Keppel

Last:10.59

-0.07

-0.07

Keppel Corp

Post Reply

361-380 of 7137

Post Reply

361-380 of 7137

Keppel share Lao Hong!

Keppel warns of &lsquo second-order&rsquo shocks from prolonged Middle East conflict

Its direct exposure remains limited, but broader macroeconomic impacts would affect the global asset manager

[SINGAPORE] Keppel : BN4 -0.58% has warned that while its direct exposure to the Middle East remains limited, an escalation in regional conflict could trigger significant &ldquo second-order&rdquo effects on global energy prices and the international economy.

In a series of responses to shareholders&rsquo questions ahead of its 58th annual general meeting on Friday (Apr 17), the global asset manager noted on Apr 11 that its operations in Qatar and Saudi Arabia have not been directly affected by ongoing hostilities.

&ldquo So far, our operations and maintenance of the Domestic Solid Waste Management Centre in Qatar, the investment by Keppel Infrastructure Trust (managed by Keppel) in a Saudi Arabia gas pipeline and our rig charters in Saudi Arabia have not been directly impacted,&rdquo said the company in a bourse filing.

However, the mainboard-listed company cautioned that &ldquo the second-order effects in terms of the impact on gas supply, energy prices and the international economy bear close watching&rdquo .

&ldquo If there is prolonged disruption to gas supply and an energy crunch, this could have significant impacts on Singapore and the region. Keppel would also be affected,&rdquo the global asset manager said.

&ldquo There could also be broader macroeconomic effects, including cost inflation, higher interest rates, among others,&rdquo it added.

Energy hedging and pass-throughs

To mitigate these risks, Keppel highlighted that its gas supply is diversified via piped natural gas from Malaysia and international liquefied natural gas cargoes.

As at end-2025, about two-thirds of its electricity contracts are long term and hedged, providing what the company describes as &ldquo some cushioning against spark spread volatility&rdquo .

Keppel also stated that the impact from higher energy prices is &ldquo not expected to be significant, as more than 95 per cent of data centre leases are on power pass-through contracts, covering customer electricity bills&rdquo .

Additionally, it noted that &ldquo the US tariffs and changes in the global economic order are contributing to a more fragmented and uncertain operating environment&rdquo .

&ldquo So far, the direct impact of the tariffs on Keppel has been relatively limited, as Keppel is not engaged in the manufacturing or export sectors,&rdquo the company said.

It added that there may even be opportunities for the company, as investors&rsquo preference for defensive, cash-flow generative assets would drive demand for alternative real assets in infrastructure and private credit.

China property market, private credit concerns

Separately addressing concerns regarding the Chinese property market, Keppel noted it has reduced its residential landbank exposure from S$3.1 billion at the end of 2017 to about S$900 million as at end-2025.

Looking ahead, the group is pursuing a &ldquo China-for-China&rdquo strategy, partnering domestic capital to &ldquo selectively invest in opportunities with a focus on achieving quality risk-adjusted returns&rdquo .

Management also sought to distance itself from recent challenges in the private credit market. Unlike open-ended funds with exposure to sections facing disruptions, Keppel noted that it runs a &ldquo close-ended private credit fund series where investors are locked-in for eight to 10 years&rdquo , and that the series is &ldquo doing well&rdquo .

The company also confirmed it has sold its entire 5 per cent stake in Seatrium as at Apr 1, realising a total value of S$429 million.

Meanwhile, the divestment of its M1 telco business remains pending regulatory approval, with the parties agreeing to extend the long-stop date to May 21.

Keppel noted that it reached S$95 billion in funds under management (FUM) as at end-2025 and is on track to achieve its FUM target of S$100 billion by the end of 2026, if not earlier.

The counter was trading at S$12.06 at 2.37 pm on Monday, S$0.07 or 0.6 per cent lower.

FY 2025 0.15 + 0.19 Core + 0.13 Special dividends)

FY 2026 with Seatrium 492million sale @1st April , and upcoming M1 1B , minimum 0.13 SGD special dividends is almost guaranteed @15% for FY2026 (FY2025 is 15% of 1.6B) , hopefully more sale within 9 more months

and 56% payout now ( can be up to 70% in future )

Let assume net profit increase by 15% . Core payout 0.34 SGD will increase by 15% too if payout ratio maintain at 56%

YuanLong94 ( Date: 27-Mar-2026 13:00) Posted:

I agreed with you .

