Great Eastern reports 21% higher Q3 profit at S$180.2 million

GREAT Eastern : G07 0% reported a 21 per cent increase in net profit to S$180.2 million for the third quarter ended September, compared to S$149.3 million in the same period last year.

This came on the back of a 5 per cent increase in total weighted new sales to S$419.4 million, driven by Singapore sales due to new product launches, said the insurance arm of OCBC on Wednesday (Nov 1).

The group&rsquo s new business embedded value stood at S$183.7 million, 8 per cent lower than the S$198.7 million in the corresponding quarter last year.

It noted that the lower new business embedded value for Q3 despite higher total weighted new sales was largely driven by lower margins in Singapore.

For the three quarters, net profit increased 65 per cent to S$617.4 million. This was led by higher profit in the Singapore Life business and favourable investment performance in the shareholders&rsquo fund.

&ldquo Our underlying insurance business is healthy, though dampened by higher-than-expected medical claims in Singapore and Malaysia,&rdquo said the group.

Profit from insurance business of the nine months registered a 14 per cent increase at S$543.5 million, while profit from shareholders&rsquo fund reversed from a loss of S$103.9 million to an S$84.8 million gain.

The investment increase was attributable to &ldquo mark-to-market&rdquo gain in equities and collective investment schemes in the nine months, compared to a loss a year earlier.

Total weighted new sales for the first three quarters decreased 21 per cent to S$1.1 billion, because of lower single premium sales from the Singapore market during the first three quarters.

Correspondingly, the lower sales volume led its new business embedded value to fall 9 per cent to S$534.9 million.

However, the group noted that margins improved across core markets compared to 2022. Its new business embedded value margin recorded a 6.1 percentage point increase to 46.7 per cent in the nine months.

Great Eastern&rsquo s chief executive Khor Hock Seng highlighted some key initiatives across the Singapore and Malaysia markets to deliver sustainable value to shareholders.

&ldquo We remain positive on the long-term outlook of our business, even as we navigate the present inflationary and interest rate challenges.&rdquo

https://www.smallcapasia.com/5-singapore-stocks-that-can-benefit-from-higher-interest-rates/

5 Singapore Stocks that can Benefit from Higher Interest Rates

5. Great Eastern (SGX: G07)

GE Holdings is a prominent insurance company with roots in Singapore. Operating under the umbrella of the OCBC Group, Great Eastern has been a reliable financial institution providing a wide range of insurance and financial solutions to its customers.

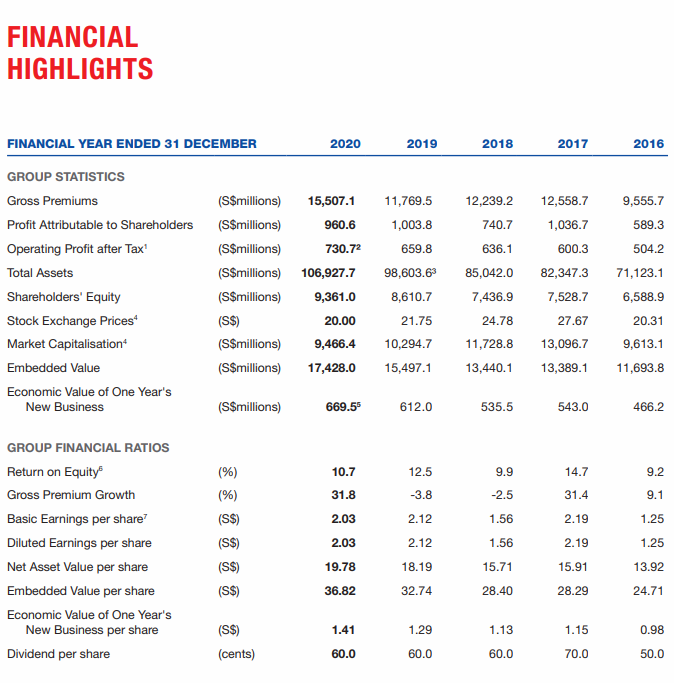

The Group observed an encouraging growth of 23%, bringing the Total Weighted New Sales to S$1,543.7 million compared to the same period of the prior year.

