AEM SGD

Last:10.01

-0.08

-0.08

AEM (+Venture, UMS) the most AI-relevant SGX stock

Post Reply

221-240 of 397

Post Reply

221-240 of 397

Recap:

AEM has surged past the 61.8% Fibonacci retracement. If this bullish momentum continues unchecked, the next resistance lies at the 78.6% level around $4.40. Should the rally remain relentless, price could even retest its previous peak near $5.30.

After reading Arogosta post, it is possible for AEM can climb the wall of Wars to $4.40, followed by $5 and then $5.30.

Is this a joke, a dream or reality? Let' s see how the drama unfolds this week.JurongW ( Date: 20-Mar-2026 19:22) Posted:

AEM Technical View

AEM has surged past the 61.8% Fibonacci retracement. If this bullish momentum continues unchecked, the next resistance lies at the 78.6% level around $4.40. Should the rally remain relentless, price could even retest its previous peak near $5.30.

Such a move could unfold before Q1 results, setting up a potential double top formation. A double top is a classic reversal pattern, signaling that an uptrend may be exhausted and a downtrend could follow. Once results are released, the market may react with a &ldquo sell on news&rdquo response, especially if the stock has already run too far, too fast.

For those who missed the initial rally but believe in Arogosta&rsquo s story, patience is key. Wait for confirmation from a shooting star, evening star, or other bearish candlestick signals before considering entry.

Remember: no stock climbs forever. Overbought conditions eventually demand a pause. On the extreme side, the 161.8% Fibonacci extension projects a price close to $8.

This is purely a technical perspective treat it as coffeeshop talk, shared for entertainment rather than investment advice.

|

|

AEM finally living up to its hype:

Aggressively Expanding Margins, and this translates to Already Expecting Millions !

FROM THE BLACK MARKET' S NOTICE BOARD

There&rsquo s a famous saying in the Black Market:

It isn' t just in WHO is buying, but WHAT they are buying.

" A Generational Pivot: The TCS Evolution. While AEM' s expanding clientele portfolio of Big Tech partnerships in well-documented, the true transformation lies deeper. The segment shift isn' t merely in WHO is buying, but in the fundamental nature of WHAT they are buying: moving from standalone hardware to mission-critical, integrated Test Cell Solutions (TCS)."

The Test Cell Solutions (TCS) segment isn' t just a business unit for AEM it' s their " generational pivot." It marks the transition from being a provider of standalone machines to becoming the indispensable architect of the entire semiconductor testing environment.

Here is the breakdown of why TCS is the secret (magic) sauce defining AEM' s future:

1. What exactly is TCS?

a) TCS is an integrated cell that combines three critical components into one automated process: Active Thermal Control (ATC), System Level Test (SLT), High Parallelism Automation.

a) Think of a " Test Cell" as a complete, integrated ecosystem. Instead of just selling a handler (the robot that moves chips), TCS provides the full stack: the thermal control systems, the high-speed electronics, the contactors (sockets), and the software that manages the " handshake" between the chip and the tester. It' s a turnkey laboratory-in-a-box.

2. Is it AEM' s forte and niche?

a) Absolutely. AEM is considered one generation ahead of its competitors in the SLT space. Their specific niche is solving the thermal challenge of AI chips.

b) While competitors often specialize in just one component (like only sockets or only testers), AEM' s forte is System Level Test (SLT) integration. They own the niche of " Massively Parallel Testing," where hundreds of complex chips are tested simultaneously under extreme thermal conditions. No one else integrates these moving parts as seamlessly at scale.

3. The Margin Secret from the Magic Sauce

a) AEM' s value proposition is shifting. By 2026, the Test Cell Solutions (TCS) segment is expected to represent 70% of total revenue (up from 63% in 2025), effectively transitioning the company from a hardware builder to a high-margin tech partner. This segment leverages proprietary PiXL thermal technology, an essential requirement for testing the next generation of high-power AI chips.

b) The Recurring Revenue Model: The magic sauce is the shift from one-time machine sales to a high-margin consumables model. Every chip design change requires new, specialized contactors and change-over kits. AEM isn' t just selling the " printer" they have become the exclusive provider of the " high-precision ink" required for the life of the machine.

4. How important is it to current and future clients?

a) As chips get smaller and more powerful (think AI and 5G), they generate immense heat and are prone to infant mortality (failing early). Clients can no longer rely on simple tests they need the deep, environmental stress testing that TCS provides. For a client like Intel or next-gen AI chipmakers, TCS is the insurance policy that their $1,000 chips won' t fail in a server farm.

b) Future Necessity: As chips move toward 2.5D/3D packaging (stacking multiple chips on top of each other), the chance of a hidden defect increases. Testing each layer individually is too expensive. Big tech companies must move to System Level Testing (SLT) to catch these defects, and AEM currently owns the most advanced automated factory-ready version of this tech.

