Collected some earlier on 81/815 for investment...

JurongW ( Date: 11-Apr-2026 15:49) Posted:

|

UIB has broken out from it descending channel, probably on its way to test its prior high of 84.

Well done to those who had the conviction to buy when there was a pull back to ~80

Well done to those who had the conviction to buy when there was a pull back to ~80

The main issue with Lendlease Global Commercial REIT wasnt failure due to COVID occupancy, but dilution from equity fundraising and acquisitions done at depressed unit prices, i.e. dilution of existing shareholders.

The COVID period wasnt the structural driver of the REIT&rsquo s underperformance. If you look at Lendlease REIT underlying business itself, the asset performance remains relatively resilient even today. Yet the unit price has not recovered, because other issues were gradually revealed to shareholders over time.

So the key driver wasn&rsquo t an occupancy collapse, it was capital management (equity issuance and acquisition timing), which led to persistent DPU dilution even as operational performance normalised.

This is also why a name like Boustead REIT may look fine on paper today (just as Lendlease REIT, Prime US REIT, etc. once did), but prices can remain depressed until management proves its capital allocation track record over time.

Which leads to a broader point: IPO price is not a fixed support level nor a fixed fair value anchor. True fair value can be higher or lower over time.

coco66 ( Date: 01-Apr-2026 08:56) Posted:

|

Different people have different return targets, hold period environments and tolerances for share price volatility which is why I try to avoid giving specific buy/hold/sell comments. But I agree with the way you are looking at it.

HVRRVH ( Date: 11-Apr-2026 14:56) Posted:

|

Price action can be unpredictable.

When we dont buy and wait fo it to go down to buy on the cheap, it goes up instead, or

When we start buying abit, stock continue to go up and we wish more shares could have been earlier, or

When we start buying abit, stock went down instead, and this give us a chance to DCA.

Just trust your judgement and decision making.

Treat my chart analysis for entertainment purpose. I use this opportunity to practise and hone my charting skills.

When we dont buy and wait fo it to go down to buy on the cheap, it goes up instead, or

When we start buying abit, stock continue to go up and we wish more shares could have been earlier, or

When we start buying abit, stock went down instead, and this give us a chance to DCA.

Just trust your judgement and decision making.

Treat my chart analysis for entertainment purpose. I use this opportunity to practise and hone my charting skills.

HVRRVH ( Date: 11-Apr-2026 15:34) Posted:

|

Personally it' s ok for me to buy at current price, and if price drop, can buy a bit more. Similar thing happened to the parent Boustead where after I first bought, it keep dropping for the next 3 to 4 years before trending up. I am trying to say it is hard to time the bottom. Everyone wish they could.

JurongW ( Date: 11-Apr-2026 15:11) Posted:

|

Yes there are risks, chiefly from high interest rate but SSB right now is still low 2% after coming down from high of 3+%. It' s hard to see saving rates of 4 to 5% even if Fed rate going higher to 5%. That said, wary of high interest rate environment is exactly the reason why I am relunctance to add to my reit portfolio to beging with but in UIB I see value. It is better to take a position now because even if the price come down, there is always room to add. I have been cutting Lendlease so as to maintain certain amount of reit portfolio and I will continue to adjust in the same direction. If Lendlease hit $0.65, perhaps it is time for me to let go of it all.

I think in this current environment where interest rate directions are very uncertain you have to focus on relative valuations to keep yourself grounded and not be caught out by what is happening with the risk free rate. Yes at an absolute level UI REIT is compelling - I think it is the only REIT with Singapore assets except ESR REIT that has a DPU yield above 8% (and ESR REIT is in a much worse spot). But on a relative basis what speaks to me more is the UI REIT / Centurion REIT comparison. One is at S$0.82 and the other at S$1.13. In my mind they should be the same price, whatever that price may be. Therefore I am selling my Centurion REIT shares and buying UI REIT. I see this offering me a 38% upside if the gap closes, on top of the 8% DPU yield.

HVRRVH ( Date: 11-Apr-2026 13:04) Posted:

|

Agree. No reason why UIB can' t trade around $1 with its projected yield. Even if 4% yield, this stock should trade around $1. Intend to add more if the low price persist but time on my side.

