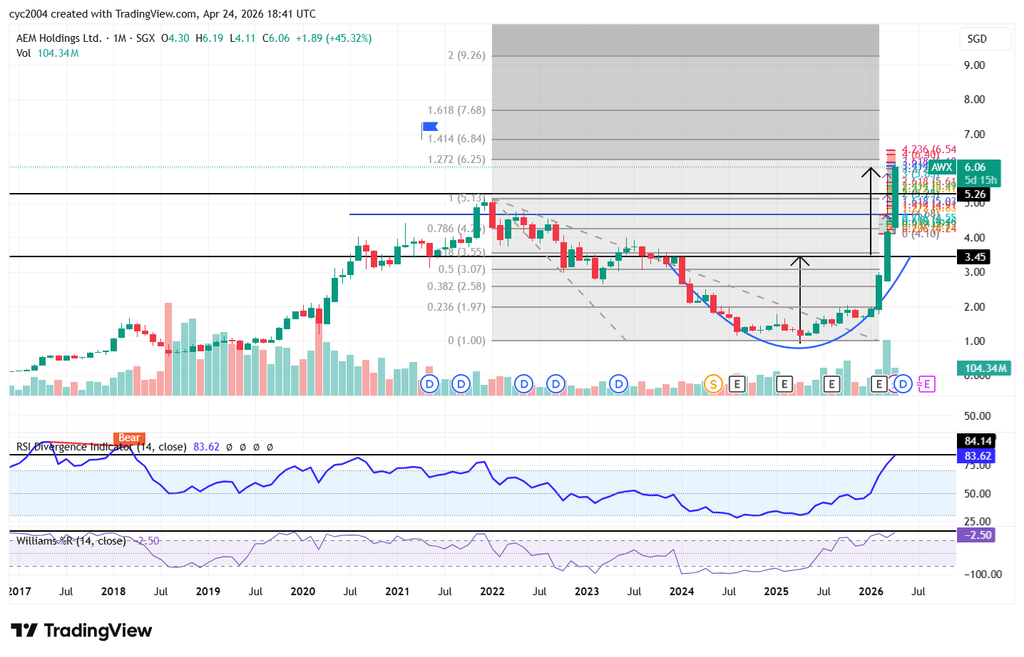

Coincidence or confluence?

The 1.414 Fibonacci extension lands exactly at $6.84.

The 1.414 Fibonacci extension lands exactly at $6.84.

aragosta ( Date: 25-Apr-2026 00:53) Posted:

|

spot on SGWealthBuilder

tongphlp ( Date: 15-Apr-2026 13:28) Posted:

|

No worries lah........As long as it got legs to run, it' s fine with me.....

tongphlp ( Date: 23-Apr-2026 10:40) Posted:

|

ASE Breaks Ground on New Renwu Plant to Build Hi-tech Testing Cluster

KAOHSIUNG, Taiwan, April 10, 2026 &ndash Advanced Semiconductor Engineering, Inc. (ASE, a member of ASE Technology Holdings Inc, NYSE: ASX, TWSE: 3711) held a groundbreaking ceremony for its new facility in the Renwu Industrial Park today. This joint investment, featuring partners WinWay Technology Co., Ltd. and HORNG TERNG AUTOMATION CO., LTD. (HTT), aims to establish a hi-tech semiconductor testing services cluster. The project is expected to create over 1,000 jobs as ASE continues to expand its investment in Taiwan, positioning Kaohsiung as a key hub to bolster Taiwan&rsquo s leadership in the global semiconductor industry.

&ldquo The global semiconductor industry has entered a critical phase of transformation. In response to the evolving global supply chain, ASE is proactively driving industrial upgrades. The commencement of the Renwu plant serves as a vital economic engine and a beacon of technological leadership,&rdquo says Dr. Tien Wu, CEO of ASE.

