Latest Forum Topics /

AEM SGD

Last:9.9

-0.19

-0.19

|

|

|

AEM (+Venture, UMS) the most AI-relevant SGX stock

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

JurongW

Elite |

22-Mar-2026 14:50

Yells: "Earnings give weight, Chart give wings" |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

x 0

x 0 Alert Admin |

Below report is generated by MSCP for reference. If the figures are wrong, do flag out. Thanks.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Company | FY26 Forward P/E | FY27 Forward P/E | Latest Target Price | Key Drivers |

|---|---|---|---|---|

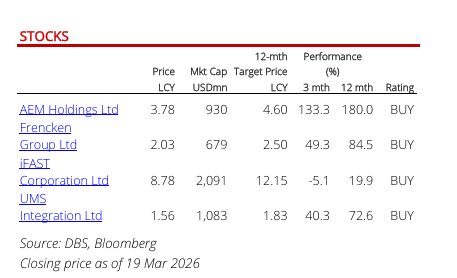

| AEM Holdings (SGX:AWX) | Consensus ~15&ndash 17x DBS applies ~25x | ~14&ndash 15x | SGD4.60 (DBS, Mar 2026) | Ramp‑ up of new AI/HPC customer, margin expansion from system‑ level test leadership, recovery post‑ FY25 forex drag. |

| UMS Holdings (SGX:558) | ~23.7x FY26 | ~19.3x FY27 | SGD1.84 (DBS, Jul 2025) | Strong Applied Materials demand, Penang expansion, FY26 net profit forecast +30% y/y, FY27 +23% y/y. |

| Frencken Group (SGX:E28) | ~22.5x FY26 | ~20.1x FY27 | SGD2.50 (DBS, Mar 2026 median TP across brokers) | Semiconductor recovery from 2H26, resilient medical/automation demand, diversified end‑ markets. |

🔎 Key Insights

- AEM: Consensus multiples are cheapest (~15&ndash 17x), but DBS&rsquo s bullish case (SGD4.60 TP) assumes re‑ rating to ~25x forward P/E if the AI/HPC ramp delivers.

- UMS: Most expensive on forward multiples, reflecting strong Applied Materials exposure and consistent earnings growth.

- Frencken: Valuation sits between AEM and UMS, offering diversified resilience but not commanding UMS‑ like premiums.

⚖ ️ Investor Takeaway

- Cheapest Growth Play &rarr AEM (consensus multiples low, upside if DBS&rsquo s bullish case materializes).

- Premium Stability &rarr UMS (highest multiples, justified by strong client demand and growth visibility).

- Middle Ground &rarr Frencken (resilient margins, diversified demand, moderate valuation).

👉 With these fresh figures, you can confidently share that UMS is the most expensive (~23.7x FY26, ~19.3x FY27), Frencken sits mid‑ range (~22.5x FY26, ~20.1x FY27), and AEM is cheapest on consensus (~15&ndash 17x), though DBS&rsquo s SGD4.60 TP implies a bullish re‑ rating to ~25x.

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

Good point, but has AEM reached maximum optimism before the selling appears, or Does it still have the legs to chiong further ?

All will find out this week.

sgtrader ( Date: 22-Mar-2026 14:34) Posted:

|

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

Analysis and Comparison of AEM and ST engineering valuations based on their forward earnings.

Based on current analyst forecasts, ST Engineering (STE) looks more expensive than AEM on FY26&ndash FY27 earnings multiples, with STE trading at ~23x forward P/E versus AEM mid‑ teens valuation range. AEM growth is expected to accelerate from FY26 onwards, while STE valuation premium reflects its diversified, resilient earnings base.

📊 Valuation Comparison: AEM vs ST Engineering (FY26&ndash FY27)

| Company | FY26 Forecast | FY27 Forecast | Valuation Notes |

|---|---|---|---|

| AEM Holdings (SGX:AEM) | Earnings recovery expected as new customer ramps (Intel, AI test solutions). Analysts project strong FY26 rebound after flat FY25. Forward P/E estimated ~15&ndash 17x. | Continued growth into FY27 with margin expansion from system‑ level test leadership. Valuation remains below STE, suggesting cheaper relative multiple. | Market cautious due to cyclical semiconductor demand, but upside tied to AI/IoT megatrends. |

| ST Engineering (SGX:S63) | Strong revenue growth across aerospace, defence, and urban solutions. FY26 forward P/E around ~23x. | FY27 earnings visibility supported by robust order book, but valuation premium persists. Dividend payout policy (1/3 of earnings growth) adds support. | Considered &ldquo expensive&rdquo relative to peers, but investors pay for stability and diversified earnings streams. |

🔎 Key Insights

-

AEM:- FY25 is transitional, with earnings weighed down by forex losses and muted growth.