Serving as an indicator of the company&rsquo s long-term economic profitability, the NBEV (New Business Embedded Value) witnessed a 9% surge to reach S$669.5 million.

This upswing can be ascribed to Great Eastern&rsquo s compelling product range coupled with its widespread distribution network.

Additionally, the company has experienced consistent premium growth over the last two years, with rates reaching double digits.

Factors like product diversity, market strategy, and distribution efficiency have played a pivotal role in this growth.

Great Eastern Q2 profit up 251% to S$193.2 million after change in accounting standards

GREAT Eastern, : G07 +1.78%the insurance arm of OCBC, on Thursday (Aug 3) posted a 251 per cent rise in net profit for the second quarter ended June, to S$193.2 million from S$55 million in the same period the year before.

The jump in profit came after the group adopted a change in accounting standards on Jan 1, which led to the comparative numbers for FY2022 being restated. Before the numbers were restated, net profit for Q2 2022 was S$282.9 million.

The replacement of Singapore Financial Reporting Standard (SFRS) 4 Insurance Contracts into SFRS 17 impacted the timing of profit recognition and initial shareholders&rsquo equity.

It will not significantly affect the group&rsquo s business operations, earning prospects and ability to pay dividends, Great Eastern said.

The group will pay an interim dividend of S$0.35 per share on Aug 31. The interim dividend was S$0.1 for the previous financial year.

Great Eastern said it will aim to pay a more steady dividend payment twice a year, targeting a full-year payout that is based on sustainable profits. The company also aims to maintain each dividend amount at a level no lower than the preceding one

The latest results bring net profit for the first half of 2023 to S$437.2 million, 95 per cent higher than the S$224.1 million recorded in the same period last year.

Before restatement due to a change in accounting standards, net profit for H1 2022 stood at S$502.9 million.

The group also attributed the rise in H1 net profit to favourable investment performance for its Singapore Life business and shareholders&rsquo fund. It noted that its underlying insurance business &ldquo remained healthy&rdquo , despite higher-than-expected claims in Singapore and Malaysia.

&ldquo Our general insurance business experienced good growth from our retail business, supported by our well-received product proposition,&rdquo said Khor Hock Seng, chief executive of the group.

For the second quarter ended June, total weighted new sales (TWNS) lost 39 per cent to S$335 million from S$548.2 million, which reflected lower single-premium sales from the Singapore market.

Similarly, the new business embedded value (NBEV) registered a 9 per cent decline to S$181.5 million from S$200.1 million. However, a more favourable product mix towards protection plans in Singapore and Malaysia allowed NBEV margins to improve, the group said.

Its new customer base grew by over 150,000 in H1 across the group, it added.

For the six months ended Jun 30, TWNS was S$725.9 million, 31 per cent down from S$1,051.8 million. NBEV stood at S$351.2 million,10 per cent down from S$390.6 million in the same period a year ago.

Insurance service result in the half-year period dropped 41 per cent to S$371.2 million, led by higher insurance service expenses and net expenses from reinsurance contracts held.

This was mainly due to worsening claims experience, said the group.

More could be on the plan . Recent increased in GE shareholdings by OCBC , and now this buy over.

Certainly no surprise if GE is taken private.

Also expecting more aggressive moves from CEO HELEN esp in the greatern bay area.

DYODD

Happy investing.

Certainly no surprise if GE is taken private.

Also expecting more aggressive moves from CEO HELEN esp in the greatern bay area.

DYODD

Happy investing.

Joelton ( Date: 01-Aug-2023 10:48) Posted:

|

OCBC&rsquo s Great Eastern in talks to buy MetLife Malaysian arm, sources say

Singapore insurer Great Eastern Holdings Ltd. G07 0.05% is in talks to buy MetLife Inc.&rsquo s Malaysian venture, according to people familiar with the matter.

The subsidiary of Oversea-Chinese Banking Corp. (OCBC) O39 -0.08% is conducting due diligence on AmMetLife Insurance Bhd. and seeking regulatory approval to clinch the deal, the people said. A transaction could value AmMetLife, which the US company jointly owns with Kuala Lumpur-listed AMMB Holdings Bhd., at US$250 million ($332.4 million) to US$300 million, the people said.