Key highlights of the investment include:

- Capital Investment: Over NT$108.3 billion

- Projected Annual Output: Approximately NT$177.3 billion upon full operation

- Smart Manufacturing: The facility will integrate AI smart manufacturing, including visual cloud inspection systems and fully automated AGVs (Automated Guided Vehicles)

- Sustainability: Designed in compliance with the Kaohsiung Green Building Autonomy Ordinance, the factory will utilize clean production assessments to achieve a &ldquo green energy, zero-pollution&rdquo smart factory status

Looking ahead, ASE will provide comprehensive wafer and chip testing services at the Renwu site.

- Phase I: Scheduled to begin operations in April 2027

- Phase II: Expansion and operations expected by October 2027

The eco-friendly, high-tech green building underscores ASE&rsquo s commitment to its net-zero transition. It also aims to attract and retain top semiconductor talent in Kaohsiung by creating high-value job opportunities, while fostering a powerful collaboration across industry, government, and academia.

Strengthening the &ldquo Semiconductor S Corridor &rdquo and Taiwan&rsquo s Silicon Shield

With over 40 years of deep roots in Taiwan, ASE continues to refine manufacturing processes, enhance yields, and advance automation. By embedding sustainability and digital transformation across its supply chain, ASE&rsquo s collaboration with WinWay and HTT in Renwu drives the localization of key components and hi-tech advanced packaging equipment.

This strategic move is a key component in advancing the Kaohsiung City Government&rsquo s Silicon Photonics ecosystem and the broader Southern Semiconductor S Corridor. By shortening supply chain distances and strengthening technical capabilities, it reinforces the resilience and global significance of Taiwan&rsquo s Silicon Shield.

Article re-produced from SG Wealth Builder.

DYODD

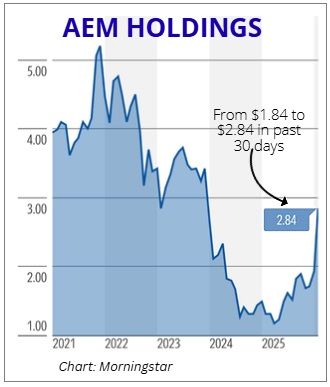

Is this for real? For the past few weeks, I have been pinching myself to check if I am dreaming as AEM share price stormed back in an unbelievable manner. Within a year, AEM share price rocketed nearly 5-folds. Year-to-date, the counter surged 160%.

Though I had conviction that this day will surely arrive, it still feels so unreal when it happened. This stock has given me so much heartbreaks and heart pains for the past 4 years. So you can imagine the bittersweet feeling when AEM share price returned to its swashbuckling form again. It really feels so surreal!

The explosive form of AEM shares price certainly caught the attention of the investment community as various analysts scrambled to revise new target prices for AEM. Personally, my investment in AEM is still in the red due to the fact that I had entered this counter at a high of $5.22 in 2022. However, given the robust form, I will not be surprised that AEM share price will surge past my breakeven investment level and hit $6 next week.

Apparently, the buoyant AEM share price is driven by institutional purchases. On 19 March 2026, the market went into tailspin when it emerged that JP Morgan became a substantial shareholder, having obtained 5.19% stake in AEM from open market purchases. However, the investment bank subsequently trimmed its stake to 4.9% a couple of days later and ceased to be a substantial shareholder. In my view, this enabled JP Morgan to buy and sell AEM shares without the need to make SGX filings, suggesting that the bank is trading the volatility.

The shock investment by JP Morgan had obviously raised plenty of eyebrows and injected significant confidence in AEM share price. For the past few years, with the exception of Temasek Holdings, various substantial shareholders like EPF and Aberdeen had either exited or trimmed their stakes due to the various misadventures of AEM &ndash legal suits by Advantest, inventory mess and over-reliance on Intel. The recent news of successful business diversification must have attracted institutional players to AEM.

After years of heavy investment in R& D, AEM managed to achieve success in diversifying its customer base through secure of new customers. In its FY2025 results (released Feb 2026), AEM highlighted growth from a second AI/HPC customer (distinct from the new anchor and Intel) that is ramping up high-volume manufacturing. This data confirms that they now have at least two major players in the AI/HPC space in addition to Intel.

