12:04 AM EDT, 03/19/2026 (MT Newswires) -- Yangzijiang Maritime Development (SGX:8YZ) re-designated its chief investment officer, Sun Jianping, as its chief financial officer, effective March 20, according to a Wednesday filing with the Singapore Exchange.

Shares of the maritime financial services company were down nearly 2% in Thursday trading.

This comes after the resignation of the company's financial controller on March 18, the filing said.

Shares of the maritime financial services company were down nearly 2% in Thursday trading.

This comes after the resignation of the company's financial controller on March 18, the filing said.

Yes. Be patient with this stock..My friend believed it should do well and had collected few hundred lots...I collected some and trade it as well...

pasttime ( Date: 18-Mar-2026 21:27) Posted:

|

good that the share price is moving with the market. got up got down then got market.

2%+ in 1 day is good. more important is they can hold 56-60 side ways and slowly up 1by1cents over weeks. believe it will move up with each ships sale. not like yzj where ship contract excite people.

this no yard ship builders has to close with a sale then the profit is in the hand.

buy aready sit steady. 3 years time got good chance to be bagger. dyodd

2%+ in 1 day is good. more important is they can hold 56-60 side ways and slowly up 1by1cents over weeks. believe it will move up with each ships sale. not like yzj where ship contract excite people.

this no yard ship builders has to close with a sale then the profit is in the hand.

buy aready sit steady. 3 years time got good chance to be bagger. dyodd

others moved 5 steps ahead, this shit only moved 1 step.

Maybe SBB by end of this week

5% + 5% or one shot @ 10% of SBB

5% + 5% or one shot @ 10% of SBB

Perhaps living up to his name " REN" - 忍 耐

Winnertakeall ( Date: 18-Mar-2026 14:24) Posted:

|

Ren already mentioned 90c. What is he waiting for SBB ???

Winnertakeall ( Date: 17-Mar-2026 17:54) Posted:

|

🟢 What' s positive about YZJ Maritime

- Exposure to shipping upcycle

It deploys capital into vessels and maritime assets, so it benefits if charter rates and asset values rise. - Higher-return strategy vs traditional finance arm

Post spin-off, it meant to generate stronger ROE by actively investing in maritime assets - Growing income sources

Recent results showed +13% income growth, helped by maritime fund assets

SBB soon

War in Iran ' not a bad thing' for Yangzijiang Maritime

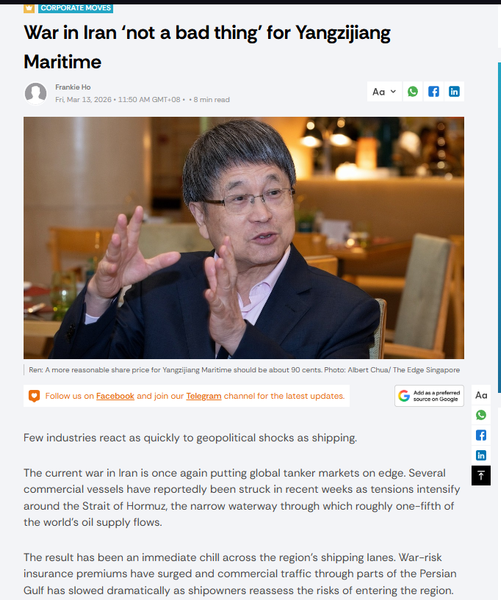

Ren: A more reasonable share price for Yangzijiang Maritime should be about 90 cents.

The Edge Singapore

25 cents....Referring to YZJ Finance?

rayokc ( Date: 16-Mar-2026 22:16) Posted:

|

heading 25 cents....

May drop further tomorrow. Below 0.56

Sgvale ( Date: 16-Mar-2026 16:46) Posted:

|

Close 0.56 i think

Where the much touted share buyback? NATO or TACO?

The recent surge in global trade connectivity (as highlighted in the 2026 DHL report) and a focus on " Cash Management" segments provide a defensive buffer. The company remains a key player in ship financing and maritime asset management during this period of high global trade volume.

https://www.dhl.com/global-en/microsites/core/global-connectedness/report.html?cid=paid-display_RPaMeU& gad_source=1& gad_campaignid=22349276619& gbraid=0AAAAA_AKl18zev-6GZ6JDo6GZqDq-iaiX& gclid=Cj0KCQjwsdnNBhC4ARIsAA_3hej-TBbAuqBdgFqEcAAcdb8KVtJg2bLCkSHkgfMXKZiLvTZM1HIAnZsaAr37EALw_wcB

The value not seen is the industry contact and knowledge. Also using shipyards idle capacity is nog only profitable. It create jobs. This is good things and good things goes around and comes around

War in Iran &lsquo not a bad thing&rsquo for Yangzijiang Maritime

Few industries react as quickly to geopolitical shocks as shipping.

The current war in Iran is once again putting global tanker markets on edge. Several commercial vessels have reportedly been struck in recent weeks as tensions intensify around the Strait of Hormuz, the narrow waterway through which roughly one-fifth of the world&rsquo s oil supply flows.

The result has been an immediate chill across the region&rsquo s shipping lanes. War-risk insurance premiums have surged and commercial traffic through parts of the Persian Gulf has slowed dramatically as shipowners reassess the risks of entering the region.

For oil tankers, though, geopolitical crises can produce a counterintuitive outcome: higher profits.