Alignment ( Date: 08-Apr-2026 13:57) Posted:

|

Looks like the institutional investors see a bargain and are tucking in

Lendlease is clearly much less resilient compared to industrial REITs like UIB REIT &mdash and Covid already made that very obvious. When the crisis hit, logistics and industrial assets continued operating (and in some cases even saw stronger demand), while retail malls under Lendlease Global Commercial REIT were hit hard by falling footfall, weak tenant sales, and rental reliefs. That&rsquo s the key difference &mdash industrial REITs serve business operations that must continue, while retail depends on discretionary spending that can disappear overnight. On top of that, retail is also facing longer-term pressure from e-commerce and changing consumer habits. So while Lendlease isn&rsquo t &ldquo uninvestable&rdquo , we should recognise that it carries higher cyclicality and structural headwinds compared to industrial REITs &mdash and price that risk accordingly.

During Covid, we saw very clearly why retail REITs like Lendlease Global Commercial REIT are inherently less resilient than industrial platforms like UIB REIT. Industrial assets are part of the economy&rsquo s backbone &mdash warehouses, logistics hubs and data centres that businesses must keep running, even in a crisis. That translates into longer leases, more stable tenants, and income that continues to flow. In contrast, retail REITs depend heavily on footfall, tourism and consumer spending &mdash all of which can disappear almost overnight during a downturn. When sales drop, rents fall, rebates kick in, and vacancies rise. In simple terms, industrial REITs rent to businesses that need to operate, while retail REITs rely on consumers who can simply stop spending. That difference in demand stability is what drives the resilience gap &mdash and it&rsquo s not just a Covid phenomenon, but a structural one going forward.

coco66 ( Date: 01-Apr-2026 08:56) Posted:

|

Ammova asset management bought 4,440,200 shares at $0.813 on 30 Mar

https://links.sgx.com/1.0.0/corporate-announcements/L1ZKHRKPNX82QJ1E/881832__eFORM3V2_AMOVA%20-%202April2026.pdf

Lendlease Reit also IPO at 0.88

IPO price is not a support price

IPO price is not a support price

Don' t FOMO. Don' t rush and be stuck at a higher price.

Give it a few weeks (look at most IPOs).

Give it a few weeks (look at most IPOs).