- FY26&ndash FY27 expected to deliver strong gains as new customers ramp up and margins expand.

- Valuation sits in the mid‑ teens P/E range, making it cheaper than STE.

- Risk: Semiconductor cycle volatility and dependence on Intel orders.

-

ST Engineering:- Diversified across aerospace, defence, and smart city solutions, giving resilience.

- Analysts highlight efficiency improvements and dividend growth, but valuation is steep at ~23x forward P/E.

- Investors pay a premium for stability and visibility, but relative to AEM, STE is more expensive.

⚖ ️ Trade‑ Offs

- AEM offers higher growth potential at a lower valuation, but carries cyclical risk.

- STE commands a premium valuation due to stability, dividends, and diversified earnings, but upside may be capped by already high multiples.

👉 Bottom Line: If you&rsquo re looking for growth at a reasonable price, AEM is cheaper on FY26&ndash FY27 earnings forecasts. If you prefer defensive stability with dividends, ST Engineering justifies its higher valuation but is clearly more expensive relative to AEM.

Senior

Yells: " Earn the right to WITHDRAW consistently."

x 0

Alert Admin

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

AEM has surged past the 61.8% Fibonacci retracement. If this bullish momentum continues unchecked, the next resistance lies at the 78.6% level around $4.40. Should the rally remain relentless, price could even retest its previous peak near $5.30.

After reading Arogosta post, it is possible for AEM can climb the wall of Wars to $4.40, followed by $5 and then $5.30.

Is this a joke, a dream or reality? Let' s see how the drama unfolds this week.

JurongW ( Date: 20-Mar-2026 19:22) Posted:

|

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

Aggressively Expanding Margins, and this translates to Already Expecting Millions !

Supreme

Yells: "BBs never say why when they buy; never tell when they sell"

x 0

Alert Admin

FROM THE BLACK MARKET' S NOTICE BOARD

There&rsquo s a famous saying in the Black Market:

It isn' t just in WHO is buying, but WHAT they are buying.

" A Generational Pivot: The TCS Evolution. While AEM' s expanding clientele portfolio of Big Tech partnerships in well-documented, the true transformation lies deeper. The segment shift isn' t merely in WHO is buying, but in the fundamental nature of WHAT they are buying: moving from standalone hardware to mission-critical, integrated Test Cell Solutions (TCS)."

The Test Cell Solutions (TCS) segment isn' t just a business unit for AEM it' s their " generational pivot." It marks the transition from being a provider of standalone machines to becoming the indispensable architect of the entire semiconductor testing environment.

Here is the breakdown of why TCS is the secret (magic) sauce defining AEM' s future:

1. What exactly is TCS?

a) TCS is an integrated cell that combines three critical components into one automated process: Active Thermal Control (ATC), System Level Test (SLT), High Parallelism Automation.

a) Think of a " Test Cell" as a complete, integrated ecosystem. Instead of just selling a handler (the robot that moves chips), TCS provides the full stack: the thermal control systems, the high-speed electronics, the contactors (sockets), and the software that manages the " handshake" between the chip and the tester. It' s a turnkey laboratory-in-a-box.

2. Is it AEM' s forte and niche?

a) Absolutely. AEM is considered one generation ahead of its competitors in the SLT space. Their specific niche is solving the thermal challenge of AI chips.

b) While competitors often specialize in just one component (like only sockets or only testers), AEM' s forte is System Level Test (SLT) integration. They own the niche of " Massively Parallel Testing," where hundreds of complex chips are tested simultaneously under extreme thermal conditions. No one else integrates these moving parts as seamlessly at scale.

3. The Margin Secret from the Magic Sauce

a) AEM' s value proposition is shifting. By 2026, the Test Cell Solutions (TCS) segment is expected to represent 70% of total revenue (up from 63% in 2025), effectively transitioning the company from a hardware builder to a high-margin tech partner. This segment leverages proprietary PiXL thermal technology, an essential requirement for testing the next generation of high-power AI chips.

b) The Recurring Revenue Model: The magic sauce is the shift from one-time machine sales to a high-margin consumables model. Every chip design change requires new, specialized contactors and change-over kits. AEM isn' t just selling the " printer" they have become the exclusive provider of the " high-precision ink" required for the life of the machine.