5. Why it is difficult to copycat?

a) You can' t the just copy a test cell. It requires a rare marriage of mechanical engineering, thermal science, and high-speed signal integrity. AEM has decades of proprietary data on how materials behave at -40° C to +150° C while carrying massive electrical loads. That institutional knowledge is a massive barrier to entry.

b) AEM holds a deep portfolio of patents protecting their thermal control and handler designs. Even if a competitor builds a similar machine, AEM' s software and hardware are already baked into the manufacturing lines of its biggest customers, making it very expensive and risky for a client to switch

6. Keeping the Magic Sauce secret

a) What is a Plan of Record (POR)?: It means the customer has designed their entire manufacturing floor around AEM' s machines. Once AEM is written into a customer' s Plan of Record, they are locked in for the entire lifecycle of chip generation (usually years). Switching vendors would require re-validating the entire testing process, costing millions in delays.

b) The AI Anchor Lock-in: As AI chips become more complex, AEM' s software becomes the brain of the factory floor. This creates a digital lock-in the more data the TCS collects, the better it gets at predicting failures, making AEM' s ecosystem impossible to rip out without blinding the manufacturer.

Sticking with AEM: Brewing Long-Term Gains that keep flowing

a) In short, TCS transforms AEM' s revenue from a lumpy hardware business into a sticky, recurring stream. It' s the " Nespresso Model" of the semiconductor world: the world-class machine gets you through the door, but the high-margin, proprietary pods (the consumables and integration services) keep the revenue flowing for a generation.

b) When analysts like JPMorgan or DBS look at a company, they love " sticky" revenue.

~ With 70% of revenue tie to TCS, AEM is no longer just selling a product they are selling an indispensable service.

~ As AI chips get more powerful (and hotter) in 2027 and 2028, the demand for this specific thermal niche will only intensify.

Essentially, AEM has found the one thing AI chip makers must have to ensure their chips don' t fail, and they' ve patented it.

AEM: Comeback is Real As It Sweeps Intel Award, Stock Skyrockets, DBS Raises Target Price Again

Leong Chan Teik

22 March 2026

After several years of struggling with operational issues, including litigation, and a semiconductor downcycle, AEM Holdings is finally catching its second wind.

AEM is in the midst of a dramatic turnaround, especially since the release of its robust FY25 results in February, evidenced by a surging share price&mdash up approximately 138% year-to-date (from $1.74 to $4.10).

Now, there' s a prestigious nod from its most critical customer, Intel Corp.

AEM (market cap: S$1.3 billion) announced it has received the 2026 Intel EPIC Supplier Award, the highest tier of recognition within Intel&rsquo s global supply chain.

This award, given to only 41 suppliers out of thousands, recognises AEM for its " excellence in quality, technology innovation, operational performance, and continuous improvement."

|

DBS Group Research published a bullish update on March 20, reinforcing the " Buy" case for the stock.

DBS raised its target price to $4.60 (up from $3.30), citing a " valuation uplift" driven by AI tailwinds and successful customer diversification.

That is now the most bullish target, while the targets of other analysts have been surpassed by the stock:

Brokerage

|

Analyst

|

Previous TP

|

New TP

|

DBS

|

Amanda Tan

|

S$3.30

|

S$4.60

|

CGS Int' l

|

William Tng

|

S$1.85

|

S$3.14

|

Maybank

|

Jarick Seet

|

S$1.49

|

S$2.84

|

UOB Kay Hian

|

John Cheong

|

S$1.51

|

S$2.65

|

Key Takeaways From DBS Report:

1. Technological Lead in System Level Test (SLT)

DBS analyst Amanda Tan notes that AEM remains approximately one generation ahead of its competitors in SLT solutions.

As chips become more complex (thanks to 5G, AI, and IoT), the industry requires more intensive testing. AEM&rsquo s " technological superiority" positions it to capture the lion' s share of this growing spend.

2. The Intel " 4nm" Transition

A major driver for AEM is Intel&rsquo s shift toward more advanced nodes.

Intel is currently preparing for the mass production of 4nm chips. These smaller, more complex nodes require significantly longer test times, which directly translates to:

Stock investment guide

-

Higher demand for AEM&rsquo s high-density modular test (HDMT) handlers.

-

Increased revenue from consumables due to higher wear and tear during longer test cycles.

3. Rapid Customer Diversification

AEM is no longer just " the Intel play." DBS highlights that traction with new customers is gaining steam:

-

AI Fabless Customers: Revenue from this segment is expected to more than double in FY26.

-

Memory Customers: Orders for final test handlers are on track, with initial revenues expected in late FY26 ahead of a major production ramp in 2027.

4. The " Hyperscaler" Opportunity

DBS points to a massive, untapped upside: Big Tech " hyperscalers" (cloud providers) are increasingly designing their own silicon.