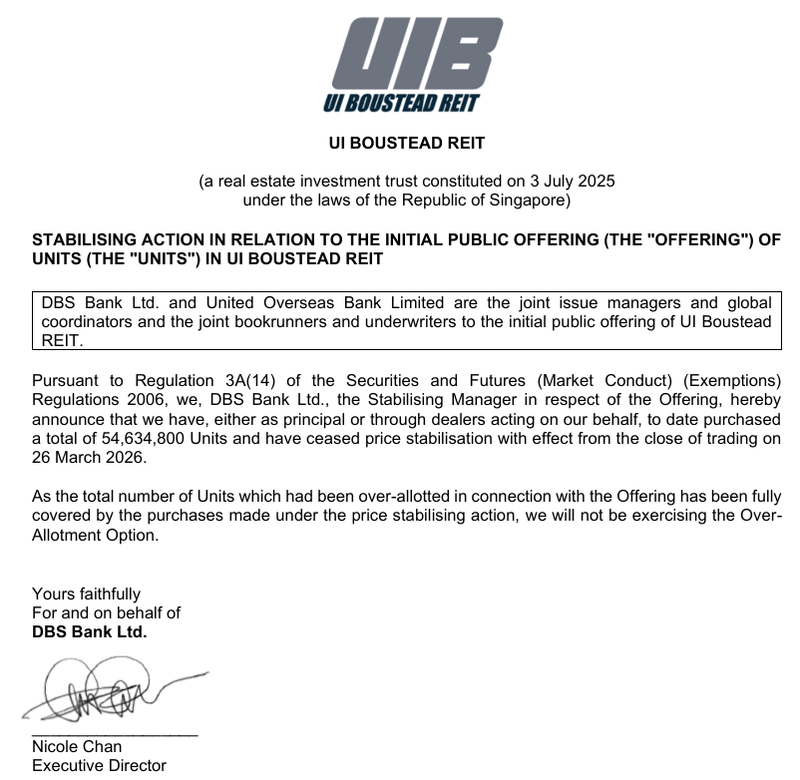

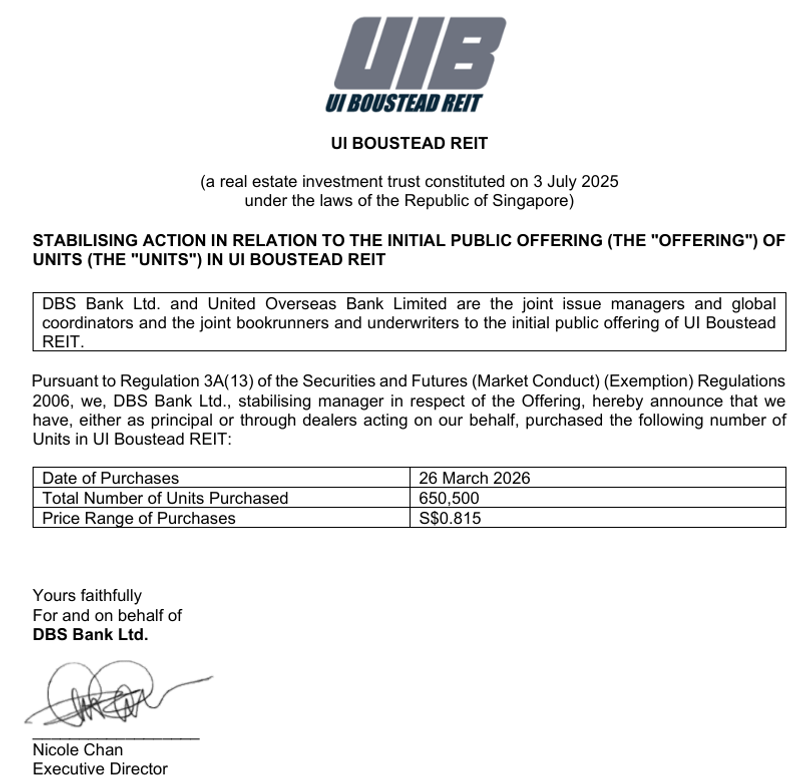

Stabilisation action ends today

minor edits to make it clearer.

Rule of Thumb

Treasury less than or equal to 3%: REITs yielding 6 to 7% look very attractive (spread 3 to 4%).Treasury about 4 to 4.5%: REITs need to yield at least 7.5 to 8% to stay compelling.

Treasury more than or equal to 5%: REITs must push yields above 8.5 to 9% to maintain appeal, otherwise investors may rotate into bonds.

JurongW ( Date: 25-Mar-2026 02:27) Posted:

|

Here&rsquo s the full calibration run for UI Boustead REIT&rsquo s yield across unit prices from S$0.70 to S$1.00, using the projected annual distribution of S$0.06864 per unit (derived from IPO yield 7.8% at S$0.88).

📊 Yield Scenario Table

| Unit Price (S$) | Annual Distribution (S$0.06864) |

Yield (%) | Spread vs. 10Y Treasury (4.4%) |

|---|---|---|---|

| 0.70 | 0.06864 | 9.81% | +5.41% |

| 0.75 | 0.06864 | 9.15% | +4.75% |

| 0.80 | 0.06864 | 8.58% | +4.18% |

| 0.85 | 0.06864 | 8.07% | +3.67% |

| 0.88 (IPO) | 0.06864 | 7.80% | +3.40% |

| 0.90 | 0.06864 | 7.63% | +3.23% |

| 0.95 | 0.06864 | 7.23% | +2.83% |

| 1.00 | 0.06864 | 6.86% | +2.46% |

✅ Interpretation

- Below 80¢ : Yield shoots above 8.5&ndash 9.8%, offering a very wide premium over Treasuries. Attractive, but signals market stress if price falls that low.

- 80&ndash 88¢ : Balanced zone &mdash yield ~7.8&ndash 8.6%, still comfortably above Treasuries.

- 90¢ &ndash $1: Yield compresses to 6.9&ndash 7.6%, narrowing the spread. Still positive, but less compelling versus risk‑ free bonds.

This table shows how price directly calibrates yield attractiveness vs. Treasuries.

For a REIT to remain attractive relative to Treasuries, the key is the yield spread &mdash the difference between the REIT&rsquo s distribution yield and the risk‑ free Treasury yield. Investors typically demand a premium of 3&ndash 4% (sometimes more) to compensate for property market risk, leverage, and liquidity compared to government bonds.

📊 Calibration Example (UI Boustead REIT)

- Projected REIT Yield: ~7.8% at IPO price (S$0.88).

- Current Treasury Yield: 4.4%.

- Spread: 3.4% &rarr still attractive, but not excessive.

🔑 Rule of Thumb

- Treasury &le 3%: REITs yielding 6&ndash 7% look very attractive (spread 3&ndash 4%).

- Treasury ~4&ndash 4.5%: REITs need to yield at least 7.5&ndash 8% to stay compelling.

- Treasury &ge 5%: REITs must push yields above 8.5&ndash 9% to maintain appeal, otherwise investors may rotate into bonds.

✅ Takeaway

For UI Boustead REIT specifically:

- At 7.8% yield, it remains attractive as long as Treasuries stay below ~4.5%.

- If Treasuries rise toward 5%, the REIT would need to trade lower (say ~80¢ , giving ~8.6% yield) to preserve a healthy spread.