4. How important is it to current and future clients?

a) As chips get smaller and more powerful (think AI and 5G), they generate immense heat and are prone to infant mortality (failing early). Clients can no longer rely on simple tests they need the deep, environmental stress testing that TCS provides. For a client like Intel or next-gen AI chipmakers, TCS is the insurance policy that their $1,000 chips won' t fail in a server farm.

b) Future Necessity: As chips move toward 2.5D/3D packaging (stacking multiple chips on top of each other), the chance of a hidden defect increases. Testing each layer individually is too expensive. Big tech companies must move to System Level Testing (SLT) to catch these defects, and AEM currently owns the most advanced automated factory-ready version of this tech.

5. Why it is difficult to copycat?

a) You can' t the just copy a test cell. It requires a rare marriage of mechanical engineering, thermal science, and high-speed signal integrity. AEM has decades of proprietary data on how materials behave at -40° C to +150° C while carrying massive electrical loads. That institutional knowledge is a massive barrier to entry.

b) AEM holds a deep portfolio of patents protecting their thermal control and handler designs. Even if a competitor builds a similar machine, AEM' s software and hardware are already baked into the manufacturing lines of its biggest customers, making it very expensive and risky for a client to switch

6. Keeping the Magic Sauce secret

a) What is a Plan of Record (POR)?: It means the customer has designed their entire manufacturing floor around AEM' s machines. Once AEM is written into a customer' s Plan of Record, they are locked in for the entire lifecycle of chip generation (usually years). Switching vendors would require re-validating the entire testing process, costing millions in delays.

b) The AI Anchor Lock-in: As AI chips become more complex, AEM' s software becomes the brain of the factory floor. This creates a digital lock-in the more data the TCS collects, the better it gets at predicting failures, making AEM' s ecosystem impossible to rip out without blinding the manufacturer.

Sticking with AEM: Brewing Long-Term Gains that keep flowing

a) In short, TCS transforms AEM' s revenue from a lumpy hardware business into a sticky, recurring stream. It' s the " Nespresso Model" of the semiconductor world: the world-class machine gets you through the door, but the high-margin, proprietary pods (the consumables and integration services) keep the revenue flowing for a generation.

b) When analysts like JPMorgan or DBS look at a company, they love " sticky" revenue.

~ With 70% of revenue tie to TCS, AEM is no longer just selling a product they are selling an indispensable service.

~ As AI chips get more powerful (and hotter) in 2027 and 2028, the demand for this specific thermal niche will only intensify.

Essentially, AEM has found the one thing AI chip makers must have to ensure their chips don' t fail, and they' ve patented it.

Supreme

Yells: "BBs never say why when they buy; never tell when they sell"

x 0

Alert Admin

didn' t see that coming! Welcome on board anyway, ah tong....

Even mini man is getting into the act

https://www.minichart.com.sg/2026/03/20/aem-stock-analysis-ai-tailwinds-customer-growth-and-upside-potential-in-2024-2027-12/

https://simplywall.st/stocks/sg/semiconductors/sgx-awx/aem-holdings-shares

https://sgwealthbuilder.com/category/stocks/

Supreme

x 0

Alert Admin

AEM: Comeback is Real As It Sweeps Intel Award, Stock Skyrockets, DBS Raises Target Price Again

22 March 2026

|

After several years of struggling with operational issues, including litigation, and a semiconductor downcycle, AEM Holdings is finally catching its second wind. AEM is in the midst of a dramatic turnaround, especially since the release of its robust FY25 results in February, evidenced by a surging share price&mdash up approximately 138% year-to-date (from $1.74 to $4.10). Now, there' s a prestigious nod from its most critical customer, Intel Corp. AEM (market cap: S$1.3 billion) announced it has received the 2026 Intel EPIC Supplier Award, the highest tier of recognition within Intel&rsquo s global supply chain. This award, given to only 41 suppliers out of thousands, recognises AEM for its " excellence in quality, technology innovation, operational performance, and continuous improvement."

|

DBS Group Research published a bullish update on March 20, reinforcing the " Buy" case for the stock.

DBS raised its target price to $4.60 (up from $3.30), citing a " valuation uplift" driven by AI tailwinds and successful customer diversification.