AEM also mentioned that demand from the second AI/HPC remains robust and that &ldquo revenue contribution is anticipated to grow significantly in FY2026, en route to becoming the Group&rsquo s new top customer by revenue&rdquo .

To put the icing on the cake, ASE subscribe for $12 million of new AEM shares. In addition, ASE, through said subsidiary, will also receive a total of 28,111,856 million free detachable warrants. If fully exercised, the warrants would result in an additional 8.935% of the current issued share capital. ASE is a leading provider of semiconductor assembly, testing and materials (&ldquo ATM&rdquo ) services and the provider of electronic manufacturing (&ldquo EMS&rdquo ) services.In this blog, I have always maintained that on its day, AEM share price can be unbeatable. Conversely, when the tide goes against AEM share price, the counter can spiral out of control. On this note, this counter is really not for the faint-hearted. Note that this is an opinion article and not meant to be a financial advice. Please do your due diligence or engage financial advisors before investing in the stock market. I am vested in this counter, so my views on AEM share price may be biased.

AEM share price still a $10 stock?

The explosive form of AEM share price saw its market capitalization crossing $1.4 billion, signaling the return of the king as the Group makes up for lost time. At the going rate, AEM is on course to hit the previous peak of $5 last seen in 2022. Honestly, I have been waiting for this day for so long. There were sleepless nights and moments of doubts, fear and anger. During this period, I have been asking myself what went wrong with my hypothesis at least 2000 times.

Previously, I have written that 2026 would be a &ldquo make or break&rdquo year for AEM share price. It turns out that my prediction was quite accurate given the recent supersonic form of the counter. With the emergence of JP Morgan and ASE as new shareholders, things are getting pretty interesting.

Back in 2022-2023, investment bank Morgan Stanley and institutional players like Aberdeen and Malaysia EPF were still substantial shareholders of AEM. That was the period when rumours were rift of AEM being on its way to being listed in Nasdaq due to the presence of investment bank Morgan Stanley.

&zwnj However, Chairman Loke Wai San wasn&rsquo t supportive of the idea as he felt that the time was not right given that the market cap of AEM was less than US$1 billion. Subsequently, Morgan Stanley, Templeton and EPF all sold off their stakes in AEM and ceased to be the substantial shareholders after Intel fell into troubles. Now with JP Morgan and Temasek Holdings as backers, will AEM become one of the first few homegrown companies to be dual-listed in Nasdaq and SGX?

&zwnj The impetus for a Nasdaq listing should be for marketing purposes. Being listed in SGX, AEM has limited access to the US market. This is unlike its competitors, Cohu, Teradyne and Advantest, which are all listed in US stock markets. Therefore, the listing in Nasdaq is really critical in enabling AEM to secure new major customers that could allow AEM sustain after its partnership with Intel sunsets. If the execution is right, there is also the possibility of AEM share price hitting the giddy height of $10 via a dual-listing in US stock market.

Turned the corner

While investor&rsquo s confidence has returned, one thing that has been bugging me consistently is whether AEM has truly addressed its inventory shortfall crisis in 2024. Back then, news of the inventory mess caused short selling activities against the counter to swell to a mind-boggling 2.7 million on 15 January. That fiasco caused AEM share price to plummet from $3.40 in January 2024 to a low of $1.20 in August 2024.

However, FY2025 financial result showed that AEM might have finally turned the corner successfully as the company reduced its inventory by $65.7 million, working through the stockpiles that had plagued its balance sheet. Net cash flow from operating activities was a positive $133 million for FY2025 vis-à -vis negative $17.5 million in FY2024.

On the other hand, AEM also announced on 19 March 2026 that it had received the 2026 Intel EPIC Supplier Award. This is the highest supplier recognition from Intel for the supplier&rsquo s performance, innovation, and collaboration within Intel&rsquo s global supply chain. AEM is among the only 41 suppliers out of the thousands of Intel&rsquo s suppliers to receive the EPIC Supplier Award.