Currently, many use inefficient lab-style tools for production testing.

AEM&rsquo s high-parallel test equipment is " favourably positioned" to replace these inefficient systems, providing a potential earnings catalyst not yet fully priced into the stock.

| Financial Outlook (FY25&ndash FY27) |

DBS forecasts a powerful earnings recovery, with net profit expected to jump from $17.1m in 2025 to $45.1m by 2027.

While a residual legal overhang and relatively small market cap keep AEM at a slight discount to global peers like Advantest and Teradyne, DBS believes the risk-reward remains " skewed to the upside."

Valuation of global test peers:

Company Name

|

FY End

|

CY-2025

|

CY-2026

|

CY-2027

|

CY-2028

|

Advantest Corporation

|

Mar

|

49.2

|

41.5

|

31.9

|

31.6

|

TERADYNE, INC

|

Dec

|

48.9

|

47.9

|

36.2

|

28.9

|

Chroma Ate Inc.

|

Dec

|

28.2

|

45.6

|

35.3

|

30.3

|

Average

|

|

42.1

|

45.0

|

34.4

|

30.3

|

Source: Visible Alpha, DBS

|

|

I was observing my previous post (below) and in less than 2 hours, it garnered more than 200 views! My other threads couldn' t even get 200 views in one single day........

Which means there seems to be a lot of interest in this stock, so I have to be careful and responsible in what I post! Otherwise, a lot of newbies and less experienced investors might be misled, if they follow the wrong sentiments of the stock.

The true highlight of yesterday' s news developments was actually the confirmation of the Intel " Epic Supplier" award, a move previously speculated upon by the black market. However, retail sentiment was largely distracted by announcement of JPMorgan' s purchase of AEM' s shares and its subsequent emergence as a substantial shareholder. I was also caught up in this retail euphoria and made posts relating to it, but it is important to clarify that this could send the wrong signal.

JPMorgan' s purchase does not represent a proprietary trade using their own capital. Instead, they are facilitating trades on behalf of institutional clients, acting as a nominee and custodian ~ similar to other brokers like UOB Kay Hian, CGSI. Therefore, their " purchase" does not necessarily mean the bank is taking a larger directional stake conversely, a future " sale" may not indicate liquidation, though both are easily misinterpreted by new and seasoned traders alike. This shouldn' t be treated with great significance, but as normal transactions.

We should instead refocus on the Intel award as a primary catalyst. The resulting publicity and goodwill serve as a powerful testimony to attract other Big Tech firms. This could potentially transition companies like Meta and Nvidia from indirect beneficiaries into full-scale anchor clients for AEM. Also, we should be more excited with AEM' s capture of a second major AI/HPC client which is expected to contribute to the bottom line by the end of this fiscal year. These factors should bolster earnings over the next two quarters and provide upward momentum for the stock price. I would not be surprised to see a formal upward revision in revenue guidance, which could further act as the next major catalyst. Remember June last year, AEM experienced a 14.52% share price jump in a single day following the company' s announcement that it was raising its revenue guidance for the first half of FY2025? Imagine, if they do it again before the next half yearly results!

aragosta ( Date: 21-Mar-2026 11:32) Posted:

JPMorgan Adjusted Transaction Log

REPORTED IN SGX FILING

Date of acquisition of or change in interest: 16 March 2026

Purchase 555,000 units at average price of SGD 3.35 per unit via market transaction.

Increase of 77,400 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.183% (up from 4.982%)

Date of acquisition of or change in interest: 17 March 2026

Sale of 910,200 units at average price of SGD 3.53 per unit via market transaction

Increase of 22,300 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 4.901% (down from 5.183%)

YET TO BE REPORTED IN SGX FILING

Date of acquisition of or change in interest: 18 March 2026

Purchase 1,225,400 units at average price of SGD 3.72 per unit via market transaction.

Decrease of 15,800 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.286% (up from 4.901%)

Note: Substantial shareholders have 2 business days to report changes therefore, a transaction occurring on 18 or 19 March

might not appear on the SGX central portal until the following Monday or Tuesday. The above UNDISCLOSED info came from

the coffee shop uncles, which I overheard while having my kopi-o sui tai. Please do not shoot me, if I overheard wrongly hor.......

IMPORTANT TO NOTE! The explicit mention of the Prime Brokerage Agreement in these filings confirms these are client-driven

activities and are not proprietary trades by JPMorgan (using their own cash). They are facilitating the trades of institutional clients,

likely hedge funds, or high-networth clients (I kept telling you this until I got no saliva! Yet gongkias newbies would panick when

they see a sales by JP Morgan).