An agreement could be reached within the next few months, the people said, asking not to be identified because the matter is private. Talks are ongoing and could still fall apart or face delays, they said.

A spokesperson for MetLife declined to comment, while a representative for Great Eastern didn&rsquo t immediately respond to requests for comment. A representative for AMMB said any announcements will be made in accordance with listing requirements.

A deal would see Great Eastern prevail in its pursuit of AmMetLife Insurance. The Singaporean firm was interested in acquiring the unit last year, even as Zurich Insurance Group AG had emerged as the frontrunner to buy a majority stake, Bloomberg News reported at the time.

MetLife and AMMB teamed up to form their Malaysian insurance partnership AmMetLife in 2014, its website shows. The parties started exploring a potential divestment of the business in 2020, people familiar with the matter said at the time.

AmMetLife offers life insurance and wealth protection services through nearly 200 AmBank and AmMetLife branches in the country, according to its website. It reported about 307 million ringgit ($90.5 million) of gross earned premiums for the six months ended Sept. 30, a 16.7% increase from a year earlier, according to its latest financial report.

Founded in 1908, Great Eastern has more than $100 billion in assets and over 14.5 million policyholders, its website shows. It has life, general and group insurance operations as well as an asset management arm called Lion Global Investors Ltd. Great Eastern operates in Singapore, Malaysia, Brunei and Indonesia and has a presence in China as well as an office in Myanmar, according to the website.

I think all waiting for any good development! It may or may not happen! But chart wise, seem turning upwards! https://www.spore-share.com/2023/06/great-eastern_22.html

Great Eastern Holdings

On Jun 19, OCBC acquired 2,345,800 shares of Great Eastern Holdings at S$16.99 per share. With a consideration of S$ 39,855,142, the married deal increased OCBC&rsquo s total interest in Great Eastern from 87.91 per cent to 88.40 per cent.

As a subsidiary of OCBC Bank, Great Eastern maintains an S$8 billion market capitalisation, however its monthly median of daily trading volume does not qualify for inclusion in the STI. Nonetheless, the stock has averaged more than S$670,000 a day in average trading turnover this year, more than doubling its 2022 average turnover level.

With over S$100 billion in assets and more than 14.5 million policyholders, including 12 million from government schemes, Great Eastern provides insurance solutions to customers through three distribution channels. These include a tied agency force, bancassurance, and financial advisory firm, Great Eastern Financial Advisers.

Great Eastern has set out a three-pronged strategic focus to bolster its product propositions to address customers&rsquo needs across all life stages and segments.

This involves enhancing its digital tools to offer a more seamless and intuitive experience, the strengthening of operational services to bring greater value to customers, in addition to living up to its refreshed brand identity and promise.

OCBC privatisation of Great Eastern unlikely but plausible: analysts

OCBC is unlikely to take its listed insurance arm Great Eastern private, although the bank might have bigger plans for the insurer, noted analysts.

On Monday (Jun 19), the lender said it bought 2.3 million Great Eastern shares at S$16.99 each in cash or S$39.9 million in total, bringing its stake in the insurer to 88.4 per cent from 87.9 per cent.

The purchase was on &ldquo a willing buyer willing seller basis&rdquo , OCBC said in a bourse filing.

Glenn Thum, research analyst at Phillip Securities Research, noted that the move was &ldquo interesting&rdquo given that OCBC previously said it would not actively trade Great Eastern.

During the bank&rsquo s annual general meeting (AGM) in April, OCBC said Great Eastern is seen as a capability, and that it was not something that it trades, but rather something that it builds on.

Thum said: &ldquo There might be bigger plans in play by OCBC, and (this move) might just be on a &lsquo willing buyer, willing seller&rsquo basis&rsquo .&rdquo

CGS-CIMB analyst Andrea Choong said OCBC&rsquo s move to increase its stake reaffirms its commitment towards building the insurance franchise.

&ldquo OCBC has often emphasised the value of the Great Eastern franchise to OCBC,&rdquo Choong noted.

But the analyst noted that the possibility of taking Great Eastern private has not been explicitly ruled out by the management, and thus remains on the table.