The EPIC award affirms that AEM remains a top-tier equipment supplier of Intel. It also serves as an important bridge for AEM to enter Intel Foundry Services (IFS) ecosystem. Traditionally, Intel build its own manufacturing plant for its own chips and AEM is its supplier to test its chips. As Intel pivots to manufacturing chips for others like Nvidia, Microsoft or Amazon via IFS, AEM&rsquo s System Level Test equipment would be used to test Intel&rsquo s customers&rsquo chips.

All road leads to R& D

The ongoing patent dispute with Advantest vindicates my belief that the key battle in semiconductor industry lies in the intellectual property. AEM&rsquo s proprietary Thermal Control Technology is considered its &ldquo crown jewel&rdquo that provides the company the competitive advantage to gain market share. As AI and High-Performance Computing (HPC) chips become more powerful, they generate extreme heat. AEM&rsquo s patented ability to test these chips under precise thermal conditions without damage has allowed it to win major contracts with &ldquo next-gen&rdquo AI customers, diversifying away from its historical reliance on Intel

In 2025, AEM continued to double down on R& D activities as the R& D expenses increased 1% to $23.8 million. The investment appears to pay off as the FY2025 revenue hit S$399 million, driven by a &ldquo second major AI/HPC customer&rdquo which now accounts for over 25% of their Test Cell revenue.

On the other hand, AEM is embroiled in yet another lawsuit from AEM&rsquo s competitor, Advantest, who is suing AEM over alleged infringement of 2 patents relating to wafer-level test systems.

AEM claims that the patents relate to a specific wafer level test system that is not practiced by the company and that it strongly denies the allegations in Advantest&rsquo s complaint. AEM has already retained U.S. counsel to defend itself against Advantest&rsquo s claims, which lack merit.

It all seems like dé jà vu to me as the Advantest has previously sued AEM over patent infringement in 2021. In that saga, AEM has paid Advantest US$20 million in two instalments. Additionally, that was a long drawn-out legal battle, causing AEM to incur massive legal fees. According to DBS research, AEM incurred $11.1 million/$27.0 million/$9.0 million in FY21/22/23 vs $5.1 million in FY20 and $9.2 million in FY24. Both the legal fees and arbitration settlement have weighed on AEM&rsquo s financial performance in recent years, plunging the company into turmoil.

The company also maintained that &ldquo the filing of Advantest&rsquo s latest complaint does not affect AEM&rsquo s business operations, its existing commercial offerings or products, or its ongoing ability to serve its customers. The Company maintains its revenue guidance for 2H 2025 as previously announced on 13 Aug 2025&rdquo . Notwithstanding the stance made by AEM, I do think that its too premature to claim that the latest lawsuit will not have material impact on the reputation of AEM given that it is still a relatively unknown player in the global stage. For this reason, I do think that investors should thread with caution.

&zwnj Conclusion

It is not a secret that AEM has been struggling to turn around the corner for the past few years. Despite the challenges, Temasek Holdings has not trimmed its stake in AEM. This is unlike the rest of the substantial shareholders like Malaysia&rsquo s EPF and Aberdeen, which had pared down their stakes in AEM in the past few years in order to reduce their risk exposures. The steadfast conviction of Temasek Holdings in AEM might be puzzling for many investors. Yet, in my perspective, I believe that conviction could be driven by Singapore&rsquo s government.

If you look back over the decades, Singapore has not produced many innovative products at the global market stage, probably due to the very small talent pool. Against this backdrop, AEM Holdings must have attracted the attention of the Singapore government with its various technology patents to support the System Level Test 2.0 solutions for the semiconductor industry

Those who had sold off their stakes in AEM were either disillusioned with the business performances of the company or have moved on to other counters which may provide better returns. I would be lying if I said that the thought of exiting this counter has not crossed my mind but cutting losses is not an option for me as the losses that would be incurred would be substantial.