Maybe just to add on.

Keppel has a clear framework for rewarding shareholders from proceeds of asset monetisation (selling non-core assets):

- They aim to pay out 10&ndash 15% of the gross value of asset monetisation transactions completed in the financial year as special dividends.

- In FY2025, they used the upper end (15%) for the completed monetisation of S$1.6 billion in gross value.

- This resulted in a proposed special dividend of ~13 cents per share:

- 2 cents per share in cash.

- The rest (~11 cents equivalent) as dividend in-specie (1 Keppel REIT unit for every 9 Keppel shares held).

This special dividend is in addition to their ordinary dividends. The M1 sale (which would generate nearly S$1 billion in cash) was not yet completed in FY2025, so it was excluded &mdash meaning more special dividends could come in future years once it close

Andrewtan18 ( Date: 27-Mar-2026 11:47) Posted:

| What $1b gain. When you sell an asset, the proceeds is not called a gain. In your balance sheet you deduct the amount from the asset (M1) and add to another asset (cash). There is a gain only if the M1 asset is carried in the books at lower than the priceeds from the sale. Since Keppel has stated there is a 220m accounting impact from this sale it means M1 is carried in its books at 220m more than the sales price. Therefore the sale does not create a gain, it only turn an asset into a cash component. |

|

|

|

Looks good, Sir

No annoncement of SBB since yesterday.

Presume it has suspend buyback activities in compliance with the blackout period due to the quarterly business update on 23 Apr.

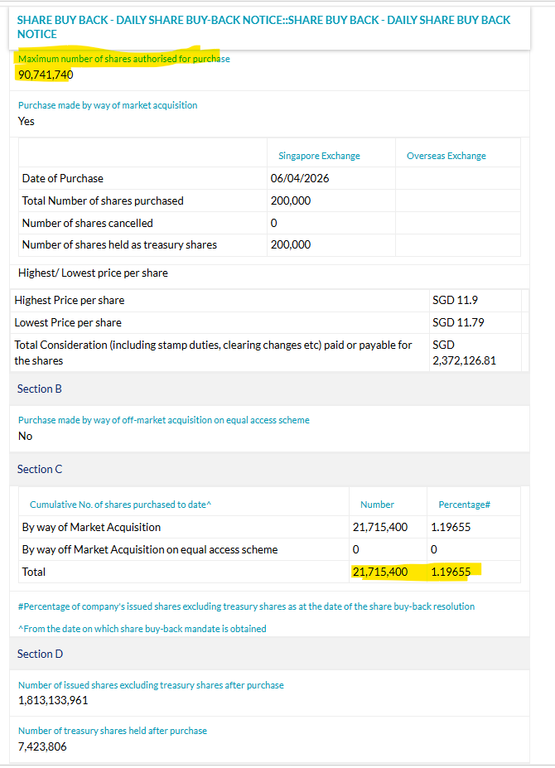

SBB today - 200,000 shares bought at 11.81 to 11.95 ($2,375,136)

The buyback program still has a long runway, with 90,741,740 shares authorized.

As of today, ~ 24% of the max allocation has been executed.

PiRPiR ( Date: 06-Apr-2026 20:51) Posted:

06:23 AM EDT, 04/06/2026 (MT Newswires) -- Keppel (SGX:BN4) bought back 200,000 shares in the open market on Monday for about SG$2.4 million, according to a same-day filing with the Singapore Exchange.

The infrastructure and real estate company has so far repurchased nearly 21.7 million shares under its existing buyback mandate. |

|

06:23 AM EDT, 04/06/2026 (MT Newswires) -- Keppel (SGX:BN4) bought back 200,000 shares in the open market on Monday for about SG$2.4 million, according to a same-day filing with the Singapore Exchange.

The infrastructure and real estate company has so far repurchased nearly 21.7 million shares under its existing buyback mandate.

