very nice 74 75

hope today is a good day

noobnub ( Date: 06-Aug-2024 10:18) Posted:

|

Manulife US REIT&rsquo s new management &lsquo focusing on the right dispositions&rsquo : RHB

The manager of Manulife US REIT (MUST), led by new leaders who were appointed June 30, is focusing on the right dispositions and deleveraging, says RHB Bank Singapore analyst Vijay Natarajan.

John Casasante is the new CEO and CIO of the manager. Mushtaque Ali, from sponsor Manulife, is the new CFO of the manager.

MUST&rsquo s operational performance for 1HFY2024 ended June was in line, says Natarajan, with a &ldquo glimmer of a sign&rdquo that market conditions are stabilising. US office leasing volumes are starting to point to a pick-up, with some normalisation in return-to-office trends.

In an Aug 6 note, Natarajan maintains his &ldquo trading buy&rdquo call on MUST with an unchanged target price of 12 US cents. A &ldquo trading buy&rdquo call by RHB means MUST&rsquo s share price may exceed 15% over the next three months, however the longer-term outlook remains uncertain.

Following an Aug 5 briefing for analysts and media, Natarajan says MUST&rsquo s disposition plan is on track, with three unidentified assets on the market.

Management has not shared the names of these assets due to the sensitive nature of the transactions, but has kept its target of US$100 million in asset divestments by the year-end.

That said, this is later than initially announced management had previously indicated that the asset disposals should be complete &ldquo by 2QFY2024 or 3QFY2024&rdquo .

A key consideration for disposition will be the need for incremental capital to be spent on the asset versus potential returns. &ldquo MUST is willing to sell assets at a discounted price if necessary. There has been a noticeable increase in purchasers&rsquo interest for its assets, from both institutional and high-net-worth investors,&rdquo notes Natarajan.

In 2QFY2024, MUST&rsquo s occupancy was stable q-o-q at 78.4% compared to 78.7% in the previous quarter.

Leasing momentum remains positive with 428,000 sq ft of leases executed in 1HFY2024, despite the challenging conditions in some of MUST&rsquo s submarkets, says the manager. Representing 8.5% of portfolio net lettable area (NLA), these leases have a long weighted average lease expiry (WALE) of 7.3 years.

The bulk of leases signed in 1HFY2024 comprised renewals (75.8%), while new leases made up 13.8%, and expansions the remaining 10.4%.

The largest lease signed was for Amazon, the anchor tenant at 10 Exchange Place (Exchange) in Jersey City, New Jersey, and one of MUST&rsquo s top five tenants. Prior to the renewal, its lease was previously due to expire in April 2025.

Rent reversion for the 1HFY2204 leases was at negative 10.6%. Natarajan believes this was dragged down by the Amazon lease extension.

According to management, the REIT&rsquo s leasing pipeline remains healthy, at 1.4 million sq ft, with 80% of this at the proposals stage. &ldquo Management expects the easing of the labour market to result in a higher return-to-office rate, which should boost its leasing momentum,&rdquo writes Natarajan.

Adjusted to exclude Tanasbourne and Park Place, which were sold in April 2023 and December 2023 respectively, MUST&rsquo s same-store 1HFY2024 gross revenue was down 8.1% y-o-y while net property income (NPI) was down 16.7% y-o-y.

This was due mainly to the exit of a key tenant, TCW, at the start of the year, and downsizing at The Children&rsquo s Place, another key tenant.

NPI margins, however, came in below Natarajan&rsquo s expectations on higher leasing commissions and higher insurance premiums.

Around 80% of MUST&rsquo s debt is hedged, and its new policy is to keep 50%-80% of debt hedged on the expectation of interest rate cuts.

As at June 30, MUST&rsquo s unencumbered gearing ratio and aggregate leverage ratio held steady at 60.0% and 56.3%, from 59.7% and 56.7% respectively as at March 31.

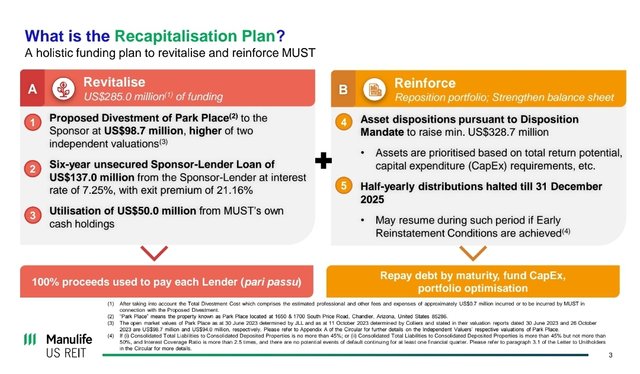

MUST has halted distributions until end-2025 as it rolls out its recapitalisation plan to address rising gearing and falling valuations.

