SIA current price is driven by sentiments that air travel will recover fast.

Merger of keppel corp will not be so soon. Probably half yr after keppel settles its own deal with temasek

Merger of keppel corp will not be so soon. Probably half yr after keppel settles its own deal with temasek

michaeltan ( Date: 10-Jun-2020 19:44) Posted:

|

Those want to veto the demerger should go and read Ezion' s annual report out just today, esp the Chairman statement.

now on w2

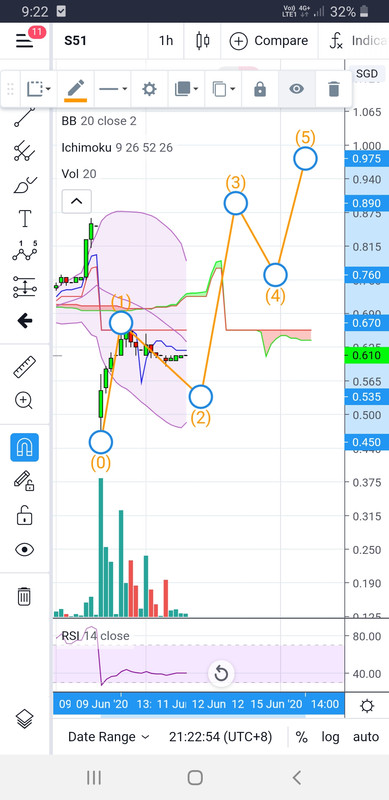

- tgt 535 px hit low 590

if w3 come it will be w3 ext ew

1h chart

- tgt 535 px hit low 590

if w3 come it will be w3 ext ew

1h chart

if it benefits SCI then why not put your words into action and buy SCI? i also think it benefits them so i queuing for SCI, but will vote yes all the same

TA_Expert ( Date: 10-Jun-2020 20:23) Posted:

|

What if the M& A fails, and SembCorp decides to cut off SembMarine or sell it to another party or close it down altogether? SembMarine cannot bleed red ink forever. No company would tolerate continuous red ink without economies of scale to drive a turnaround. Then the value of the shares will plunge.

My call is minority shareholders of SMM should be veto the proposal.

This deal will only serve to benefit the shareholders SCI. That' s why you can see a strong rally in SCI' s price while SMM share price plunged.

I agree with member " better" who will vote aganist the proposal.

This deal will only serve to benefit the shareholders SCI. That' s why you can see a strong rally in SCI' s price while SMM share price plunged.

I agree with member " better" who will vote aganist the proposal.

Djsoul80 ( Date: 10-Jun-2020 16:48) Posted:

|

I meant after the exercise rights convert to mother share. Based on last rights closing price $0.65 + $3.00 = $3.65

Justice888 ( Date: 10-Jun-2020 19:53) Posted:

|

The day after ex right it went above $5

michaeltan ( Date: 10-Jun-2020 19:44) Posted:

|

If you look at it logically, everyone benefits. SMM also gets a richer parent now. The SGD1.5 billion in debt to SCI will also get wiped off the books. Is this not better than the company closing shop, due to being unable to pay back its debts? I do not think SCI would want to support SMM forever either.

It is ok.

I believe Temasek who is the major share holder for both must have a deep study and support the demerger exercise.

Not be suprised the price may go up to $0.40 after ex-right. Look at SIA, many predicted after ex-right to be $3.60 to $3.80 but now $4.35?

Don' t forget another catalyst of merger with KOM card in play.

I believe Temasek who is the major share holder for both must have a deep study and support the demerger exercise.

Not be suprised the price may go up to $0.40 after ex-right. Look at SIA, many predicted after ex-right to be $3.60 to $3.80 but now $4.35?

Don' t forget another catalyst of merger with KOM card in play.

Djsoul80 ( Date: 10-Jun-2020 19:24) Posted:

|

Not really, you must look at other benefit that you are to SCI shares.

Suppose buying 1000 SCI shares at $2.10 = $2100 entitled to 4500 SMM shares free. =$2100 -you own 1000 SCI shares + 4500 SMM shares

Suppose buying 1000 SMM shares at $0.61 = $610 + ($1000) ( 5000 shares X $0.20) =$1610 - you own 6000 SMM shares.

Let say after the ex-right is overed.

SMM $0.30 = 6000 X $0.30 = $1800 - Capital gain ( $1800 - $1610 ) = $190

SCI $1.50 = 1000 X $1.50 + (4500 X $0.30 = $1350) = $2850 - Capital gain ( $2850 - $2100 ) = $ 750

Suppose buying 1000 SCI shares at $2.10 = $2100 entitled to 4500 SMM shares free. =$2100 -you own 1000 SCI shares + 4500 SMM shares

Suppose buying 1000 SMM shares at $0.61 = $610 + ($1000) ( 5000 shares X $0.20) =$1610 - you own 6000 SMM shares.