SBB today - 200,000 shares bought at 11.79 to 11.90 ($2,372,126)

Doesn' t make sense. 17 April report - will reveal good or bad results, depends on it will be below or above " support" /" resistance" .

War in Iran ends earlier - sky rocket to 13.

Interest raise - ... you got it.

If price breaks down below the triangle formation, the next support lies at 11.59, followed by the lower bound of the blue channel.

Yes, OCBC&rsquo s cut in savings account interest rates from 5.45% to 4.45% (effective 1 May 2026) could encourage more funds to flow into the market, especially equities and higher‑ yield instruments, since deposit returns are less attractive. However, the actual impact depends on investor sentiment, global rate trends, and risk appetite.

🔎 Details of OCBC&rsquo s Move

- Effective Date: 1 May 2026

- Product: OCBC 360 Account (flagship savings account)

- Change: Interest on the first S$100,000 cut from 5.45% &rarr 4.45% per annum

- Reason: &ldquo In line with broader market conditions&rdquo and expectations of lower global interest rates.

- History: This is the first cut in 2026, after two reductions in 2025.

📊 Implications for Fund Flows

-

Retail Investors

- Lower deposit returns reduce the incentive to keep large sums in savings accounts.

- Some funds may shift into Singapore equities, REITs, or bonds offering higher yields.

-

Institutional & Wealth Clients

- Wealth managers may reallocate toward fixed income, structured products, or dividend stocks.

- The cut signals a broader easing environment, aligning with expectations of a U.S. Fed rate cut in 2026.

-

Market Liquidity

- Potential increase in trading volumes as retail investors seek alternatives.

- REITs and dividend‑ paying counters could see inflows, given their yield appeal relative to savings accounts.

📊 Scenario Mapping

| Scenario |

Effect on Funds |

Likely Beneficiaries |

| Retail shifts to equities |

More liquidity in SGX counters |

Banks, REITs, dividend stocks |

| Institutional reallocation |

Larger flows into bonds & structured products |

Fixed income markets |

| Global rate cuts continue |

Sustained move away from deposits |

Growth sectors, yield assets |

⚠ ️ Risks & Trade‑ offs

- Risk Appetite: Not all savers will move funds some prefer safety despite lower returns.

- Global Volatility: If markets remain uncertain (oil, geopolitics), inflows may be muted.

- Competition: Other banks may follow suit, reinforcing the trend but limiting arbitrage.

✅ Takeaway

OCBC&rsquo s rate cut makes savings less rewarding, nudging investors toward

higher‑ yield assets. While not all funds will shift, expect

incremental inflows into equities, REITs, and bonds as investors recalibrate portfolios in a lower‑ rate environment.

YuanLong94 ( Date: 02-Apr-2026 18:50) Posted:

OCBC bank interest cut starting 1st May

more fund will enter market ?

JurongW ( Date: 02-Apr-2026 18:23) Posted:

|

|

|

OCBC bank interest cut starting 1st May

more fund will enter market ?

JurongW ( Date: 02-Apr-2026 18:23) Posted:

newbie2019 ( Date: 02-Apr-2026 18:11) Posted:

|

|

|

newbie2019 ( Date: 02-Apr-2026 18:11) Posted:

Spot on 👍 🏻

JurongW ( Date: 02-Apr-2026 18:05) Posted:

SBB today - 400,000 shares bought at $11.78 to $12.08 ($4,760,263) |

|

|

|

Spot on 👍 🏻

JurongW ( Date: 02-Apr-2026 18:05) Posted:

SBB today - 400,000 shares bought at $11.78 to $12.08 ($4,760,263) |

|

SBB today - 400,000 shares bought at $11.78 to $12.08 ($4,760,263)

Oops should be 8 Apr

JurongW ( Date: 02-Apr-2026 16:30) Posted:

My guess is 400,000 shares. Prob buyback continues until 8 Mar

newbie2019 ( Date: 02-Apr-2026 16:22) Posted:

@JurongW

Today got 500,000 SBB?  |

|

|

|

My guess is 400,000 shares. Prob buyback continues until 8 Mar

newbie2019 ( Date: 02-Apr-2026 16:22) Posted:

@JurongW

Today got 500,000 SBB? |

|