Keppel

Last:10.59

-0.07

-0.07

Keppel Corp

Post Reply

401-420 of 7137

Post Reply

401-420 of 7137

Short-term setback for Keppel. When the sale of M1 is eventually approved, it will rebound very fast as well.

Joelton ( Date: 28-Mar-2026 10:59) Posted:

Keppel shares fall as much as 4.6% on M1-Simba deal delay

The counter drops as low as S$11.70 in early trading

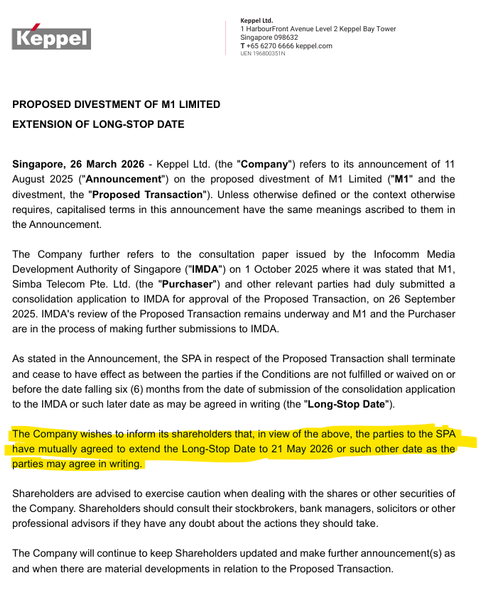

[SINGAPORE] Shares of Keppel : BN4 -3.02% fell on Friday (Mar 27) after overnight news of a mutually agreed extension of the long-stop date for the proposed M1 deal.

The counter fell as much as 4.6 per cent to S$11.70 in early trading, erasing S$0.57 a share, as investors reacted negatively to the deal&rsquo s delay. The counter later pared some of the losses to be 3.3 per cent lower at 9.30 am.

Keppel in August last year announced plans to sell M1&rsquo s telco business to mobile network operator Simba for S$1.4 billion in an all-cash deal.

M1, Simba and other relevant parties then submitted a consolidation application to the Infocomm Media Development Authority of Singapore on Sep 26, said Keppel.

Without the Thursday extension to May 21, the sale and purchase agreement would have been terminated and ceased to have effect if certain conditions were not fulfilled and waived before the long-stop date of Mar 26.

|

|

Keppel shares fall as much as 4.6% on M1-Simba deal delay

The counter drops as low as S$11.70 in early trading

[SINGAPORE] Shares of Keppel : BN4 -3.02% fell on Friday (Mar 27) after overnight news of a mutually agreed extension of the long-stop date for the proposed M1 deal.

The counter fell as much as 4.6 per cent to S$11.70 in early trading, erasing S$0.57 a share, as investors reacted negatively to the deal&rsquo s delay. The counter later pared some of the losses to be 3.3 per cent lower at 9.30 am.

Keppel in August last year announced plans to sell M1&rsquo s telco business to mobile network operator Simba for S$1.4 billion in an all-cash deal.

M1, Simba and other relevant parties then submitted a consolidation application to the Infocomm Media Development Authority of Singapore on Sep 26, said Keppel.

Without the Thursday extension to May 21, the sale and purchase agreement would have been terminated and ceased to have effect if certain conditions were not fulfilled and waived before the long-stop date of Mar 26.

SBB today - 400,000 shares bought at $11.91 to $12.00 ($4,786,535)

Today' low price : $11.70, High Price: $12.11, Mid point : $11.91. So it bought at the higher end of mid point.

I prepare the chart and MSCP helps with the explanation:

1. Current Trend

- The stock is still in a downtrend &mdash prices have been sliding lower overall.

- Today&rsquo s move was down about 2.8%, which reinforces that weakness.

2. Key Moving Averages

- 50‑ day EMA (around 11.92): The price is sitting right around this level. It&rsquo s acting like a balance point &mdash if the stock holds above it, that&rsquo s supportive if it breaks below, it could signal more downside.

- 5‑ day EMA (around 12.20): The short‑ term average is above the current price, showing near‑ term momentum is negative.

3. Chart Pattern

- The lines drawn form a symmetrical triangle: one sloping down (resistance) and one sloping up (support).

- This pattern usually means the stock is coiling &mdash building up energy before a bigger move.