When answering a shareholders&rsquo question during the April AGM on whether the bank will consider taking GE private, OCBC said it was always open to possibilities for acquisitions, but that it would leave its stance &ldquo ambiguous&rdquo .

DBS Group Research analyst Lim Rui Wen also noted that there have been previous attempts by OCBC to take Great Eastern private, through a share swap and cash offer, though the bids have failed. OCBC last tried to take Great Eastern private in 2006 through a voluntary unconditional cash offer.

With Great Eastern trading at a discount to its embedded value per share, she expects that OCBC may continue acquiring Great Eastern shares as it had done in the latest transaction.

Given that OCBC already owns 88.4 per cent of Great Eastern shares, the bank would need to purchase just another 1.6 per cent &ndash or 7.6 million shares &ndash to trigger a compulsory delisting of the latter.

Based on Great Eastern&rsquo s closing price of S$17.55 per share on Wednesday, it would cost OCBC around S$963.3 million, before fees, to purchase all 54.9 million of the insurer&rsquo s shares it does not own at that price.

Analysts weighed the pros and cons of taking the insurer private. Phillip&rsquo s Thum noted that keeping Great Eastern listed would provide the company with access to additional capital and liquidity, as well as more brand visibility and a possibility to increase valuation.

Meanwhile, a privatisation would allow it to have more control over its operations, he said.

But having Great Eastern&rsquo s financials consolidated into OCBC&rsquo s results introduces heightened volatility and uncertainty to OCBC&rsquo s earnings, noted Maybank Securities head of research Thilan Wickramasinghe.

In a research note in March, Wickramasinghe noted that Great Eastern has high earnings volatility given multiple market shocks in the past five years.

The insurer had also been a drag on the bank&rsquo s performance in recent quarters &ndash Great Eastern posted a 22 per cent fall in total weighted new sales to S$390.9 million for its fiscal first quarter ended Mar 31. For its second half of the year ended Dec 31, 2022, the insurer&rsquo s profit also declined 37 per cent amid the negative impact of financial market movements.

OCBC&rsquo s peers have mitigated this volatility through their bancassurance partnerships, which drive fee certainty without the downside of mark-to-market gyrations of insurance portfolios, Wickramasinghe said.

DBS&rsquo Lim noted that each strategy has their own benefits &ndash having a bancassurance deal is more asset-light, but owning an insurer provides organic synergies.

For Phillip&rsquo s Thum, he expects that keeping Great Eastern is a strategic option for OCBC, as this differentiates them from their local bank peers.

Even though the earnings may be more volatile, the bank will have a wider range of products and be able to provide more options to their customers, Thum said.

He added: &ldquo It may be beneficial short term and will directly impact earnings, but in the long term I would think holding on to Great Eastern would be the better option.&rdquo

In response to queries on the deal, OCBC group chief financial officer Goh Chin Yee said that increasing OCBC&rsquo s stake in Great Eastern is in line with its group&rsquo s strategy to be a leading financial services partner in Asia, with a broad geographical footprint in North and South-east Asia and a diversified business.

The bank will constantly evaluate ways to enhance its group&rsquo s franchise, and will take appropriate actions to create value for the group and its shareholders, she added.

OCBC shows it&rsquo s still a buyer of Great Eastern

A RARE fillip of excitement earlier this week involving shares of Great Eastern could refocus investor attention on OCBC&rsquo s strategic plans for its tightly-owned insurance group and the exceedingly low valuations the latter&rsquo s shares currently garner in the market.

It seems unlikely to be a catalyst for a re-rating of the stock, though.

Nearly 2.37 million Great Eastern shares changed hands on Monday (Jun 19), most of them at just under S$17 each.

The stock ended the day at S$17.20, up nearly 0.9 per cent versus its previous close.

The bank said after the market closed that it had bought, on a &ldquo willing buyer, willing seller basis&rdquo , nearly 2.35 million Great Eastern shares at S$16.99 per share, or for a total of S$39.9 million.

A filing by Great Eastern showed OCBC&rsquo s direct and deemed interest in the insurer increased on Jun 19 to more than 418.4 million shares, from nearly 416.1 million shares previously. This raised OCBC&rsquo s stake in Great Eastern from 87.9 per cent to 88.4 per cent.