JPMorgan Chase & Co. typically files as a Substantial Shareholder because the aggregate of its clients' holdings (for which it acts

as a nominee/custodian) exceeds the 5% threshold. |

|

No worries, Ah Gong (T) still holding shares of AEM tight tight.

aragosta ( Date: 21-Mar-2026 11:32) Posted:

JPMorgan Adjusted Transaction Log

REPORTED IN SGX FILING

Date of acquisition of or change in interest: 16 March 2026

Purchase 555,000 units at average price of SGD 3.35 per unit via market transaction.

Increase of 77,400 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.183% (up from 4.982%)

Date of acquisition of or change in interest: 17 March 2026

Sale of 910,200 units at average price of SGD 3.53 per unit via market transaction

Increase of 22,300 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 4.901% (down from 5.183%)

YET TO BE REPORTED IN SGX FILING

Date of acquisition of or change in interest: 18 March 2026

Purchase 1,225,400 units at average price of SGD 3.72 per unit via market transaction.

Decrease of 15,800 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.286% (up from 4.901%)

Note: Substantial shareholders have 2 business days to report changes therefore, a transaction occurring on 18 or 19 March

might not appear on the SGX central portal until the following Monday or Tuesday. The above UNDISCLOSED info came from

the coffee shop uncles, which I overheard while having my kopi-o sui tai. Please do not shoot me, if I overheard wrongly hor.......

IMPORTANT TO NOTE! The explicit mention of the Prime Brokerage Agreement in these filings confirms these are client-driven

activities and are not proprietary trades by JPMorgan (using their own cash). They are facilitating the trades of institutional clients,

likely hedge funds, or high-networth clients (I kept telling you this until I got no saliva! Yet gongkias newbies would panick when

they see a sales by JP Morgan).

JPMorgan Chase & Co. typically files as a Substantial Shareholder because the aggregate of its clients' holdings (for which it acts

as a nominee/custodian) exceeds the 5% threshold. |

|

JPMorgan Adjusted Transaction Log

REPORTED IN SGX FILING

Date of acquisition of or change in interest: 16 March 2026

Purchase 555,000 units at average price of SGD 3.35 per unit via market transaction.

Increase of 77,400 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.183% (up from 4.982%)

Date of acquisition of or change in interest: 17 March 2026

Sale of 910,200 units at average price of SGD 3.53 per unit via market transaction

Increase of 22,300 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 4.901% (down from 5.183%)

YET TO BE REPORTED IN SGX FILING

Date of acquisition of or change in interest: 18 March 2026

Purchase 1,225,400 units at average price of SGD 3.72 per unit via market transaction.

Decrease of 15,800 units pursuant to the Prime Brokerage Agreement

Final interest (Direct plus Deemed) 5.286% (up from 4.901%)

Note: Substantial shareholders have 2 business days to report changes therefore, a transaction occurring on 18 or 19 March

might not appear on the SGX central portal until the following Monday or Tuesday. The above UNDISCLOSED info came from

the coffee shop uncles, which I overheard while having my kopi-o sui tai. Please do not shoot me, if I overheard wrongly hor.......

IMPORTANT TO NOTE! The explicit mention of the Prime Brokerage Agreement in these filings confirms these are client-driven

activities and are not proprietary trades by JPMorgan (using their own cash). They are facilitating the trades of institutional clients,

likely hedge funds, or high-networth clients (I kept telling you this until I got no saliva! Yet gongkias newbies would panick when

they see a sales by JP Morgan).

JPMorgan Chase & Co. typically files as a Substantial Shareholder because the aggregate of its clients' holdings (for which it acts

as a nominee/custodian) exceeds the 5% threshold.

For those who believe in AEM' s growth story and are already on board, this high-energy, high-tempo music could lift your spirits even further.

ENG SUB 動 畫 【 仙 逆 】 王 林 問 鼎 插 曲 《 何 惜 一 戰 》 完 整 版 - 張 申 騁 「 燃 」 | Renegade Immortal OST (EP 121 ED)

From pg 11 report, forecast EPS for AEM for FY26 and FY27 is 10.9 cents and 14.4 cents respectively, highest among peers UMS and Frencken

If shares price is $8, forward PE will be approximately 55times base on FY27 projected earnings. This implies market is pricing aggressive growth expectations.

If earnings growth slows or results underperform, such a high multiple leaves little margin of safety.

Trade‑ offs

Bull case - Investors may justify the premium if they believe AEM technology edge (eg in test equipment for advanced chips) will deliver outsized growth.

Bear case - Valuation looks stretched, especially if Q1 results trigger sell on news behavior after a parabolic run.

Takeaway

A forward P/E of 55x is objectively high for AEM compared to UMS, Frencken, and global peers. It reflects strong optimism but also raises the risk of sharp corrections if growth expectations are not met.

https://www.dbs.com/insightsdirect/api/s3/dbs-buffer/article_attachment/20260320/07-35-27_SG%20Tech%20-%2020mar2026.pdf

AEM Technical View

AEM has surged past the 61.8% Fibonacci retracement. If this bullish momentum continues unchecked, the next resistance lies at the 78.6% level around $4.40. Should the rally remain relentless, price could even retest its previous peak near $5.30.