Natarajan cut his NPI margin assumptions for FY2024 and FY2025 on the back of higher opex and tenant incentives resulting in 12% and 11% lower available distributable income respectively. He also expects no distribution payments until FY2026.

later take profits happy until i pee on my pants haha

noobnub ( Date: 06-Aug-2024 08:55) Posted:

|

now waiting to go above my price to take small profits huat ah

noobnub ( Date: 05-Aug-2024 09:45) Posted:

|

😅

Stocky901 ( Date: 05-Aug-2024 18:29) Posted:

|

Manulife US REIT same-store NPI falls 16.7% y-o-y in 1HFY2024 manager &lsquo marketing three properties for sale&rsquo

Manulife US REIT (MUST) has posted income available for distribution (DI) of US$22.9 million ($30.38 million) for 1HFY2024 ended June 30, 39.8% lower y-o-y. That said, MUST has halted distributions until end-2025 as it rolls out its recapitalisation plan to address rising gearing and falling valuations.

In an Aug 5 announcement, the manager of the US office REIT blames higher finance expenses incurred due to higher interest cost from 1HFY2023. From July 2023, the manager elected to receive payment of 100% of its base fee and property management fee in cash. To provide a like-for-like comparison, the manager offers an adjusted DI in the prior year period to reflect the manager&rsquo s base fee of US$3.8 million and property management fee of US$2.5 million being payable in cash instead of units.

Hence, adjusted DI only fell 27.8% y-o-y, according to the manager. Adjusted DI per unit is down 27.5% y-o-y to 1.29 US cents.

In the six months till June 30, MUST recorded gross revenue of $86.7 million, down 12.9% y-o-y and net property income (NPI) of $42.8 million, down 22.7% y-o-y. These were due to lower rental and recoveries income from higher vacancies, which rose 6.7% y-o-y across the portfolio and higher property operating expenses, say the manager.

Adjusted to exclude Tanasbourne and Park Place, which were sold in April 2023 and December 2023 respectively, same-store 1HFY2024 gross revenue was down 8.1% y-o-y while NPI was down 16.7% y-o-y.

Gearing stable

As at June 30, MUST&rsquo s unencumbered gearing ratio and aggregate leverage ratio held steady at 60.0% and 56.3%, from 59.7% and 56.7% respectively.

Interest coverage ratio fell to 2.2 times from 2.3 times as at March 31, while weighted average debt maturity shortened slightly to 3.0 years from 3.2 years over the same quarter.

To mitigate cash flow volatility resulting from interest rate movements, MUST targets to maintain an optimal hedge ratio of between 50% and 80%. The percentage of hedged/fixed rate loans remained at 80.2% as at June 30.

Leasing momentum ' positive'

In 2QFY2024, MUST&rsquo s occupancy was stable q-o-q at 78.4% compared to 78.7% in the previous quarter.

Leasing momentum remains positive with 428,000 sq ft of leases executed in 1HFY2024, despite the challenging conditions in some of MUST&rsquo s submarkets, says the manager. Representing 8.5% of portfolio net lettable area (NLA), these leases have a long weighted average lease expiry (WALE) of 7.3 years.

The bulk of leases signed in 1HFY2024 comprised renewals (75.8%), while new leases made up 13.8%, and expansions the remaining 10.4%.

These tenants include &ldquo creditworthy&rdquo companies from diverse sectors including technology, retail, financial and healthcare, contributing further to a resilient tenant base, says the manager. The largest lease signed was for Amazon, the anchor tenant at 10 Exchange Place (Exchange) in Jersey City, New Jersey, and one of MUST&rsquo s top five tenants. Prior to the renewal, its lease was previously due to expire in April 2025.

Amazon occupies 129,000 sq ft, or about 17% of the NLA, at the 30-storey Exchange office tower and the 3+ years lease renewal comes with modest tenant concessions and no early termination options.

The average rent reversion of leases signed in 1HFY2024 was negative 10.6% and majority (11 out of 17) of the office leases were signed at above market rents.

As at end-June 2024, the portfolio WALE lengthened to 4.7 years, from 4.3 years three months ago.