The macro-economic fundamentals have turned favorably for AEM but the looming Advantest lawsuit could throw a spanner in the works for AEM&rsquo s business recovery. That said, the long-term potential of AEM is there but existing investors need to have strong holding power to withstand this winter. In this regard, I am cautiously optimistic that AEM share price may hit $7 in 2026. Till then, enjoy the ride.

DYODD

AEM share price in massive comeback

Is this for real? For the past few weeks, I have been pinching myself to check if I am dreaming as AEM share price stormed back in an unbelievable manner. Within a year, AEM share price rocketed nearly 5-folds. Year-to-date, the counter surged 160%.

Though I had conviction that this day will surely arrive, it still feels so unreal when it happened. This stock has given me so much heartbreaks and heart pains for the past 4 years. So you can imagine the bittersweet feeling when AEM share price returned to its swashbuckling form again. It really feels so surreal!

The explosive form of AEM shares price certainly caught the attention of the investment community as various analysts scrambled to revise new target prices for AEM. Personally, my investment in AEM is still in the red due to the fact that I had entered this counter at a high of $5.22 in 2022. However, given the robust form, I will not be surprised that AEM share price will surge past my breakeven investment level and hit $6 next week.

Apparently, the buoyant AEM share price is driven by institutional purchases. On 19 March 2026, the market went into tailspin when it emerged that JP Morgan became a substantial shareholder, having obtained 5.19% stake in AEM from open market purchases. However, the investment bank subsequently trimmed its stake to 4.9% a couple of days later and ceased to be a substantial shareholder. In my view, this enabled JP Morgan to buy and sell AEM shares without the need to make SGX filings, suggesting that the bank is trading the volatility.

The shock investment by JP Morgan had obviously raised plenty of eyebrows and injected significant confidence in AEM share price. For the past few years, with the exception of Temasek Holdings, various substantial shareholders like EPF and Aberdeen had either exited or trimmed their stakes due to the various misadventures of AEM &ndash legal suits by Advantest, inventory mess and over-reliance on Intel. The recent news of successful business diversification must have attracted institutional players to AEM.

After years of heavy investment in R& D, AEM managed to achieve success in diversifying its customer base through secure of new customers. In its FY2025 results (released Feb 2026), AEM highlighted growth from a second AI/HPC customer (distinct from the new anchor and Intel) that is ramping up high-volume manufacturing. This data confirms that they now have at least two major players in the AI/HPC space in addition to Intel.

AEM also mentioned that demand from the second AI/HPC remains robust and that &ldquo revenue contribution is anticipated to grow significantly in FY2026, en route to becoming the Group&rsquo s new top customer by revenue&rdquo .

To put the icing on the cake, ASE subscribe for $12 million of new AEM shares. In addition, ASE, through said subsidiary, will also receive a total of 28,111,856 million free detachable warrants. If fully exercised, the warrants would result in an additional 8.935% of the current issued share capital. ASE is a leading provider of semiconductor assembly, testing and materials (&ldquo ATM&rdquo ) services and the provider of electronic manufacturing (&ldquo EMS&rdquo ) services.In this blog, I have always maintained that on its day, AEM share price can be unbeatable. Conversely, when the tide goes against AEM share price, the counter can spiral out of control. On this note, this counter is really not for the faint-hearted. Note that this is an opinion article and not meant to be a financial advice. Please do your due diligence or engage financial advisors before investing in the stock market. I am vested in this counter, so my views on AEM share price may be biased.

AEM share price still a $10 stock?

The explosive form of AEM share price saw its market capitalization crossing $1.4 billion, signaling the return of the king as the Group makes up for lost time. At the going rate, AEM is on course to hit the previous peak of $5 last seen in 2022. Honestly, I have been waiting for this day for so long. There were sleepless nights and moments of doubts, fear and anger. During this period, I have been asking myself what went wrong with my hypothesis at least 2000 times.