The transaction is a reminder that OCBC remains a buyer of Great Eastern shares nearly two decades after its attempts to take the insurer private were rebuffed by minority investors.

It is also, perhaps, an indication that some minority shareholders of Great Eastern are now less resistant to privatisation.

While trading in Great Eastern may be suspended if fewer than 10 per cent of its shares are held by the public, the Singapore Exchange requires delisting offers to be both fair and reasonable.

On Tuesday, Great Eastern&rsquo s share price surged as much as 4.7 per cent with 128,100 shares changing hands. The stock ended the day at S$17.70, up 2.9 per cent versus the previous day&rsquo s close.

Great Eastern closed on Wednesday at S$17.55, on a much lower trading volume of 47,200 shares.

Past privatisation attempts

As OCBC was offloading non-core assets and reorganising its balance sheet in the early 2000s, a strategic decision was made to subsume Great Eastern in order to increase the group&rsquo s heft and diversify its sources of income.

In 2004, OCBC unveiled a proposal to acquire all the shares in Great Eastern it did not already own. It offered 976 new OCBC shares for every 1,000 Great Eastern shares. OCBC also proposed a &ldquo selective capital reduction&rdquo in order to cancel a block of OCBC shares held by Great Eastern at the time.

When the offer closed, however, OCBC&rsquo s stake in Great Eastern had increased from 48.8 per cent to only 81.1 per cent.

OCBC continued trying to tighten its grip on Great Eastern. In 2006, OCBC made a voluntary cash offer for all the Great Eastern shares it did not already own at S$16 per share.

The offer price was more than 14 per cent above Great Eastern&rsquo s market price at the time. More importantly, it was 1.51 times Great Eastern&rsquo s embedded value at end-2005 of S$10.598 per share.

Embedded value refers to the present value of future profits an insurer is expected to generate from its in-force business plus its adjusted net asset value. Conceptually, it is the value of an insurer assuming it does not write any further policies.

Yet, there was enough minority shareholder resistance to the offer to prevent Great Eastern from being taken private. When the offer closed, OCBC and its concert parties held 87.1 per cent of Great Eastern&rsquo s shares.

Were Great Eastern&rsquo s minority shareholders right to reject OCBC&rsquo s overtures? Would they have been better off accepting OCBC&rsquo s offers?

Great Eastern has quietly grown from strength to strength over the years. At the end of 2022, its embedded value stood at S$37.81 per share. This was more than three times its embedded value at end-2006 of S$11.885 per share.

Weak market valuation

Yet, even after the uptick earlier this week, Great Eastern currently trades at a 54 per cent discount to its embedded value &ndash a far cry from the 51 per cent premium OCBC offered to pay in 2006.

This pathetic market valuation could be due to Great Eastern&rsquo s shares being tightly held by OCBC and minority investors alike. Since the end of 2006, Great Eastern&rsquo s shares have delivered a total return of only 70.5 per cent &ndash almost all of it from dividend payouts.

By contrast, OCBC&rsquo s shares have returned 211.7 per cent during the same period.

While it could make sense for OCBC to eventually make another attempt at taking Great Eastern private &ndash either through a cash offer or the issue of new OCBC shares &ndash it isn&rsquo t in OCBC&rsquo s interest to be too generous with minority shareholders of Great Eastern.

In the meantime, it seems unlikely that Great Eastern&rsquo s board will take any steps to boost the market valuation of its shares &ndash for instance, by promoting wider ownership and greater trading liquidity of the stock. After all, Great Eastern&rsquo s controlling shareholder has no apparent interest in seeing this happen.

Where does that leave Great Eastern&rsquo s minority shareholders? At current levels, the stock seems too undervalued to sell unless one is in a pinch. But a deal that fully unlocks Great Eastern&rsquo s immense value seems unlikely to materialise any time soon.

