Venture

Last:18.26

-

2022 Venture Corporation - A Year Of Recovery

Post Reply

41-60 of 888

Post Reply

41-60 of 888

Venture Corporation: Operating Model and Capital Position

Venture Corporation, the largest Singapore‑ listed technology stock by market capitalisation, reflects this through a design‑ led manufacturing model that integrates design and engineering with manufacturing, supported by a net‑ cash position and selective, customer‑ driven capital deployment.

Venture&rsquo s outlook continues to focus on disciplined operating performance and selective investment across its diversified customer programmes. DBS also highlights Venture&rsquo s resilient profitability despite softer volumes, supported by its focus on high value‑ add programmes. DBS noted that this operating model has translated into strong net cash, underpinning balanced capital allocation including dividends and share buybacks. This aligns with a broader shift among key supply‑ chain‑ oriented companies towards prioritising delivery capability and financial resilience, consistent with World Economic Forum research showing that operational reliability and balance‑ sheet strength are central to corporate performance through volatile cycles.

While Venture ranks as Singapore&rsquo s largest technology stock by market capitalisation, it has ranked as the fifth most traded stock of the sector this year after AEM Holdings, UMS Holdings, iFAST Corporation, and Frencken Group. Rightstock ( Date: 10-May-2026 14:29) Posted:

In my opinion $20 by the end of this week.

kye_lin ( Date: 10-May-2026 08:35) Posted:

| Probably can hit above 20. After that hard to say. |

|

|

|

In my opinion $20 by the end of this week.

kye_lin ( Date: 10-May-2026 08:35) Posted:

| Probably can hit above 20. After that hard to say. |

|

Probably can hit above 20. After that hard to say.

Key Analyst Target Price (May 2026):

With both Venture' s customers - Philip Morris and Illumina sales soaring, it should be positive for Venture moving forward

Philip Morris International (PM) shares have shown strong performance, recently trading around \(\$171\) per share, driven by a solid Q1 2026 earnings beat ($1.96 EPS vs. $1.83 expected) and growing smoke-free portfolio revenue. While the stock recently pulled back nearly 2% from post-earnings highs, it has still outperformed the broader tobacco industry, benefiting from robust ZYN pouch sales and IQOS, which retained its FDA modified-risk authorization.

As of May 2026, Illumina (ILMN) shares are experiencing a strong rally, up over 5% following a Q1 2026 earnings beat, with revenue growth driven by NovaSeq demand, trading around $139&ndash $142. The company raised its 2026 guidance, and investors are responding positively to the continued divestiture of Grail.

DYODD

tongphlp ( Date: 08-May-2026 09:35) Posted:

Philip Morris' IQOS Retains FDA Modified-Risk Authorization

Zacks Equity Research

April 20, 2026 3 min read

Philip Morris International Inc. PMI has received renewed regulatory backing in the United States, as the Food and Drug Administration (&ldquo FDA&rdquo ) reauthorized its IQOS heated tobacco system as a modified risk tobacco product. The decision allows the company to continue communicating that switching completely from cigarettes to IQOS can reduce exposure to harmful chemicals, based on the agency&rsquo s scientific assessment.

The renewal covers multiple versions of the IQOS device along with associated tobacco sticks sold under the HEETS brand. The FDA concluded that extending this authorization is appropriate for public health, taking into account both current tobacco users and non-users.

This regulatory decision reinforces PM&rsquo s broader strategy to transition away from traditional cigarettes toward smoke-free alternatives. The company has been investing heavily in this shift for more than a decade, committing billions of dollars to research, product development and commercialization. The effort is increasingly reflected in its business mix, with smoke-free products contributing a substantial and growing share of overall revenues and profits.

Zacks Investment Research

Image Source: Zacks Investment Research

IQOS remains central to this transformation. The product is already available in dozens of markets worldwide and has shown strong adoption in countries such as Japan, where heated tobacco products have significantly reduced cigarette consumption. Philip Morris continues to position IQOS as a key tool for adult smokers seeking alternatives, alongside other smoke-free offerings like nicotine pouches and e-vapor products.

The FDA&rsquo s renewed authorization provides both validation and continuity for PM&rsquo s reduced-risk portfolio. As regulatory frameworks evolve and consumer preferences shift, the decision strengthens the Zacks Rank #3 (Hold) company&rsquo s ability to advance its long-term goal of replacing cigarettes with scientifically substantiated alternatives for adult smokers.