Previously, I have written that 2026 would be a &ldquo make or break&rdquo year for AEM share price. It turns out that my prediction was quite accurate given the recent supersonic form of the counter. With the emergence of JP Morgan and ASE as new shareholders, things are getting pretty interesting.

Back in 2022-2023, investment bank Morgan Stanley and institutional players like Aberdeen and Malaysia EPF were still substantial shareholders of AEM. That was the period when rumours were rift of AEM being on its way to being listed in Nasdaq due to the presence of investment bank Morgan Stanley.

&zwnj However, Chairman Loke Wai San wasn&rsquo t supportive of the idea as he felt that the time was not right given that the market cap of AEM was less than US$1 billion. Subsequently, Morgan Stanley, Templeton and EPF all sold off their stakes in AEM and ceased to be the substantial shareholders after Intel fell into troubles. Now with JP Morgan and Temasek Holdings as backers, will AEM become one of the first few homegrown companies to be dual-listed in Nasdaq and SGX?

&zwnj The impetus for a Nasdaq listing should be for marketing purposes. Being listed in SGX, AEM has limited access to the US market. This is unlike its competitors, Cohu, Teradyne and Advantest, which are all listed in US stock markets. Therefore, the listing in Nasdaq is really critical in enabling AEM to secure new major customers that could allow AEM sustain after its partnership with Intel sunsets. If the execution is right, there is also the possibility of AEM share price hitting the giddy height of $10 via a dual-listing in US stock market.

Turned the corner

While investor&rsquo s confidence has returned, one thing that has been bugging me consistently is whether AEM has truly addressed its inventory shortfall crisis in 2024. Back then, news of the inventory mess caused short selling activities against the counter to swell to a mind-boggling 2.7 million on 15 January. That fiasco caused AEM share price to plummet from $3.40 in January 2024 to a low of $1.20 in August 2024.

However, FY2025 financial result showed that AEM might have finally turned the corner successfully as the company reduced its inventory by $65.7 million, working through the stockpiles that had plagued its balance sheet. Net cash flow from operating activities was a positive $133 million for FY2025 vis-à -vis negative $17.5 million in FY2024.

On the other hand, AEM also announced on 19 March 2026 that it had received the 2026 Intel EPIC Supplier Award. This is the highest supplier recognition from Intel for the supplier&rsquo s performance, innovation, and collaboration within Intel&rsquo s global supply chain. AEM is among the only 41 suppliers out of the thousands of Intel&rsquo s suppliers to receive the EPIC Supplier Award.

The EPIC award affirms that AEM remains a top-tier equipment supplier of Intel. It also serves as an important bridge for AEM to enter Intel Foundry Services (IFS) ecosystem. Traditionally, Intel build its own manufacturing plant for its own chips and AEM is its supplier to test its chips. As Intel pivots to manufacturing chips for others like Nvidia, Microsoft or Amazon via IFS, AEM&rsquo s System Level Test equipment would be used to test Intel&rsquo s customers&rsquo chips.

All road leads to R& D

The ongoing patent dispute with Advantest vindicates my belief that the key battle in semiconductor industry lies in the intellectual property. AEM&rsquo s proprietary Thermal Control Technology is considered its &ldquo crown jewel&rdquo that provides the company the competitive advantage to gain market share. As AI and High-Performance Computing (HPC) chips become more powerful, they generate extreme heat. AEM&rsquo s patented ability to test these chips under precise thermal conditions without damage has allowed it to win major contracts with &ldquo next-gen&rdquo AI customers, diversifying away from its historical reliance on Intel

In 2025, AEM continued to double down on R& D activities as the R& D expenses increased 1% to $23.8 million. The investment appears to pay off as the FY2025 revenue hit S$399 million, driven by a &ldquo second major AI/HPC customer&rdquo which now accounts for over 25% of their Test Cell revenue.

On the other hand, AEM is embroiled in yet another lawsuit from AEM&rsquo s competitor, Advantest, who is suing AEM over alleged infringement of 2 patents relating to wafer-level test systems.