- A breakout above the descending line could mean recovery a breakdown below the ascending line could mean further weakness.

4. Volume

- Trading volume today was 9 million shares, which is fairly active.

- Rising volume on a down day suggests sellers are still in control.

Layman&rsquo s Takeaway

Think of it like this:

- The stock is stuck in a tug of war between buyers (support line) and sellers (resistance line).

- Right now, sellers have the upper hand, but the triangle pattern means a decisive move is coming soon.

- If it breaks upwards, it could signal a rebound. If it breaks downwards, expect more weakness.

Newbie2025 ( Date: 27-Mar-2026 17:13) Posted:

| Sir, what does it mean in layman terms

Thanks |

|

Sir, what does it mean in layman terms

Thanks

No worries lar...

Steady pom pi pi

https://rfs.cgsi.com/api/download?file=f20c78bb-a93e-40cb-a046-bc684c3fde7f

Reiterate Add

● During its FY25 results briefing, KEP guided that it would be disbursing 10-15% of the

gross value of its asset monetisation completed over 2025-2030. This could translate

into a special DPS of c.S$0.05-0.11/share for the M1 deal upon completion.

● We reiterate our Add call for KEP&rsquo s recurring income stream and dividend upside. Our

SOP-based TP of S$13.52 values New Keppel at 18x FY27F earnings and non-core

assets at book value. Re-rating catalysts: completion of M1 divestment and further asset

monetisation. Downside risks: delays or unfavourable adjustments to deal terms to

accommodate concerns raised by IMDA and slower pace of monetisation.

In addition

Keppel commit higher Payout ratio when recurring is higher in future. Currnet dividends is 56% payout ratio., it can go even higher to 70%(minimum ) or higher. However, as interim they have special dividends from monetarization. There is no real urgent for them to increase their core payout to 70% but from this forecast, is possible that their 2030 core might even be higher than their current core+ special dividends)

Take for example. now their core is 0.19 + 0.15 = 0.34 SGD/share at 2025. That only their 2025 56% payout. Mean Techincally they are able to pay 0.45 SGD for 75% payout if they want too at 2030.

However, kindly take note, AUM at 2030 is 200 BIllion Target Versus AUM at 2026 100Billion . So the profit they have in 2030 will definitely be higher than now ( ideally). So if assume a 50% net profit higher by 2030. The payout for dividends is at least 0.7 SGD/share by then.

2025

Now is 0.34 SGD/share(56% payout bass) + 0.13 SGD/share special dividends = 0.47 SGD/share

2030

75% Payout basis with 50% higher profit then now. Even without monetized asset. It will be 0.7 SGD/share. This 0.7SGD/share is limited by my assumption of MAXIMUM 50% net profit and MINIMUM 75% payout. If the netprofit is higher or payout ratio is higher, it will be higher.

YuanLong94 ( Date: 27-Mar-2026 13:00) Posted:

I agreed with you .

Maybe just to add on.

Keppel has a clear framework for rewarding shareholders from proceeds of asset monetisation (selling non-core assets):

- They aim to pay out 10&ndash 15% of the gross value of asset monetisation transactions completed in the financial year as special dividends.

- In FY2025, they used the upper end (15%) for the completed monetisation of S$1.6 billion in gross value.

- This resulted in a proposed special dividend of ~13 cents per share:

- 2 cents per share in cash.

- The rest (~11 cents equivalent) as dividend in-specie (1 Keppel REIT unit for every 9 Keppel shares held).

This special dividend is in addition to their ordinary dividends. The M1 sale (which would generate nearly S$1 billion in cash) was not yet completed in FY2025, so it was excluded &mdash meaning more special dividends could come in future years once it close

Andrewtan18 ( Date: 27-Mar-2026 11:47) Posted:

| What $1b gain. When you sell an asset, the proceeds is not called a gain. In your balance sheet you deduct the amount from the asset (M1) and add to another asset (cash). There is a gain only if the M1 asset is carried in the books at lower than the priceeds from the sale. Since Keppel has stated there is a 220m accounting impact from this sale it means M1 is carried in its books at 220m more than the sales price. Therefore the sale does not create a gain, it only turn an asset into a cash component. |

|

|

|

JP Morgan downgraded Keppel to " Neutral" with TP of $12.

if it didnt go through, it will slowdown it re-rating of AUM ( it used to be eps x