Shares of PM have risen 3.8% over the past six months, outperforming the industry&rsquo s growth of 1.5%.

- One of Venture' s customers is PMI

|

|

Venture Corporation Ltd &ndash Here comes the AI bump - Phillips Securities

May 8, 2026

PSR Recommendation: BUYStatus: Upgraded

Last Close Price: 18.65Target Price: 22.10

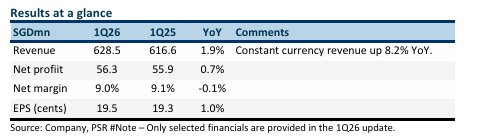

- 1Q26 revenue/net profit were within expectations at 24%/22% of our FY26e forecast. 1Q is seasonally weaker. Revenue faced a 6.3 percentage-point drag from the weaker US dollar. AI-related infrastructure products drove 11% YoY revenue growth. However, consumer lifestyle and related categories declined by 12% YoY .

- Venture&rsquo s guidance emphasised new shoots appearing in 2026. We believe it is benefiting from the massive global build-out of data centres. Key products include network interface cards in servers and semiconductor equipment components. Revenue returned to growth after 12 consecutive quarters of decline.

- We upgrade our recommendation to BUY from ACCUMULATE. Our FY26e PATMI is unchanged. We raised our target price to S$22.10 (prev. S$16.80), or 25x FY26e PE, as we move away from historical valuations toward US-listed peers trading at 33x forward PE. Earnings growth for FY26e/FY27e will be led by AI products to support the massive deployment of data centres globally. 4Q26e will be driven by the launch of new consumer lifestyle products. Net cash on the balance as at 1Q26 was disclosed as in excess of S$1bn.

The Positive

The Positive

+ Revenue returns to growth. 1Q26 revenue rebounded with a 1.9% YoY growth (or 8.2% constant

currency). It is a turnaround from 12 consecutive quarters of YoY decline. Driving growth was the

11.2% improvement in AI-related infrastructure products. It included products in test and

measurement, networking cards, sensors, controllers and semiconductor equipment.

The Negative

&ndash Weak consumer lifestyle. The portfolio of products that include consumer lifestyle declined

12.4% YoY to S$212mn. Improvements to the product increased its lifespan and lengthened its

lifecycle.

Massive short squeeze in the works. Many shorted this morning and now scrambling to cover. Will venture close green today?

I should have clarified it does not look like a move based on the fundamentals of Venture specifically. Obviously a situation like this can affect the broader economic environment and hence the fundamentals of individual stocks either for good or bad.

tongphlp ( Date: 08-May-2026 11:17) Posted:

the writing has always been on the wall...think many are tired of this nonsense of POTUS

Alignment ( Date: 08-May-2026 10:56) Posted:

Almost everything is dropping as the US/Iran ceasefire deal is appearing to collapse. Those that rose fastest in the lull are now dropping the most, generally speaking. Does not look like a move based on fundamentals, more about market volatility.

|

|

|

|

the writing has always been on the wall...think many are tired of this nonsense of POTUS

Alignment ( Date: 08-May-2026 10:56) Posted:

Almost everything is dropping as the US/Iran ceasefire deal is appearing to collapse. Those that rose fastest in the lull are now dropping the most, generally speaking. Does not look like a move based on fundamentals, more about market volatility.

|

|

Almost everything is dropping as the US/Iran ceasefire deal is appearing to collapse. Those that rose fastest in the lull are now dropping the most, generally speaking. Does not look like a move based on fundamentals, more about market volatility.

Any idea why the drop in share price?

Philip Morris' IQOS Retains FDA Modified-Risk Authorization

Zacks Equity Research

April 20, 2026 3 min read

Philip Morris International Inc. PMI has received renewed regulatory backing in the United States, as the Food and Drug Administration (&ldquo FDA&rdquo ) reauthorized its IQOS heated tobacco system as a modified risk tobacco product. The decision allows the company to continue communicating that switching completely from cigarettes to IQOS can reduce exposure to harmful chemicals, based on the agency&rsquo s scientific assessment.