AEM claims that the patents relate to a specific wafer level test system that is not practiced by the company and that it strongly denies the allegations in Advantest&rsquo s complaint. AEM has already retained U.S. counsel to defend itself against Advantest&rsquo s claims, which lack merit.

It all seems like dé jà vu to me as the Advantest has previously sued AEM over patent infringement in 2021. In that saga, AEM has paid Advantest US$20 million in two instalments. Additionally, that was a long drawn-out legal battle, causing AEM to incur massive legal fees. According to DBS research, AEM incurred $11.1 million/$27.0 million/$9.0 million in FY21/22/23 vs $5.1 million in FY20 and $9.2 million in FY24. Both the legal fees and arbitration settlement have weighed on AEM&rsquo s financial performance in recent years, plunging the company into turmoil.

The company also maintained that &ldquo the filing of Advantest&rsquo s latest complaint does not affect AEM&rsquo s business operations, its existing commercial offerings or products, or its ongoing ability to serve its customers. The Company maintains its revenue guidance for 2H 2025 as previously announced on 13 Aug 2025&rdquo . Notwithstanding the stance made by AEM, I do think that its too premature to claim that the latest lawsuit will not have material impact on the reputation of AEM given that it is still a relatively unknown player in the global stage. For this reason, I do think that investors should thread with caution.

&zwnj Conclusion

It is not a secret that AEM has been struggling to turn around the corner for the past few years. Despite the challenges, Temasek Holdings has not trimmed its stake in AEM. This is unlike the rest of the substantial shareholders like Malaysia&rsquo s EPF and Aberdeen, which had pared down their stakes in AEM in the past few years in order to reduce their risk exposures. The steadfast conviction of Temasek Holdings in AEM might be puzzling for many investors. Yet, in my perspective, I believe that conviction could be driven by Singapore&rsquo s government.

If you look back over the decades, Singapore has not produced many innovative products at the global market stage, probably due to the very small talent pool. Against this backdrop, AEM Holdings must have attracted the attention of the Singapore government with its various technology patents to support the System Level Test 2.0 solutions for the semiconductor industry

Those who had sold off their stakes in AEM were either disillusioned with the business performances of the company or have moved on to other counters which may provide better returns. I would be lying if I said that the thought of exiting this counter has not crossed my mind but cutting losses is not an option for me as the losses that would be incurred would be substantial.

The macro-economic fundamentals have turned favorably for AEM but the looming Advantest lawsuit could throw a spanner in the works for AEM&rsquo s business recovery. That said, the long-term potential of AEM is there but existing investors need to have strong holding power to withstand this winter. In this regard, I am cautiously optimistic that AEM share price may hit $7 in 2026. Till then, enjoy the ride.

Have trust in Arogosta and the Mafia

This beauty didn' t hit $4.84 in 10 days.... But it was close enuf, it did it in 15 days......so in another 10 days, can we expect the same pattern? Maybe, if it coincides with the convincingly ending of the conflict......and that' s not all, if the gangsters are to be believed, besides the brewing development that has nothing to do with a contract win, and which I mentioned earlier, there is also another news of a possible incoming new customer, with the help of a partner........ there' s not much interest in here anyway, so I shouldn' t be talking too much on this,... in any case, write so much, also nobody read, also one-ime dissident ah tong has been doing an excellent job promoting and selling......don' t want to steal his thunder....

btw, I also asked you to look out for Sembcorp' s unusual movements, and as it happened, it is actually crying out to you, it could reach eight as early as this month (impossible, right?), if not, by latest next month.... don' t ask me why, I also don' t know why...... but you know the mafia .... they don' t play games.....

btw, I also asked you to look out for Sembcorp' s unusual movements, and as it happened, it is actually crying out to you, it could reach eight as early as this month (impossible, right?), if not, by latest next month.... don' t ask me why, I also don' t know why...... but you know the mafia .... they don' t play games.....

aragosta ( Date: 20-Mar-2026 16:03) Posted:

|