Let say after the ex-right is overed.

SMM $0.30 = 6000 X $0.30 = $1800 - Capital gain ( $1800 - $1610 ) = $190

SCI $1.50 = 1000 X $1.50 + (4500 X $0.30 = $1350) = $2850 - Capital gain ( $2850 - $2100 ) = $ 750

michaeltan ( Date: 10-Jun-2020 18:59) Posted:

|

Not really, you must look at other benefit that you are to SCI shares.

Suppose buying 1000 SCI shares at $2.10 = $2100 entitled to 4500 SMM shares free. =$2100 -you own 1000 SCI shares + 4500 SMM shares

Suppose buying 1000 SMM shares at $0.61 = $600 + ($1000) ( 5000 shares X $0.20) =$1600 - you own 6000 SMM shares.

Let say after the ex-right is overed.

SMM $0.30 = 6000 X $0.30 = $1800 - Capital gain ( $1800 - $1600 ) = $200

SCI $1.50 = 1000 X $1.50 + (4500 X $0.30 = $1350) = $2850 - Capital gain ( $2850 - $2100 ) = $ 750

Suppose buying 1000 SCI shares at $2.10 = $2100 entitled to 4500 SMM shares free. =$2100 -you own 1000 SCI shares + 4500 SMM shares

Suppose buying 1000 SMM shares at $0.61 = $600 + ($1000) ( 5000 shares X $0.20) =$1600 - you own 6000 SMM shares.

Let say after the ex-right is overed.

SMM $0.30 = 6000 X $0.30 = $1800 - Capital gain ( $1800 - $1600 ) = $200

SCI $1.50 = 1000 X $1.50 + (4500 X $0.30 = $1350) = $2850 - Capital gain ( $2850 - $2100 ) = $ 750

Djsoul80 ( Date: 10-Jun-2020 16:55) Posted:

|

The whole idea of this complex deal is really for temasek to take over sembmarine and subsequently merge with keppel . National interest at play as OG remains a key business interest In Singapore blue print

Rem we are coming up w a Tuas mega port in the near future - 2021

We need a strong consolidated keppel / sembmarine for us to remain relevant

So to me , survival is guaranteed . It?s all about how good is the deal when the merger comes in oct / nov etc

Rem we are coming up w a Tuas mega port in the near future - 2021

We need a strong consolidated keppel / sembmarine for us to remain relevant

So to me , survival is guaranteed . It?s all about how good is the deal when the merger comes in oct / nov etc

So anybody shorted this counters since so say the deal is unfair mm would like to hear some opinion..

Not completely true

Usually the rights itself has a trading value as well

So as a shareholder u can sell the rights too

Conversely you have to buy the rights itself to subscribe for 20 cent shares ... ie higher than absolute 20 cents

Usually the rights itself has a trading value as well

So as a shareholder u can sell the rights too

Conversely you have to buy the rights itself to subscribe for 20 cent shares ... ie higher than absolute 20 cents

Elf2000 ( Date: 10-Jun-2020 18:42) Posted:

|

Assume that if I buy 1 lot at the current closing price at $0.61 so I have to fork out 5 lots of rights share x $0.20 is $1000 and total share I have own now after the ex-rights are 1 lot($610.00) + 5 lots($1000.00) the total cost will be $1610.00 ÷ 6 lots = $0.27!🧐 so end up I paying more for the rights issue price🤔 ...correct me if I am wrong.

Adjusted for the additional rights shares, the price is 29c. Still pricey any price above 40c. Moreover 5X more shares will flood the market. Even if the merger with Keppel materialise, do you think Keppel shareholders will agree at 61c.

Precisely. Be it a shareholder of SCI or SMM, it's both very beneficial. For this, I thank Temasek holdings for the first time. I'm a shareholder of SCI.. I bought it at $1.41. I'll let it rollover the corporate action. As for SMM, I'm already loading and be accumulating more. I'm seeing that the Keppel O&M be a good deal as by then we will see better oil and gas pricing with the easing of the lockdown in few months time.

weekaykee ( Date: 10-Jun-2020 16:59) Posted:

|

Long and Short squeeze narrower

The main attraction for people buying into SMM from now onwards would be the upside from a very likely merger with Kepple O& M. I myself seriously considering doing a short term (6-12 mths) punt on SMM but when it goes ex-rights.

alfredx ( Date: 10-Jun-2020 15:42) Posted:

|