Great Eastern Holdings free float falls further with OCBC acquiring 2.3 million shares

Oversea-Chinese Banking Corp announced that it bought 2.3 million shares of Great Eastern Holdings G07 0.94% for $16.99 apiece. The tranche cost $39.9 million. The purchase in the market takes OCBC O39 -0.47% &rsquo s stake in GEH from 87.9% to 88.4%. Market observers have indicated that the sellers are likely to be offspring of old-time shareholders, or as one investor put it &ldquo inherited old monies&rdquo .

After Citibank and HSBC nominees, the largest shareholders of GEH are the grandchildren of S.Q. Wong, the legendary former chairman of Overseas Assurance Company. Wong&rsquo s business interests were wide and varied. According to ISEAS Library, Wong' s first investments were in mining and real estate, but soon expanded to include rubber, banking and insurance. Of course, Wong&rsquo s name was most closely associated with the Great Eastern life Assurance Company, the Overseas Assurance Company and OCBC. He sat on the boards of these companies, as well as the Kempas Rubber Company and Kuchai Tin Berhad until his 80s.

Presently, and mindful of the 10% free-float rule, investors in GEH are concerned that the purchase price on June 19 is at a significant discount to GEH&rsquo s embedded value of $37.81 per share in FY2022. This, in turn is 2% lower than FY2021&rsquo s $38.57.

Embedded value is the sum of the value of In-Force Business and the value of the adjusted Shareholders&rsquo Funds. The value of the In-Force Business is calculated using cash flow assumptions for future operating experience and are discounted at a risk-adjusted discount rate. The value of the In-Force Business varies from traditional DCF methods to arrive at an NPV because the risk-adjusted discount rate and allowance for the cost of holding statutory reserves for risk are approximates.

The economic value of one year&rsquo s new business rose by 7.1% y-o-y in FY2022 to $860.4 million. However, shareholders&rsquo equity fell by 6% to $9,431.4 million.

The closer OCBC&rsquo s stake gets to 90%, the stronger the likelihood of compulsory acquisition by OCBC. Interestingly, this comes at a time when life insurers elsewhere, such as FWD have expressed an interest in an IPO. In November last year, Bloomberg reported that SingLife with Aviva is eyeing an IPO.

See also: Liquidity risks low for Singapore banks though funding costs will rise in 2H2023: Bloomberg Intelligence

NTUC Income corporatised to become Income Insurance Ltd. In May, Income announced The Proposed Capital Reduction which aims to return $43 million to shareholders. This translates into a one-off distribution of around $0.40 cash per share to all Income Insurance shareholders. The capital reduction is intended to help shareholders with Income Insurance&rsquo s transition from a co-operative to a company, Income Insurance said.

Market watchers are keenly watching Income Insurance and some have suggested the corporatisation and capital return could be part of the path towards an IPO.

what' s ailing g.e. .....?

Great Eastern H2 profit falls 37% to S$281.3 million

INSURANCE provider Great Eastern : G07 -1.81%&rsquo s profit for the second half of the year ended Dec 31, 2022 declined 37 per cent to S$281.3 million, from S$443.1 million for H2 2021.

In a bourse filing on Wednesday (Feb 22), the group attributed this to the &ldquo negative impact of financial market movements&rdquo which adversely impacted the valuation of insurance contract liabilities.

The group&rsquo s earnings per share for the second half of the year stood at S$0.60, down from S$0.93 in the year ago period.

After the announcement, shares of Great Eastern fell as much as 1.8 per cent and closed at S$18.45. Shares of OCBC &ndash which holds an 87 per cent stake in Great Eastern &ndash also fell as much as 1.8 per cent on Wednesday, before ending 1.1 per cent lower at S$12.90. The bank is due to report its fourth-quarter and full-year results for FY2022 on Friday.

In a results briefing on Wednesday, Great Eastern chief executive Khor Hock Seng noted that Singapore experienced an inverted yield curve towards the end of the year, resulting in the insurer&rsquo s liabilities &ndash which are valued on a longer term &ndash incurring higher mark-to-market losses.

This resulted in a non-operating loss of S$249.7 million in Q4, from the non-operating profit of S$46.1 million in the same period in 2021.

Rising interest rates had also hit the sales of savings products in Singapore, given that consumers could turn to other options such as fixed deposits and Singapore Treasury bills that were offering better returns with higher yields, Khor noted.