The renewal covers multiple versions of the IQOS device along with associated tobacco sticks sold under the HEETS brand. The FDA concluded that extending this authorization is appropriate for public health, taking into account both current tobacco users and non-users.

This regulatory decision reinforces PM&rsquo s broader strategy to transition away from traditional cigarettes toward smoke-free alternatives. The company has been investing heavily in this shift for more than a decade, committing billions of dollars to research, product development and commercialization. The effort is increasingly reflected in its business mix, with smoke-free products contributing a substantial and growing share of overall revenues and profits.

Zacks Investment Research

Image Source: Zacks Investment Research

IQOS remains central to this transformation. The product is already available in dozens of markets worldwide and has shown strong adoption in countries such as Japan, where heated tobacco products have significantly reduced cigarette consumption. Philip Morris continues to position IQOS as a key tool for adult smokers seeking alternatives, alongside other smoke-free offerings like nicotine pouches and e-vapor products.

The FDA&rsquo s renewed authorization provides both validation and continuity for PM&rsquo s reduced-risk portfolio. As regulatory frameworks evolve and consumer preferences shift, the decision strengthens the Zacks Rank #3 (Hold) company&rsquo s ability to advance its long-term goal of replacing cigarettes with scientifically substantiated alternatives for adult smokers.

Shares of PM have risen 3.8% over the past six months, outperforming the industry&rsquo s growth of 1.5%.

- One of Venture' s customers is PMI

Who' s this DBS analyst??

Venture (VEMLF)

Venture received a Buy rating and a S$21.80 price target from DBS analyst Ling Lee Keng

Keng is a 4-star analyst with an average return of 15.6% and a 56.5% success rate. Keng covers the Technology sector, focusing on stocks such as Renesas Electronics, Applied Materials, and UMS Integration.

Joelton ( Date: 07-May-2026 12:14) Posted:

Analysts upbeat on Venture Corporation after 1QFY2026 results, shares surge more than 11%

After reporting a stronger set of results on a y-o-y basis for the 1QFY2026 ended March 31, analysts have strengthened their outlook on Mainboard-listed Venture Corporation.

In a bourse filing after trading hours on May 5, the advanced technology solutions provider reported y-o-y growth in earnings of 0.7% to $56.3 million on the back of a 1.9% y-o-y rise in revenue to $628.5 million. Earnings per share was 19.5 cents with net margin at 9%.

Venture Corp shares, following the news, surged by as much as 11.17% to $18.32 ahead of the lunch break on May 6.

Before the result announcement, William Tng of CGS International had raised his target price for the company to $21.78 from $17.04 while maintaining a &ldquo buy&rdquo call in his report dated April 30. Forecasting earnings per share to grow by an average of 8% from FY2026 to FY2028, his target price values Venture at 23 times of FY2027 forecasted P/E.

The results beat his expectations slightly and he reinforced his call at an unchanged target price with a follow-up report on May 5.

Meanwhile, DBS analyst Lee Keng Ling has upgraded Venture Corporate to a &ldquo buy&rdquo at a higher target price of $21.80 from the previous $17.90. This valuation is based on an higher forecasted 2027 P/E of 24 times, up from the previous 21 times

To her, the result was &ldquo broadly&rdquo in line with expectations and signals early signs of recovery, with momentum expected to pick up through the year.

She notes that Portfolio B, which include the test and measurement, semiconductor and data centre domains, grew revenue by 11.2% y-o-y to $417 million and remain the company&rsquo s principal expansion pillars.

For Portfolio A &mdash comprising life science, medtech and lifestyle consumer &mdash which declined in revenue 12.4% to $212 million, she suggests that a recovery in the consumer lifestyle segment could emerge in 2HFY2026, supported by new product introductions aimed at improving user experience and rebuilding volume momentum.

She believes the quarter marks an &ldquo important turnaround&rdquo as it delivered the company&rsquo s first y-o-y quarterly earnings and revenue growth after three years of decline. &ldquo Venture remains an attractive value play, underpinned by a strong balance sheet with over $1 billion in net cash and zero debt,&rdquo she states, adding that this cash holding and dividend yield of 4.9% makes the counter &ldquo compelling&rdquo .

UOB Kay Hian&rsquo s John Cheong and Heidi Mo have similarly raised their target price to $20.65 from $18.64, with their &ldquo buy&rdquo rating maintained. This valuation is pegged to 23.7 times forward FY2027 P/E or 2.5 standard deviations above the long-term historical mean.