15 (example 0.4 x

15 = 6 dollar, now maybe around eps x

21/22(0.6 x 21.5 = 12.9 dollar , maximum can go up to

x27 if benchmark to blackrock or

x70 brookfield(trillion versus Keppel 200B 2030 target)

Keppel do give better dividends then Blackrock. so the rating for Keppel maybe till 2028 then we will know with aermont to add in another 25Billion to 30Billion AUM to new Keppel( Their Target is 2028 150 Billion, 2030 200 Billion) . They are hitting their 2026 target of 100 Billion

Once EPS up, the stock price up. Once re-rating up, the stock price will up too. So is more on how people envisioned Keppel as a AUM company. If you believe in New Keppel, it will worth higher when future EPS & Re-rating up.

M1 is not a bad company, it generated around 50 million Profit per year but due to upcoming competition ,it does not align with New Keppel strategy. Bifrost will take over to contribute the missing M1 revenue while Keppel can immediate monetized on the 1Billion. As " M1 is locked for sale" The 25million profit for 2H 2025 (July 2025 to Dec 2025) is not under Keppel to the best of my understanding from their report.

LoneRanger1420 ( Date: 27-Mar-2026 10:43) Posted:

If didn't go through , will share price drop ? Likewise if go through price goes up ?

Louistan ( Date: 27-Mar-2026 09:42) Posted:

| M1 sale may not go throug |

|

|

|

I agreed with you .

Maybe just to add on.

Keppel has a clear framework for rewarding shareholders from proceeds of

asset monetisation (selling non-core assets):

- They aim to pay out 10&ndash 15% of the gross value of asset monetisation transactions completed in the financial year as special dividends.

- In FY2025, they used the upper end (15%) for the completed monetisation of S$1.6 billion in gross value.

- This resulted in a proposed special dividend of ~13 cents per share:

- 2 cents per share in cash.

- The rest (~11 cents equivalent) as dividend in-specie (1 Keppel REIT unit for every 9 Keppel shares held).

This special dividend is

in addition to their ordinary dividends. The M1 sale (which would generate nearly S$1 billion in cash) was

not yet completed in FY2025, so it was excluded &mdash meaning more special dividends could come in future years once it close

Andrewtan18 ( Date: 27-Mar-2026 11:47) Posted:

What $1b gain. When you sell an asset, the proceeds is not called a gain. In your balance sheet you deduct the amount from the asset (M1) and add to another asset (cash). There is a gain only if the M1 asset is carried in the books at lower than the priceeds from the sale. Since Keppel has stated there is a 220m accounting impact from this sale it means M1 is carried in its books at 220m more than the sales price. Therefore the sale does not create a gain, it only turn an asset into a cash component.

YuanLong94 ( Date: 27-Mar-2026 09:13) Posted:

- The Long-Stop Date is the final deadline by which all conditions (mainly regulatory approval from IMDA) must be fulfilled, or the deal can be terminated.

- They are simply giving themselves more time (about 2 extra months) for the IMDA review process, which is still underway.

Firstly, the recognized the lost of 222m for M1 (asset price drop).(2025)

Secondly , they have not factor the gain from the transaction , 1 Billion Cash ( 2H 2026?)

Thirdly, the profit of M1 has been locked under the entity since July 2025 till now. So M1 profit 2H did not go to Keppel for Year 2026

Lastly, if M1 go through there will be special dividends, if M1 did not go through(unlikely), it does not affected the 0.47 cent that is announce for FY 2025 ( August and April). There is still other monetarize for the balance of the 13.5B monetarized plan.

For past few days there is no sharebuyback due to all this sensitive announcement. I think Keppel is up for grab next week with the sharebuyback |

|

|

|

What $1b gain. When you sell an asset, the proceeds is not called a gain. In your balance sheet you deduct the amount from the asset (M1) and add to another asset (cash). There is a gain only if the M1 asset is carried in the books at lower than the priceeds from the sale. Since Keppel has stated there is a 220m accounting impact from this sale it means M1 is carried in its books at 220m more than the sales price. Therefore the sale does not create a gain, it only turn an asset into a cash component.

YuanLong94 ( Date: 27-Mar-2026 09:13) Posted:

- The Long-Stop Date is the final deadline by which all conditions (mainly regulatory approval from IMDA) must be fulfilled, or the deal can be terminated.