There is approximately 1.4 million sq ft in MUST&rsquo s leasing pipeline across its portfolio. However, the leasing environment remains &ldquo challenging&rdquo and the manager says it is &ldquo strategically prioritising leases that create liquidity and maximise value for MUST and its unitholders over chasing higher occupancy&rdquo .

MUST&rsquo s lease expiry profile has 14.7% of leases by NLA expiring in 2HFY2024 and 9.6% expiring in FY2025.

Asset sales

MUST&rsquo s unitholders voted at an EGM in December 2023 to approve a recapitalisation plan and save the REIT from liquidation. One of the three resolutions passed provides the manager and lenders with the authority to divest &ldquo non-core&rdquo , &ldquo Tranche 1&rdquo properties, albeit at a minimum sum of US$328.7 million.

As at the previous results briefing, four Tranche 1 assets in MUST&rsquo s portfolio are potentially up for sale: Centerpointe, Diablo, Figueroa and Penn. The manager said then that it targets asset sales of some US$100 million by 2Q2024 or 3Q2024.

Among its portfolio of 10 assets, Tranche 1 assets account for 66% of the expiries in the next 1.5 years, says the manager in the Aug 5 announcement.

Figueroa, a 35-storey Class A office building in Downtown Los Angeles that has been in the portfolio since its IPO in May 2016, saw the largest decline in NPI, falling 85% y-o-y in 1HFY2024 to US$0.7 million. The manager blames the exit of US asset management firm TCW Group, whose lease for some 189,000 sq ft at Figueroa expired on Dec 31, 2023.

Meanwhile, there are lease expiries in 2024 for the Tranche 3 assets, Phipps and Michelson, in respect of which the manager is expecting a renewed and partial backfill respectively.

MUST&rsquo s top 10 tenants have a WALE of 6.8 years by NLA and there are no significant termination options in leases with these tenants within the next five years.

&ldquo Overall, its tenant base is well-diversified across more than 20 trade sectors with no single tenant contributing more than 5.1% of gross rental income,&rdquo says the manager.

John Casasante, CEO and CIO of the manager, says the REIT is marketing &ldquo three of our properties for sale&rdquo . &ldquo Our strategic focus for MUST centres firmly on improving returns for unitholders through a strategic disposition plan, optimising leasing and business operations, and exercising prudence in capital and liquidity management. The execution of our recapitalisation plan remains a top priority, and we have commenced the process to sell three carefully selected assets that we believe would attract liquidity amid the challenging environment.&rdquo

Casasante, who was appointed on June 30, adds: &ldquo We have also commenced high-level discussions with potential off-market buyers for other targeted assets in the portfolio. The level of interest from prospective buyers has been encouraging, and we are optimistic that we should be in a position to achieve the milestones of the master restructuring agreement.&rdquo

stock market collapsing...real office market already collapsed.. .now sitll on painful slow road to recovery, at least for KORE' s assets. PRIME not sure (waiting for results). MUST' s asset still dead. Real assets' s fate don' t change as fast as stock market lah.. chill :)

US market collapsing. US Office cham

added 75

noobnub ( Date: 05-Aug-2024 09:32) Posted:

|

bought 76 try my luck for 1 or 2 pips

Results out... still lack lusture occupany dipping to 78.4% (from 78.7%) and mgt still claim 3 assets on track to be divested.. .stil in ICU

Proposed changes to leverage limits for S-Reits make sense given Manulife US Reit&rsquo s experience

ON THE final trading day of 2022, the manager of Manulife US Real Estate Investment Trust (MUST) put out an announcement headlined: &ldquo Aggregate leverage to remain within regulatory limit based on updated asset valuations&rdquo .

The announcement was, in fact, a warning that MUST&rsquo s aggregate leverage as at end-2022 had risen to 49 per cent because of a double-digit percentage decline in the valuation of its property portfolio.

Singapore-listed real estate investment trusts (S-Reits) are subject to an aggregate leverage cap of 45 per cent, but they are allowed to raise their aggregate leverage to 50 per cent if they have an interest coverage ratio (ICR) of at least 2.5 times.

As MUST was projected to have an ICR of 3.1 times at end-2022, its aggregate leverage was within the regulatory limit, its manager said in the announcement.

For investors, MUST&rsquo s compliance with the regulatory cap on leverage at that point was arguably far less important than the fact that the US commercial property market was likely to continue deteriorating.

Indeed, the experience of MUST over the past couple of years might be a useful case study in understanding why the proposed amendments to the leverage requirements for S-Reits unveiled by the Monetary Authority of Singapore (MAS) last week make a lot of sense.