In their May 6 report, Cheong and Mo note that results were in line, with revenue growing by 8% on a constant currency basis suggesting strong momentum. Both seemed satisfied with the net margin of 9% which indicated focus on high value-add solutions and cost discipline. Venture&rsquo s cash holding of more than $1 billion provides downside protection and capacity for strategic investments, they point out.

On the operational front, they see upcoming growth in Venture&rsquo s various business segments including data centre and life science. They believe Venture&rsquo s R& D programme positions the business to seize opportunities beyond product/system design and development.

Cheong and Mo raise their target price to reflect &ldquo stronger conviction&rdquo in the firm&rsquo s earnings visibility, balance sheet and upcoming growth drivers.

|

|

Analysts upbeat on Venture Corporation after 1QFY2026 results, shares surge more than 11%

After reporting a stronger set of results on a y-o-y basis for the 1QFY2026 ended March 31, analysts have strengthened their outlook on Mainboard-listed Venture Corporation.

In a bourse filing after trading hours on May 5, the advanced technology solutions provider reported y-o-y growth in earnings of 0.7% to $56.3 million on the back of a 1.9% y-o-y rise in revenue to $628.5 million. Earnings per share was 19.5 cents with net margin at 9%.

Venture Corp shares, following the news, surged by as much as 11.17% to $18.32 ahead of the lunch break on May 6.

Before the result announcement, William Tng of CGS International had raised his target price for the company to $21.78 from $17.04 while maintaining a &ldquo buy&rdquo call in his report dated April 30. Forecasting earnings per share to grow by an average of 8% from FY2026 to FY2028, his target price values Venture at 23 times of FY2027 forecasted P/E.

The results beat his expectations slightly and he reinforced his call at an unchanged target price with a follow-up report on May 5.

Meanwhile, DBS analyst Lee Keng Ling has upgraded Venture Corporate to a &ldquo buy&rdquo at a higher target price of $21.80 from the previous $17.90. This valuation is based on an higher forecasted 2027 P/E of 24 times, up from the previous 21 times

To her, the result was &ldquo broadly&rdquo in line with expectations and signals early signs of recovery, with momentum expected to pick up through the year.

She notes that Portfolio B, which include the test and measurement, semiconductor and data centre domains, grew revenue by 11.2% y-o-y to $417 million and remain the company&rsquo s principal expansion pillars.

For Portfolio A &mdash comprising life science, medtech and lifestyle consumer &mdash which declined in revenue 12.4% to $212 million, she suggests that a recovery in the consumer lifestyle segment could emerge in 2HFY2026, supported by new product introductions aimed at improving user experience and rebuilding volume momentum.

She believes the quarter marks an &ldquo important turnaround&rdquo as it delivered the company&rsquo s first y-o-y quarterly earnings and revenue growth after three years of decline. &ldquo Venture remains an attractive value play, underpinned by a strong balance sheet with over $1 billion in net cash and zero debt,&rdquo she states, adding that this cash holding and dividend yield of 4.9% makes the counter &ldquo compelling&rdquo .

UOB Kay Hian&rsquo s John Cheong and Heidi Mo have similarly raised their target price to $20.65 from $18.64, with their &ldquo buy&rdquo rating maintained. This valuation is pegged to 23.7 times forward FY2027 P/E or 2.5 standard deviations above the long-term historical mean.

In their May 6 report, Cheong and Mo note that results were in line, with revenue growing by 8% on a constant currency basis suggesting strong momentum. Both seemed satisfied with the net margin of 9% which indicated focus on high value-add solutions and cost discipline. Venture&rsquo s cash holding of more than $1 billion provides downside protection and capacity for strategic investments, they point out.

On the operational front, they see upcoming growth in Venture&rsquo s various business segments including data centre and life science. They believe Venture&rsquo s R& D programme positions the business to seize opportunities beyond product/system design and development.

Cheong and Mo raise their target price to reflect &ldquo stronger conviction&rdquo in the firm&rsquo s earnings visibility, balance sheet and upcoming growth drivers.

Forgot the link

DBS :

Venture Corp: AI Momentum Offsets Consumer Drag Upgrade To BUY

tongphlp ( Date: 07-May-2026 10:23) Posted:

After CGS upgraded Venture, price rocketed $1.9.