Such a move could unfold before Q1 results, setting up a potential double top formation. A double top is a classic reversal pattern, signaling that an uptrend may be exhausted and a downtrend could follow. Once results are released, the market may react with a &ldquo sell on news&rdquo response, especially if the stock has already run too far, too fast.

For those who missed the initial rally but believe in Arogosta&rsquo s story, patience is key. Wait for confirmation from a shooting star, evening star, or other bearish candlestick signals before considering entry.

Remember: no stock climbs forever. Overbought conditions eventually demand a pause. On the extreme side, the 161.8% Fibonacci extension projects a price close to $8.

This is purely a technical perspective treat it as coffeeshop talk, shared for entertainment rather than investment advice.

Just like DBS, it could just be another once in a life time stock

Saw this picture..... someone was trying to make a joke out of it.... except it may not be not a joke.......

yesterday price hit $3.84 intraday high...

so if you follow the logical money trail....

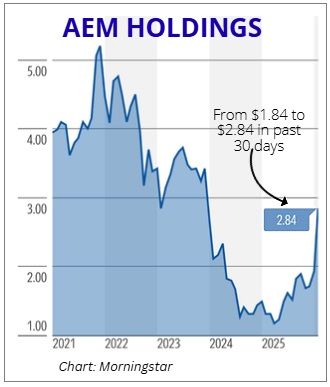

In 30 days, AEM' s price went from $1,84 to $2.84

In 20 days, AEM' s price went from $2.84 to $3.84

in 10 days?

whatever it' s in mind, don' t bet against it, now is $4 plus..... takes another 70c plus

=====

btw, I was trying to post my previous post BEFORE LUNCH' . ....and managed to go thru only a while ago, so the sting of the message was lost in the delay.....

Solubl ( Date: 27-Feb-2026 11:39) Posted:

|

Beautiful article

aragosta ( Date: 20-Mar-2026 15:06) Posted:

Whole day I was walking up and down 52 Serangoon North Avenue 4, hoping some one would recognise me and come up to me..... But alas there were none, it' s like some people just have a nice meal at a 5 star Michelin restaurant and leave with out paying, pretending nothing' s doing...... but it' s okay because I myself was pretending (very hard) too, trying to be humble and try not say a thing to sound like bragging....... but I tell you, it' s very very hard..... very very difficult to stay humble when the stuffs you anyhow talk, somehow turn up to be true!........btw, it hits four now in case you pretending not to notice

Any way, to those very shy believers, I got another coming great news for you, another tokkong development is likely on the way that will rocket this gem even further away from those unbelievers who brag they sold @$3, @$3.38......, this may come as early next month&hellip

today, the news seems to be on JPM, but I tell you, Temasek is working very hard not to be overshadowed......heard it is trying to get another big tech company, in which it has a big stake to join as a high value partner of AEM....this one in fact, the black market is 99% confident will happen soon&hellip ..

On another note, THIS FOLLOWING PIECE IS DEDICATED TO JURONGWEST, one of the few black market believers ...... basically addressing his confusion and concern....... For those who are too lazy to read my lengthy statement below, you may just read the following summary which provide the gist of it......

A LAZY SUMMARY

JPMorgan Chase & Co. became a substantial shareholder in AEM Holdings on March 19, 2026, increasing its stake to 5.19% (16,307,735 shares) following a market acquisition. A significant portion of this holding is managed under a Prime Brokerage Agreement, which allows clients to leverage and borrow shares for trading, yet requires institutional disclosure. JPMorgan' s increased investment indicates strong conviction in AEM' s AI-driven growth trajectory, with FY2026 revenue guidance of S$460M - S$510M and a forward P/E of ~29.4x, suggesting resilience against patent litigation with Advantest. Furthermore, AEM presents a value opportunity, trading at a 25~35% forward P/E discount to industry leaders Advantest and Teradyne.

=========

Here is a structured breakdown of the latest developments regarding JPMorgan' s investment in AEM Holdings as of today, March 20, 2026.

1. The Transaction & Current Stake

On March 19, 2026, JPMorgan Chase & Co. officially crossed the 5% Substantial Shareholder threshold.

~ The Buy: Purchased 555,000 shares in the open market.

~ The Price: An average of S$3.35 per share.

~ Pre-Transaction Stake: 15,629,935 shares (4.97%).

~ AFTER YESTERDAY' S TRANSACTION: Current Stake: 16,307,735 shares (5.19%).

~ Note on Accuracy: The figures from the March 19 SGX Filing are the definitive legal record. Previous higher estimates likely included non-notifiable or " right-to-recall" shares that hadn' t yet triggered a formal disclosure.

