t yet triggered a formal disclosure. 2. Understanding the " Prime Brokerage Agreement" A large portion of JPMorgan' s stake is held under a Prime Brokerage Agreement, simply means &hellip &hellip ~ The Banker' s Role: JPMorgan acts as a " one-stop-shop" for hedge funds and large investors. ~ Deemed Interest: Even if JPMorgan' s clients are the ones buying, Singapore law requires JPMorgan to disclose these shares as a deemed interest because they control the custody and lending of the stock. ~ The Signal: When a Prime Broker' s holding increases, it usually means their most sophisticated, high-networth clients are aggressively " long" on the stock. ~ Newbies' often MISCONCEPTION: So when you see an SGX' s filing by a big institutional fund (like BlackRock, JPM, Goldman Sachs) it DOES NOT necessarily means that that fund is buying for its own &ldquo trading accounts&rdquo . It could well mean it is executing the order on behalf of a high networth client. Got it? 3. The Confidence Factors in the Increase in Stake JPMorgan' s move to buy at S$3.35 ~ a price significantly higher than the S$2.00 range seen earlier this year ~ signals high conviction in two areas: ~ Growth Inflection: AEM has issued FY2026 revenue guidance of S$460M &ndash S$510M. This is driven by a massive ramp-up from a new AI/High-Performance Computing (HPC) customer that is expected to become their largest revenue source. Multiple sources are persistently stating as of late, many top tech companies have been in need of AEM' s critical high value services. ~ Legal Resilience: By increasing their stake, institutional investors are signaling that the Advantest patent litigation is likely manageable. They likely view AEM' s new thermal testing technology as unique enough to either win in court or reach a settlement that won' t cripple the company' s finances. 4. Why AEM is STILL Undervalued vs. Peers Despite AEM' s recent price surge, it remains " cheap" when compared to the global semiconductor testing duopoly:

~ The Opportunity: AEM is trading at a 30% average discount to its peers on a forward-earnings basis. ~ Small-Cap Alpha: Because AEM is much smaller (market cap ~S$1.18B), its earnings explosion from new AI contracts has a much bigger impact on its stock price than similar wins would for a US$100B giant like Advantest. 5. The Final Word JPMorgan' s entry as a substantial shareholder marks a turning point for AEM. By paying S$3.35 per share, the bank is validating AEM' s transition from a legacy Intel-dependent supplier to a diversified AI infrastructure play. While the Advantest lawsuit remains a risk, the Forward P/E discount of nearly 30% compared to global peers suggests that the market has more than priced in the legal uncertainty, leaving significant room for catch-up growth as FY2026 revenue targets are met.

|

||||||||||||||||

| Good Post Bad Post | |||||||||||||||||

| First < Newer 101-120 of 612 Older> Last |