Gross premiums for H2 fell 21 per cent to S$7.7 billion from S$9.8 billion, due to lower sales in single premium products.

Meanwhile, total weighted new sales (TWNS) for the group fell 9 per cent to S$449.1 million in Q4. TWNS dropped 18 per cent in Singapore, although it rose 3 per cent in Malaysia.

Great Eastern chief financial officer Ronnie Tan noted that the insurance industry typically sells more savings products in Singapore, as compared to Malaysia with more protection products, resulting in such interest rate movements having a higher impact on operations in Singapore than in Malaysia.

For the full year, profit for the insurer was down 30 per cent to S$784.2 million, from S$1.1 billion for FY2021. Gross premiums fell just 2 per cent to S$18.6 billion, from nearly S$19 billion in FY2021.

Meanwhile, the insurer&rsquo s embedded value fell 2 per cent on year in FY2022, due to a decline in its adjusted shareholders&rsquo fund.

Tan noted that the adjusted shareholders&rsquo fund was dragged by investment losses recorded for both equities and fixed income products in 2022. He added, however, that this was a trend seen across the industry, and that this was mitigated by a 5.9 per cent rise in the value of Great Eastern&rsquo s in-force business over FY2021.

Looking ahead, Khor expects a growing emphasis on the protection market will likely continue to boost sales in 2023. Meanwhile, new structures in savings products should also provide some recovery, given that savings products still have a high demand among customers.

&ldquo But we may have to introduce more protection on such products, to differentiate them from other instruments that do not offer such protection,&rdquo he said.

Khor also expects the insurer&rsquo s Indonesia business to post solid growth, while its Takaful business in Malaysia continues to be a bright spot.

Great Eastern proposed a dividend of S$0.55 per share for the second half of the year, payable on May 8 after books closure on Apr 28.

Great Eastern Holdings reports 4QFY2022 earnings of $3.3 million, down 99%

Great Eastern Holdings G07 0.00% has reported earnings of $3.3 million for 4QFY2022, down 99% y-o-y, as the valuation of its insurance contract liabilities in the Singapore non-participating business got " adversely" impacted by market movements.

For the whole of FY2022, earnings dropped by 30% to $784.2 million, largely reflecting the lower valuation of investments given the challenging global investment climate.

Operating Profit from its insurance business, meanwhile, managed to grow at a " healthy" pace of 7% over FY2021.

For 4QFY2022, Great Eastern' s TWNS, or total weighted new sales, was down by 9% y-o-y. For the whole of FY2022, the drop was 3%.

The company explains that while regular premium sales improved, it suffered from lower sales from the single premium plans.

Great Eastern plans to pay a final dividend of 55 cents, bringing the payout for FY2022 to 65 cents.

" While the Group&rsquo s profit was impacted by the volatility in the global financial markets during the year, our investment portfolio remains sound and our capital position also remains strong," says group CEO Khor Hock Seng.

He notes that the company' s NBEV, or new business embedded value increased by 9%, while the operating profit from insurance was up by 7%, as " good growth momentum" continued.

" Looking ahead, the business climate remains challenging, reflecting geopolitical uncertainty, a difficult investment climate and inflationary pressures," says Khor.

See also: Dyna-Mac reports earnings of $10.1 mil for the 2HFY2022, up four times y-o-y

" We remain positive on the long-term growth potential of the markets we operate in and will continue to strengthen our business model and build a resilient and sustainable business for the long term," he adds.

Great Eastern&rsquo s Q3 profit up 30% on insurance business says climate remains challenging

Great Eastern' s total weighted new sales sank 27 per cent in the third quarter to $403.4 million.

SINGAPORE - Great Eastern on Wednesday posted a 30 per cent increase in net profit to $278 million for the third quarter ended Sept 30, from $213.3 million a year ago.

The insurance arm of OCBC Bank said the increase was mainly driven by higher profit from its insurance business, which reflects the net mark-to-market gain on asset liability from increasing interest rates.

Non-operating profit for the segment swung to $83.9 million in the third quarter, from a loss of $3.5 million in the previous year. Year to date, non-operating profit rose 25 per cent to $311.2 million, from $248.2 million previously.