2. Understanding the " Prime Brokerage Agreement"

A large portion of JPMorgan' s stake is held under a Prime Brokerage Agreement, simply means &hellip &hellip

~ The Banker' s Role: JPMorgan acts as a " one-stop-shop" for hedge funds and large investors.

~ Deemed Interest: Even if JPMorgan' s clients are the ones buying, Singapore law requires JPMorgan to disclose these shares as a deemed interest because they control the custody and lending of the stock.

~ The Signal: When a Prime Broker' s holding increases, it usually means their most sophisticated, high-networth clients are aggressively " long" on the stock.

~ Newbies' often MISCONCEPTION: So when you see an SGX' s filing by a big institutional fund (like BlackRock, JPM, Goldman Sachs) it DOES NOT necessarily means that that fund is buying for its own &ldquo trading accounts&rdquo . It could well mean it is executing the order on behalf of a high networth client. Got it?

3. The Confidence Factors in the Increase in Stake

JPMorgan' s move to buy at S$3.35 ~ a price significantly higher than the S$2.00 range seen earlier this year ~ signals high conviction in two areas:

~ Growth Inflection: AEM has issued FY2026 revenue guidance of S$460M &ndash S$510M. This is driven by a massive ramp-up from a new AI/High-Performance Computing (HPC) customer that is expected to become their largest revenue source. Multiple sources are persistently stating as of late, many top tech companies have been in need of AEM' s critical high value services.

~ Legal Resilience: By increasing their stake, institutional investors are signaling that the Advantest patent litigation is likely manageable. They likely view AEM' s new thermal testing technology as unique enough to either win in court or reach a settlement that won' t cripple the company' s finances.

4. Why AEM is STILL Undervalued vs. Peers

Despite AEM' s recent price surge, it remains " cheap" when compared to the global semiconductor testing duopoly:

Metric

|

AEM Holdings

|

Advantest (Japan)

|

Teradyne (USA)

|

Forward P/E (FY26)

|

~29.4x

|

~40.5x

|

~45.9x

|

Discount to Peers

|

Baseline

|

27% Premium

|

35% Premium

|

~ The Opportunity: AEM is trading at a 30% average discount to its peers on a forward-earnings basis.

~ Small-Cap Alpha: Because AEM is much smaller (market cap ~S$1.18B), its earnings explosion from new AI contracts has a much bigger impact on its stock price than similar wins would for a US$100B giant like Advantest.

5. The Final Word

JPMorgan' s entry as a substantial shareholder marks a turning point for AEM. By paying S$3.35 per share, the bank is validating AEM' s transition from a legacy Intel-dependent supplier to a diversified AI infrastructure play. While the Advantest lawsuit remains a risk, the Forward P/E discount of nearly 30% compared to global peers suggests that the market has more than priced in the legal uncertainty, leaving significant room for catch-up growth as FY2026 revenue targets are met.

aragosta ( Date: 12-Mar-2026 16:40) Posted:

Smashes through $3.40..... if all goes well, I hope I be allowed to bring you some interesting news next week......

' still want to be iron teeth, and think four is impossible?..... I tell you what, if it crosses four CONVINCINGLY, it may turn into a IFast-que type of boh meh chow...... dyodddd any way... |

|

|

|

Whole day I was walking up and down 52 Serangoon North Avenue 4, hoping some one would recognise me and come up to me..... But alas there were none, it' s like some people just have a nice meal at a 5 star Michelin restaurant and leave with out paying, pretending nothing' s doing...... but it' s okay because I myself was pretending (very hard) too, trying to be humble and try not say a thing to sound like bragging....... but I tell you, it' s very very hard..... very very difficult to stay humble when the stuffs you anyhow talk, somehow turn up to be true!........btw, it hits four now in case you pretending not to notice

Any way, to those very shy believers, I got another coming great news for you, another tokkong development is likely on the way that will rocket this gem even further away from those unbelievers who brag they sold @$3, @$3.38......, this may come as early next month&hellip

today, the news seems to be on JPM, but I tell you, Temasek is working very hard not to be overshadowed......heard it is trying to get another big tech company, in which it has a big stake to join as a high value partner of AEM....this one in fact, the black market is 99% confident will happen soon&hellip ..

On another note, THIS FOLLOWING PIECE IS DEDICATED TO JURONGWEST, one of the few black market believers ...... basically addressing his confusion and concern....... For those who are too lazy to read my lengthy statement below, you may just read the following summary which provide the gist of it......