DBS too upgraded Venture, will it do the same?

See whose words are stronger...

Alignment ( Date: 06-May-2026 12:36) Posted:

You cannot look at the financials in isolation. What matters is the numbers relative to expectations as reflected in the share price. Expectations were very low, so even a stablisation/slight increase would have prompted a positive reaction.

But on top of this the strength of the reaction relates to the guidance rather than the latest financials |

|

|

|

After CGS upgraded Venture, price rocketed $1.9.

DBS too upgraded Venture, will it do the same?

See whose words are stronger...

Alignment ( Date: 06-May-2026 12:36) Posted:

You cannot look at the financials in isolation. What matters is the numbers relative to expectations as reflected in the share price. Expectations were very low, so even a stablisation/slight increase would have prompted a positive reaction.

But on top of this the strength of the reaction relates to the guidance rather than the latest financials.

spore1 ( Date: 06-May-2026 12:26) Posted:

| I am surprised the mkt seem to like the latest financial numbers. Only up a bit but price spike up |

|

|

|

Tng has made successful calls on AEM, ISDN and Venture

DYODD

Alignment ( Date: 06-May-2026 12:20) Posted:

There are similarities between what was said in this update and the AEM FY results announcement on 25 Feb when the AEM share price was still at S$2. Fast forward two months and the share price went above S$8.

Not saying that Venture' s share price will quadruple in the same way in the next two months, but the markets can clearly see parallels.

MambaFinancial89 ( Date: 06-May-2026 10:37) Posted:

| " This is like new shoots sprouting in early spring... We expect these new shoots to grow in 2026." Excerpt from their Outlook in the 1Q26 update. Don' t think I have ever seen such a statement from a Venture announcement. |

|

|

|

may want to note the below are the shareholders in VC currently

Top Institutional Holders

- Silchester International Investors LLP: ~7.9% &ndash 9.0%

- Columbia Management Investment Advisers, LLC: ~5.98%

- The Vanguard Group, Inc.: ~4.05%

- BlackRock, Inc.: ~2.28%

- Seafarer Capital Partners, LLC: ~2.09%

- Massachusetts Financial Services Company (MFS): ~1.90%

- Norges Bank Investment Management: ~1.61%

- Dimensional Fund Advisors LP: ~1.42%

Alignment ( Date: 06-May-2026 12:20) Posted:

There are similarities between what was said in this update and the AEM FY results announcement on 25 Feb when the AEM share price was still at S$2. Fast forward two months and the share price went above S$8.

Not saying that Venture' s share price will quadruple in the same way in the next two months, but the markets can clearly see parallels.

MambaFinancial89 ( Date: 06-May-2026 10:37) Posted:

| " This is like new shoots sprouting in early spring... We expect these new shoots to grow in 2026." Excerpt from their Outlook in the 1Q26 update. Don' t think I have ever seen such a statement from a Venture announcement. |

|

|

|

Financial matters really. But it depends on what the BBs and institutions want the price to be...

Alignment ( Date: 06-May-2026 12:36) Posted:

You cannot look at the financials in isolation. What matters is the numbers relative to expectations as reflected in the share price. Expectations were very low, so even a stablisation/slight increase would have prompted a positive reaction.

But on top of this the strength of the reaction relates to the guidance rather than the latest financials.

spore1 ( Date: 06-May-2026 12:26) Posted:

| I am surprised the mkt seem to like the latest financial numbers. Only up a bit but price spike up |

|

|

|

You cannot look at the financials in isolation. What matters is the numbers relative to expectations as reflected in the share price. Expectations were very low, so even a stablisation/slight increase would have prompted a positive reaction.

But on top of this the strength of the reaction relates to the guidance rather than the latest financials.

spore1 ( Date: 06-May-2026 12:26) Posted:

I am surprised the mkt seem to like the latest financial numbers. Only up a bit but price spike up

Alignment ( Date: 06-May-2026 12:20) Posted:

There are similarities between what was said in this update and the AEM FY results announcement on 25 Feb when the AEM share price was still at S$2. Fast forward two months and the share price went above S$8.

Not saying that Venture' s share price will quadruple in the same way in the next two months, but the markets can clearly see parallels |

|

|

|