Meanwhile, operating profit for the segment declined 38 per cent year on year to $208.1 million. On a year-to-date basis, operational profit slipped marginally to $573.6 million, from $575.8 million last year.

The insurer swung to a loss from its shareholders&rsquo fund at $103.9 million year to date &ndash a $14.1 million loss in the third quarter &ndash from a profit of $73.8 million previously.

This was due to lower mark-to-market losses in equities and bonds, compared with a relatively flatter performance in 2021, said Great Eastern.

Total weighted new sales sank 27 per cent in the third quarter to $403.4 million, from $554.3 million in 2021, mainly due to lower single premium sales from the Singapore market, which was offset by stronger sales momentum from the Malaysia and Indonesia markets, noted Great Eastern.

Great Eastern chief executive Khor Hock Seng expects the business climate to remain challenging in the near to medium term, &ldquo reflecting geopolitical uncertainty, a difficult investment climate and inflationary pressures&rdquo .

&ldquo Our focus remains on strengthening our business and distribution model, supported by data-driven targeted propositions to meet the needs of our customers,&rdquo he said.

MEDIA RELEASE

Great Eastern 9M-22 Financial Results

Q3-22 Profit Attributable to Shareholders up 30% to S$278.0 million 9M-22

down 12% to S$780.9 million

Q3-22 Total Weighted New Sales down 27% to S$403.4 million 9M-22 down

1% to S$1,459.3 million

Q3-22 New Business Embedded Value up 10% to S$202.1 million 9M-22 up

4% to S$595.3 million......

https://links.sgx.com/1.0.0/corporate-announcements/S130NV07YF90EQOU/737300_2022%20Q3%20Media%20Release.pdf

Great Eastern 9M-22 Financial Results

Q3-22 Profit Attributable to Shareholders up 30% to S$278.0 million 9M-22

down 12% to S$780.9 million

Q3-22 Total Weighted New Sales down 27% to S$403.4 million 9M-22 down

1% to S$1,459.3 million

Q3-22 New Business Embedded Value up 10% to S$202.1 million 9M-22 up

4% to S$595.3 million......

https://links.sgx.com/1.0.0/corporate-announcements/S130NV07YF90EQOU/737300_2022%20Q3%20Media%20Release.pdf

MEDIA RELEASE

(For Immediate Release)

Great Eastern Reports Q1-22 Financial Results

Operating Profit from Insurance Business up 6% to S$191.4 million

Profit Attributable to Shareholders down 50% to S$220.0 million

Total Weighted New Sales up 32% to S$505.3 million

New Business Embedded Value down 3% to S$191.3 million....

https://links.sgx.com/1.0.0/corporate-announcements/GY1434EPZBTBIPH6/714468_2022%20Q1%20Media%20Release.pdf

(For Immediate Release)

Great Eastern Reports Q1-22 Financial Results

Operating Profit from Insurance Business up 6% to S$191.4 million

Profit Attributable to Shareholders down 50% to S$220.0 million

Total Weighted New Sales up 32% to S$505.3 million

New Business Embedded Value down 3% to S$191.3 million....

https://links.sgx.com/1.0.0/corporate-announcements/GY1434EPZBTBIPH6/714468_2022%20Q1%20Media%20Release.pdf

Train moving up north... Who taking the ride 🚉 🚂 🚂 👍 👍 👍

I think on big picture insurance shares should do well (for rate hike environment) , this fall might be good opportunity to accumulate some 😉 👍

https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/life-insurance-shares-rally-as-prospect-of-faster-interest-rate-hikes-rises-68423092

https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/life-insurance-shares-rally-as-prospect-of-faster-interest-rate-hikes-rises-68423092

Yes that was 2-weeks (Feb-22) old news. Reaction is slow??

Great Eastern Q4 profit falls 33% but posts full-year increase

MEGAN CHEAHTAN NAI LUN

FEB 22, 2022 08:09 AM

Great Eastern Q4 profit falls 33% but posts full-year increase

MEGAN CHEAHTAN NAI LUN

FEB 22, 2022 08:09 AM

john_ric ( Date: 07-Mar-2022 18:11) Posted:

|

Q4 profit down 33% that is a lot.