A LAZY SUMMARY

JPMorgan Chase & Co. became a substantial shareholder in AEM Holdings on March 19, 2026, increasing its stake to 5.19% (16,307,735 shares) following a market acquisition. A significant portion of this holding is managed under a Prime Brokerage Agreement, which allows clients to leverage and borrow shares for trading, yet requires institutional disclosure. JPMorgan' s increased investment indicates strong conviction in AEM' s AI-driven growth trajectory, with FY2026 revenue guidance of S$460M - S$510M and a forward P/E of ~29.4x, suggesting resilience against patent litigation with Advantest. Furthermore, AEM presents a value opportunity, trading at a 25~35% forward P/E discount to industry leaders Advantest and Teradyne.

=========

Here is a structured breakdown of the latest developments regarding JPMorgan' s investment in AEM Holdings as of today, March 20, 2026.

1. The Transaction & Current Stake

On March 19, 2026, JPMorgan Chase & Co. officially crossed the 5% Substantial Shareholder threshold.

~ The Buy: Purchased 555,000 shares in the open market.

~ The Price: An average of S$3.35 per share.

~ Pre-Transaction Stake: 15,629,935 shares (4.97%).

~ AFTER YESTERDAY' S TRANSACTION: Current Stake: 16,307,735 shares (5.19%).

~ Note on Accuracy: The figures from the March 19 SGX Filing are the definitive legal record. Previous higher estimates likely included non-notifiable or " right-to-recall" shares that hadn' t yet triggered a formal disclosure.

2. Understanding the " Prime Brokerage Agreement"

A large portion of JPMorgan' s stake is held under a Prime Brokerage Agreement, simply means &hellip &hellip

~ The Banker' s Role: JPMorgan acts as a " one-stop-shop" for hedge funds and large investors.

~ Deemed Interest: Even if JPMorgan' s clients are the ones buying, Singapore law requires JPMorgan to disclose these shares as a deemed interest because they control the custody and lending of the stock.

~ The Signal: When a Prime Broker' s holding increases, it usually means their most sophisticated, high-networth clients are aggressively " long" on the stock.

~ Newbies' often MISCONCEPTION: So when you see an SGX' s filing by a big institutional fund (like BlackRock, JPM, Goldman Sachs) it DOES NOT necessarily means that that fund is buying for its own &ldquo trading accounts&rdquo . It could well mean it is executing the order on behalf of a high networth client. Got it?

3. The Confidence Factors in the Increase in Stake

JPMorgan' s move to buy at S$3.35 ~ a price significantly higher than the S$2.00 range seen earlier this year ~ signals high conviction in two areas:

~ Growth Inflection: AEM has issued FY2026 revenue guidance of S$460M &ndash S$510M. This is driven by a massive ramp-up from a new AI/High-Performance Computing (HPC) customer that is expected to become their largest revenue source. Multiple sources are persistently stating as of late, many top tech companies have been in need of AEM' s critical high value services.

~ Legal Resilience: By increasing their stake, institutional investors are signaling that the Advantest patent litigation is likely manageable. They likely view AEM' s new thermal testing technology as unique enough to either win in court or reach a settlement that won' t cripple the company' s finances.

4. Why AEM is STILL Undervalued vs. Peers

Despite AEM' s recent price surge, it remains " cheap" when compared to the global semiconductor testing duopoly:

Metric

|

AEM Holdings

|

Advantest (Japan)

|

Teradyne (USA)

|

Forward P/E (FY26)

|

~29.4x

|

~40.5x

|

~45.9x

|

Discount to Peers

|

Baseline

|

27% Premium

|

35% Premium

|

~ The Opportunity: AEM is trading at a 30% average discount to its peers on a forward-earnings basis.

~ Small-Cap Alpha: Because AEM is much smaller (market cap ~S$1.18B), its earnings explosion from new AI contracts has a much bigger impact on its stock price than similar wins would for a US$100B giant like Advantest.

5. The Final Word

JPMorgan' s entry as a substantial shareholder marks a turning point for AEM. By paying S$3.35 per share, the bank is validating AEM' s transition from a legacy Intel-dependent supplier to a diversified AI infrastructure play. While the Advantest lawsuit remains a risk, the Forward P/E discount of nearly 30% compared to global peers suggests that the market has more than priced in the legal uncertainty, leaving significant room for catch-up growth as FY2026 revenue targets are met.

aragosta ( Date: 12-Mar-2026 16:40) Posted:

Smashes through $3.40..... if all goes well, I hope I be allowed to bring you some interesting news next week......

' still want to be iron teeth, and think four is impossible?..... I tell you what, if it crosses four CONVINCINGLY, it may turn into a IFast-que type of boh meh chow...... dyodddd any way....

aragosta ( Date: 26-Feb-2026 14:36) Posted:

If u want to play AEM, go for long term, and ignore the current fundamental data and figures... they' re irrelevant.......I say again....FOUR is not a joke! And we are talking about short term to mini mid term only..... same as UMS, FOUR is not playing a fool, next week will be its turn to shine, pity those who throw away their bonus shares.... literally throw away!!!