- They are simply giving themselves more time (about 2 extra months) for the IMDA review process, which is still underway.

Firstly, the recognized the lost of 222m for M1 (asset price drop).(2025)

Secondly , they have not factor the gain from the transaction , 1 Billion Cash ( 2H 2026?)

Thirdly, the profit of M1 has been locked under the entity since July 2025 till now. So M1 profit 2H did not go to Keppel for Year 2026

Lastly, if M1 go through there will be special dividends, if M1 did not go through(unlikely), it does not affected the 0.47 cent that is announce for FY 2025 ( August and April). There is still other monetarize for the balance of the 13.5B monetarized plan.

For past few days there is no sharebuyback due to all this sensitive announcement. I think Keppel is up for grab next week with the sharebuyback.

JurongW ( Date: 26-Mar-2026 19:59) Posted:

|

|

|

as reiterated. it's Telco business is gonna have minimal ok impact on Keppel simply because the key drivers of the business are Property and infrastructure along with wealth management. Focus on these businesses as they will impact Keppel more than M1.

Keppel's long term value depends very little on M1. Don't buy it just because we want a special dividend next year. Buy it for it's recurring dividend streams for the next ten years

LoneRanger1420 ( Date: 27-Mar-2026 10:43) Posted:

If didn't go through , will share price drop ? Likewise if go through price goes up ?

Louistan ( Date: 27-Mar-2026 09:42) Posted:

| M1 sale may not go throug |

|

|

|

If didn't go through , will share price drop ? Likewise if go through price goes up ?

Louistan ( Date: 27-Mar-2026 09:42) Posted:

M1 sale may not go through

hubertwee ( Date: 27-Mar-2026 09:09) Posted:

| What' s up with Keppel today ? |

|

|

|

it will.

Keppel is determined to get rid of non core assets.

Telecommunications is not gonna be it's core business.

Therefore it must go, even if given away.

Keppel must focus on its new mission. The new Keppel must emerge from the shadows of rig building and a whole host of other industries ...

Keppel towards 2030

Louistan ( Date: 27-Mar-2026 09:42) Posted:

M1 sale may not go through

hubertwee ( Date: 27-Mar-2026 09:09) Posted:

| What' s up with Keppel today ? |

|

|

|

Keppel' s close of planned sale of M1 to Simba extended

The closing of Keppel' s sale of mobile operator subsidiary M1 to Australia-listed Tuas, the owner of local telco Simba Telecom, has been extended.

The deal is subject to the approval of local industry regulator the Infocomm Media Development Authority of Singapore.

As part of its review, IMDA has put out a consultation paper on Oct 1 and feedback invited.

Last August, Tuas announced it will buy M1 from Keppel for an enterprise value of $1.43 billion.

While consolidation of the local mobile industry has long been flagged, StarHub, which operates a mobile network jointly with M1, has long been said to be the acquirer instead.

According to Keppel on March 26, IMDA' s review of the deal " remains underway" and M1 and the Tuas are addressing additional queries from the regulator.

The deal, which was aimed to be closed within six months after the sale and purchase agreement, has been extended to May 21, or another mutually-agreeable date.

M1 sale may not go through

hubertwee ( Date: 27-Mar-2026 09:09) Posted:

| What' s up with Keppel today ? |

|

- The Long-Stop Date is the final deadline by which all conditions (mainly regulatory approval from IMDA) must be fulfilled, or the deal can be terminated.

- They are simply giving themselves more time (about 2 extra months) for the IMDA review process, which is still underway.

Firstly, the recognized the lost of 222m for M1 (asset price drop).(2025)

Secondly , they have not factor the gain from the transaction , 1 Billion Cash ( 2H 2026?)

Thirdly, the profit of M1 has been locked under the entity since July 2025 till now. So M1 profit 2H did not go to Keppel for Year 2026

Lastly, if M1 go through there will be special dividends, if M1 did not go through(unlikely), it does not affected the 0.47 cent that is announce for FY 2025 ( August and April). There is still other monetarize for the balance of the 13.5B monetarized plan.

For past few days there is no sharebuyback due to all this sensitive announcement. I think Keppel is up for grab next week with the sharebuyback.

JurongW ( Date: 26-Mar-2026 19:59) Posted:

|

What' s up with Keppel today ?