MAS wants to simplify the current leverage requirements by subjecting all S-Reits to a minimum ICR of 1.5 times, and an aggregate leverage cap of 50 per cent.

MAS also wants S-Reits to perform and disclose sensitivity analyses on the impact that changes in their Ebitda (earnings before interest, tax, depreciation and amortisation) and interest rates would have on their ICRs.

On the face of it, these proposals are a loosening of the current rules. The S-Reits with the most to gain are those with aggregate leverage ratios currently approaching 45 per cent, and ICRs plumbing towards 1.5 per cent.

Maintaining balance sheet strengths as S-Reits average 39% gearing

Will the proposed rule changes undermine market discipline? Will they promote dangerous risk-taking?

Regulations versus lenders

The rule changes are being proposed at a time when interest rates are more likely to fall than rise, and the whole S-Reit sector seems poised to turn the corner.

The experience of MUST over the past couple of years also suggests that the regulatory limits on aggregate leverage have not been the most potent disciplining force for S-Reits.

As at Jun 30 last year, MUST suffered a further double-digit percentage decline in the valuation of its property portfolio, which pushed its aggregate leverage up to 57 per cent. MUST&rsquo s manager said this was not considered a breach of the aggregate leverage limit as it was due to circumstances beyond its control.

The manager was, however, forced to take remedial action because MUST had, at that point, also breached a loan covenant requiring it to maintain a ratio of unencumbered debt to unencumbered assets of not more than 60 per cent.

This resulted in a cross default of MUST&rsquo s interest rate swaps, which put it at risk of having to bear higher interest costs. This, in turn, put MUST in danger of eventually breaching another loan covenant that required it to maintain an ICR of more than two times.

At the mercy of its lenders, MUST&rsquo s manager hammered out a deal late last year that involved the immediate repayment of US$285 million of debt with the help of its sponsor group, and a commitment to raise at least US$328.7 million through asset sales.

MUST&rsquo s bankers extended the maturities of its loans by one year. They also temporarily raised the ceiling for MUST&rsquo s unencumbered gearing from 60 per cent to 80 per cent, and lowered the floor for its ICR from two times to 1.5 times.

With the simplified leverage requirements MAS is proposing, investors may begin to focus more closely on the margin of safety that S-Reits have in satisfying their loan covenants. As long as lenders maintain their standards, this could well be a positive development for the S-Reit sector.

Merits of sensitivity analyses

By the time MUST&rsquo s manager made its announcement about the double-digit percentage decline in the valuation of its portfolio on Dec 30, 2022, it was clear that the deteriorating commercial property market in the US posed a major problem.

Only a few weeks before, the manager had announced the appointment of Citigroup Global Markets Singapore as its financial adviser in relation to a strategic review.

The manager also subsequently said in its 2023 first-quarter operational update that it had attempted three asset dispositions between April and November 2022, but that the deals were scuppered by rising interest rates and potential buyers being unable to obtain funding.

In such a dynamic market environment, investors would naturally be inclined to speculate on how an S-Reit&rsquo s balance sheet and credit profile might be affected. This is where the proposed sensitivity analyses could be useful.

MAS is proposing S-Reits produce sensitivity analyses on the impact of changes in Ebitda and interest rates on their ICRs.

MAS wants S-Reits to disclose these sensitivity analyses in their interim financial statements and annual reports. At least one scenario should assume a 10 per cent decrease in Ebitda and a 100 basis point increase in interest rates.

This could be an effective way for S-Reit managers to provide investors with information in a timely manner.

Given the experience of MUST, MAS should perhaps also require S-Reits to provide sensitivity analyses on the impact of changes in the valuation of their largest properties on their aggregate leverage.

These various sensitivity analyses should perhaps also be required to indicate how bad things would need to get for loan covenants to be breached.

With a better sense of how the capital structure and debt-servicing ability of S-Reits might change through an economic cycle, investors would have a deeper understanding of the risks they face.

wait for the first ACTUAL cut then say ^_^

piscesmonkey ( Date: 01-Aug-2024 04:28) Posted:

|

Investors saw Powell?s comments as clearly setting the stage for a reduction in borrowing costs at the Fed?s Sept 17-18 meeting, just seven weeks shy of the Nov 5 US elections.

Chair Powell gives the September rate cut signal traders were hoping for

Tonight rate cuts? Or sep? Since aug no fed meeting.

Breakout 82 so MUST can move up 90.

yap this one.