AEM' s Turnaround Story

When investors buy a stock like AEM Holdings despite a high P/E, low yield, and low NAV (trading well above book value), they are not looking at what the company is today, but what it will become tomorrow. They are discounting the present to price in a high-conviction growth story. They are trading current income for a structural turnaround centered on AI integration and the semiconductor industry' s cyclical recovery.

Why Investors Are Buying AEM (The " Turnaround Story" )

1. Forward Earnings Pivot

Investors ignore the Trailing P/E (past performance) and focus on the much power Forward P/E. They are betting that projected earnings for 2026/2027 will surge, making today' s " expensive" price a relative bargain.

2. Structural Turnaround

AEM is transitioning from a cyclical slump to a growth phase. The market rewards the inflection point ~ the moment a company proves the " worst is over" ~ more aggressively than the actual profit numbers themselves.

3. AI & HPC Revenue Ramp

AEM' s shift toward High-Performance Computing (HPC) and AI customers validates its technology. This provides a " pick and shovel" play for the AI boom, which carries a higher valuation premium than legacy business. Investors are betting that demand for their advanced testing equipment will skyrocket. (Please read below all my notes on AEM, which I took so much trouble to sneak out the middle of the night to steal from those coffee shops and mafia&rsquo s vaults)

4. Expansion into New Markets

The validation of AEM' s Memory Test capabilities opens a massive new revenue stream. Success in the Memory Test segment represents a massive expansion of the company' s Total Addressable Market (TAM), which is not yet reflected in the current low NAV or Book Value. Investors are pricing in this future dominance before the revenue fully hits the balance sheet.

5. Signal of Confidence

Despite the low dividend yield, the resumption of payouts is a strategic signal. It confirms management' s confidence in cash flow stability and indicates that the worst of the cyclical downturn has passed, and is confident enough in the 2026 outlook to return capital to shareholders.

6. Operating Leverage & Margins

As a high-tech manufacturer, AEM possesses significant operating leverage. Once fixed costs are covered, a recovery in sales volume leads to an exponential increase in net profit margins. Investors are buying in anticipation of this margin expansion.

7.Intagible Value

A low NAV relative to price suggests the market is valuing intellectual property and " moats" over physical assets. Investors are paying for AEM' s proprietary testing technology, which is not easily captured on a traditional balance sheet

|

|

|

|

You&rsquo re right to challenge whether

EPS of 16&ndash 18 cents in FY2026 is realistic compared to

FY2025&rsquo s ~5 cents. On the surface, that looks like a huge jump&mdash more than triple. Let&rsquo s break down why analysts think it&rsquo s possible, and where the risks lie.

📊 FY2025 vs FY2026 EPS

- FY2025 EPS: ~SGD 0.045&ndash 0.05 (net profit ~SGD 20m).

- FY2026 Projection: ~SGD 0.16&ndash 0.18 (net profit ~SGD 70&ndash 80m).

That&rsquo s a

3&ndash 4x increase in earnings year-on-year.

⚖ ️ Why Analysts See It as Plausible

-

Revenue Ramp-Up:

- FY2025 revenue: SGD 399m.

- FY2026 guidance: SGD 460&ndash 510m (up ~15&ndash 28%).

-

Margin Expansion:

- FY2025 net margin: ~5%.

- FY2026 expected margin: ~15&ndash 16% (due to higher volumes, better product mix, and new customer ramp).

-

Customer Diversification:

- AEM&rsquo s second major AI/HPC customer contributed > 25% of FY2025 revenue.

- This new client is expected to scale significantly in FY2026, reducing reliance on Intel.

📌 Risks to Watch

- Execution Risk: If the new customer&rsquo s ramp is slower, EPS could undershoot (closer to 12&ndash 14 cents).

- Margin Pressure: Semiconductor cycles are volatile&mdash if margins don&rsquo t expand as expected, EPS growth will be muted.

- Valuation Sensitivity: At SGD 4.02, forward P/E looks reasonable (~22&ndash 25x), but only if EPS really hits 16&ndash 18 cents.

🔍 Calibration Table

| Scenario |

Revenue (SGD m) |

Net Margin |

Net Profit (SGD m) |

EPS (SGD) |

Forward P/E (at 4.02) |

| Bear |

460 |

10% |

46 |

0.105 |

38.3 |

| Base |

485 |

15% |

72.8 |

0.165 |

24.4 |

| Bull |

510 |

16% |

81.6 |

0.185 |

21.7 |

🎯 Takeaway

- Yes, 16&ndash 18 cents is aggressive but plausible if margins triple from FY2025 levels.

- The leap looks dramatic only because FY2025 EPS was unusually low due to margin compression.

- The market is already pricing in this rebound&mdash if AEM misses, valuation could look stretched again.