That is now the most bullish target, while the targets of other analysts have been surpassed by the stock:

|

Brokerage |

Analyst |

Previous TP |

New TP |

|

DBS |

Amanda Tan |

S$3.30 |

S$4.60 |

|

CGS Int' l |

William Tng |

S$1.85 |

S$3.14 |

|

Maybank |

Jarick Seet |

S$1.49 |

S$2.84 |

|

UOB Kay Hian |

John Cheong |

S$1.51 |

S$2.65 |

Key Takeaways From DBS Report:

1. Technological Lead in System Level Test (SLT)

DBS analyst Amanda Tan notes that AEM remains approximately one generation ahead of its competitors in SLT solutions.

As chips become more complex (thanks to 5G, AI, and IoT), the industry requires more intensive testing. AEM&rsquo s " technological superiority" positions it to capture the lion' s share of this growing spend.

2. The Intel " 4nm" Transition

A major driver for AEM is Intel&rsquo s shift toward more advanced nodes.

Intel is currently preparing for the mass production of 4nm chips. These smaller, more complex nodes require significantly longer test times, which directly translates to:

Stock investment guide

-

Higher demand for AEM&rsquo s high-density modular test (HDMT) handlers. -

Increased revenue from consumables due to higher wear and tear during longer test cycles.

3. Rapid Customer Diversification

AEM is no longer just " the Intel play." DBS highlights that traction with new customers is gaining steam:

-

AI Fabless Customers: Revenue from this segment is expected to more than double in FY26.

-

Memory Customers: Orders for final test handlers are on track, with initial revenues expected in late FY26 ahead of a major production ramp in 2027.

4. The " Hyperscaler" Opportunity

DBS points to a massive, untapped upside: Big Tech " hyperscalers" (cloud providers) are increasingly designing their own silicon.

Currently, many use inefficient lab-style tools for production testing.

AEM&rsquo s high-parallel test equipment is " favourably positioned" to replace these inefficient systems, providing a potential earnings catalyst not yet fully priced into the stock.

DBS forecasts a powerful earnings recovery, with net profit expected to jump from $17.1m in 2025 to $45.1m by 2027. While a residual legal overhang and relatively small market cap keep AEM at a slight discount to global peers like Advantest and Teradyne, DBS believes the risk-reward remains " skewed to the upside." Valuation of global test peers:

|

|||||||||||||||||||||||||||||||||||||

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

https://www.tiktok.com/@ronan_wu/video/7094536478805560603?is_from_webapp=1& sender_device=pc& web_id=7506771443117721095

For who those miss the boat like me, this song will be more suitable.

https://www.tiktok.com/@yaki_ling/video/7512689778664459528?is_from_webapp=1& sender_device=pc& web_id=7506771443117721095

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

Supreme

Yells: "BBs never say why when they buy; never tell when they sell"

x 0

Alert Admin

I was observing my previous post (below) and in less than 2 hours, it garnered more than 200 views! My other threads couldn' t even get 200 views in one single day........

Which means there seems to be a lot of interest in this stock, so I have to be careful and responsible in what I post! Otherwise, a lot of newbies and less experienced investors might be misled, if they follow the wrong sentiments of the stock.

The true highlight of yesterday' s news developments was actually the confirmation of the Intel " Epic Supplier" award, a move previously speculated upon by the black market. However, retail sentiment was largely distracted by announcement of JPMorgan' s purchase of AEM' s shares and its subsequent emergence as a substantial shareholder. I was also caught up in this retail euphoria and made posts relating to it, but it is important to clarify that this could send the wrong signal.

JPMorgan' s purchase does not represent a proprietary trade using their own capital. Instead, they are facilitating trades on behalf of institutional clients, acting as a nominee and custodian ~ similar to other brokers like UOB Kay Hian, CGSI. Therefore, their " purchase" does not necessarily mean the bank is taking a larger directional stake conversely, a future " sale" may not indicate liquidation, though both are easily misinterpreted by new and seasoned traders alike. This shouldn' t be treated with great significance, but as normal transactions.

We should instead refocus on the Intel award as a primary catalyst. The resulting publicity and goodwill serve as a powerful testimony to attract other Big Tech firms. This could potentially transition companies like Meta and Nvidia from indirect beneficiaries into full-scale anchor clients for AEM. Also, we should be more excited with AEM' s capture of a second major AI/HPC client which is expected to contribute to the bottom line by the end of this fiscal year. These factors should bolster earnings over the next two quarters and provide upward momentum for the stock price. I would not be surprised to see a formal upward revision in revenue guidance, which could further act as the next major catalyst. Remember June last year, AEM experienced a 14.52% share price jump in a single day following the company' s announcement that it was raising its revenue guidance for the first half of FY2025? Imagine, if they do it again before the next half yearly results!

aragosta ( Date: 21-Mar-2026 11:32) Posted:

|

Supreme

x 0

Alert Admin

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

aragosta ( Date: 21-Mar-2026 11:32) Posted:

|

Supreme

Yells: "BBs never say why when they buy; never tell when they sell"

x 0

Alert Admin

JPMorgan Adjusted Transaction Log

REPORTED IN SGX FILING

Date of acquisition of or change in interest: 16 March 2026

Purchase 555,000 units at average price of SGD 3.35 per unit via market transaction.

Increase of 77,400 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.183% (up from 4.982%)

Date of acquisition of or change in interest: 17 March 2026

Sale of 910,200 units at average price of SGD 3.53 per unit via market transaction

Increase of 22,300 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 4.901% (down from 5.183%)

YET TO BE REPORTED IN SGX FILING

Date of acquisition of or change in interest: 18 March 2026

Purchase 1,225,400 units at average price of SGD 3.72 per unit via market transaction.

Decrease of 15,800 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.286% (up from 4.901%)

Note: Substantial shareholders have 2 business days to report changes therefore, a transaction occurring on 18 or 19 March

might not appear on the SGX central portal until the following Monday or Tuesday. The above UNDISCLOSED info came from

the coffee shop uncles, which I overheard while having my kopi-o sui tai. Please do not shoot me, if I overheard wrongly hor.......

IMPORTANT TO NOTE! The explicit mention of the Prime Brokerage Agreement in these filings confirms these are client-driven

activities and are not proprietary trades by JPMorgan (using their own cash). They are facilitating the trades of institutional clients,

likely hedge funds, or high-networth clients (I kept telling you this until I got no saliva! Yet gongkias newbies would panick when

they see a sales by JP Morgan). JPMorgan Chase & Co. typically files as a Substantial Shareholder because the aggregate of its clients' holdings (for which it acts

as a nominee/custodian) exceeds the 5% threshold.

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

JP Morgan - Sale of 910,200 shares at $3.53 on 17 Mar

https://links.sgx.com/1.0.0/corporate-announcements/2NY8C8LXMHPY7JH7/879026__eFORM3V2.pdf

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

For those who believe in AEM' s growth story and are already on board, this high-energy, high-tempo music could lift your spirits even further.

ENG SUB 動 畫 【 仙 逆 】 王 林 問 鼎 插 曲 《 何 惜 一 戰 》 完 整 版 - 張 申 騁 「 燃 」 | Renegade Immortal OST (EP 121 ED)

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

If shares price is $8, forward PE will be approximately 55times base on FY27 projected earnings. This implies market is pricing aggressive growth expectations.

If earnings growth slows or results underperform, such a high multiple leaves little margin of safety.

Trade‑ offs

Bull case - Investors may justify the premium if they believe AEM technology edge (eg in test equipment for advanced chips) will deliver outsized growth.

Bear case - Valuation looks stretched, especially if Q1 results trigger sell on news behavior after a parabolic run.

Takeaway

A forward P/E of 55x is objectively high for AEM compared to UMS, Frencken, and global peers. It reflects strong optimism but also raises the risk of sharp corrections if growth expectations are not met.

https://www.dbs.com/insightsdirect/api/s3/dbs-buffer/article_attachment/20260320/07-35-27_SG%20Tech%20-%2020mar2026.pdf

Elite

Yells: "Earnings give weight, Chart give wings"

x 0

Alert Admin

AEM has surged past the 61.8% Fibonacci retracement. If this bullish momentum continues unchecked, the next resistance lies at the 78.6% level around $4.40. Should the rally remain relentless, price could even retest its previous peak near $5.30.

Such a move could unfold before Q1 results, setting up a potential double top formation. A double top is a classic reversal pattern, signaling that an uptrend may be exhausted and a downtrend could follow. Once results are released, the market may react with a &ldquo sell on news&rdquo response, especially if the stock has already run too far, too fast.

For those who missed the initial rally but believe in Arogosta&rsquo s story, patience is key. Wait for confirmation from a shooting star, evening star, or other bearish candlestick signals before considering entry.

Remember: no stock climbs forever. Overbought conditions eventually demand a pause. On the extreme side, the 161.8% Fibonacci extension projects a price close to $8.

This is purely a technical perspective treat it as coffeeshop talk, shared for entertainment rather than investment advice.

Member

x 0

Alert Admin