When oil cargoes are forced to travel longer distances or when ships avoid certain routes altogether, the effective supply of vessels shrinks. This can quickly push up freight rates, not to mention oil prices.

History offers several precedents. The so-called Tanker War in the 1980s saw Iran and Iraq attack hundreds of oil tankers and commercial vessels in the Gulf in a bid to cripple each other&rsquo s economies. Tanker freight rates jumped as shipowners demanded risk premiums and fewer vessels were willing to enter the conflict zone.

Russia&rsquo s 2022 invasion of Ukraine similarly upended global oil shipping, as Western sanctions forced Moscow to turn to ageing, uninsured tankers to keep its crude flowing to willing buyers.

For Chinese billionaire Ren Yuanlin, the current situation in the Middle East represents a rare moment when geopolitical risk and market opportunity converge.

&ldquo The war in Iran is not entirely a bad thing for the shipping market. It&rsquo s not a bad thing for us,&rdquo Ren, Yangzijiang Maritime Development&rsquo s executive chairman and CEO, tells The Edge Singapore.

&ldquo Demand for oil tankers has gone up, as seen from the jump in freight rates, and shares of listed tanker operators are soaring,&rdquo he says. &ldquo I think it&rsquo s an opportunity for us to take some risks.&rdquo

Yangzijiang Maritime, an asset manager that deploys capital into vessels, maritime financing, and related industry services, announced a few months ago plans to build four medium-range tankers in China through a joint venture with a European shipowner.

Slated for delivery over the next two years, these tankers could fetch higher prices if the war in Iran becomes protracted, says Ren.

The company, which was spun off from Yangzijiang Financial Holding in November last year, also recently said it would sell four medium-range tankers currently under construction to a Marshall Islands-based shipowner for a total of US$180 million ($230 million).

In addition to oil tankers, Yangzijiang Maritime also owns gas carriers, containerships, offshore support vessels, and bulk carriers, all of which are available for charter or sale. But unlike other listed tanker owners or operators, it has barely roused investors&rsquo interest since the first wave of the joint attack on Iran by the US and Israel.

That partly reflects the company&rsquo s diversified fleet and business model. Investors tend to view the group less as a pure tanker play and more as a maritime investment platform spanning multiple segments of the shipping industry.

To be sure, Yangzijiang Maritime is only in the early stages of building out that platform. According to its strategic roadmap, the company will roll out a fuller suite of services over the next three to five years. These will range from vessel investment and financing to leasing, retrofitting and brokerage. The strategy reflects its ambition to become a hub connecting shipyards, shipowners, charterers, and capital markets.

A sense of dé jà vu

&ldquo I can say frankly that our share price is undervalued,&rdquo says Ren. &ldquo The current price is just like Yangzijiang Shipbuilding&rsquo s share price years ago.&rdquo

When Yangzijiang Shipbuilding listed on the Singapore Exchange in 2007, its shares traded for years without much excitement. Investors were uneasy about its dual exposure to shipbuilding and financial investments, particularly its lending activities in China, where there were concerns it could end up saddled with massive bad loans.

It was only after the shipbuilder spun off its investment arm, Yangzijiang Financial, in 2022 that investors began to view its business more clearly.

&ldquo A more reasonable price for Yangzijiang Maritime should be about 90 Singapore cents,&rdquo Ren figures.

The way he sees it, Yangzijiang Maritime&rsquo s profitability should strengthen as vessels ordered in recent years are delivered, creating scope to sell or charter out the ships and, in turn, drive the share price higher. The stock is currently trading near parity to the company&rsquo s latest reported net asset value of 46.57 US cents per share or 60 cents.

Strategy and financial firepower

The company&rsquo s competitive edge lies in keeping its costs as much as 20% below market levels without compromising quality, says Ren. It typically forms joint ventures with European shipowners, usually taking the controlling stake, and taps a network of small- and medium-sized shipyards in Jiangsu to build vessels, while supervising construction using experienced contractors.

A number of these shipyards are underutilised. This gives Yangzijiang Maritime leverage in price negotiations, allowing it to secure discounts on building costs while providing the yards with much-needed order flow.

The company has been actively reshaping its fleet portfolio, which now comprises more than 80 completed and yet-to-be-built vessels, in anticipation of opportunities across shipping cycles.

Fleet optimisation reflects its disciplined approach to capital allocation: acquiring or building vessels when asset prices and charter opportunities align, then selling or chartering them out as market conditions improve.

Given the current situation in the Strait of Hormuz, medium-range product tankers &mdash widely used in the refined petroleum trade &mdash are a natural fit for the company. If Middle Eastern oil flows are further disrupted, this segment could benefit as cargoes are rerouted across longer distances, potentially lifting demand for tankers.

The company is also positioning itself to ride the shipping industry&rsquo s shift toward cleaner vessels. Much of the global fleet still runs on conventional fuel, but tighter environmental rules are accelerating demand for ships powered by cleaner fuels and more efficient propulsion systems.

This combination of shipbuilding access in China and financing capability enables Yangzijiang Maritime to participate in both the construction and ownership of these next-generation vessels.

With about US$500 million in cash and no debt, the company has ample financial firepower to fund vessel acquisitions or new building projects without relying on external financing. It has an internal rate of return target of 10% to 15% on investments made without leverage. This could double to between 20% and 30% if it takes on debt to amplify investment returns.

Alongside its expansion strategy, Yangzijiang Maritime has also signalled its willingness to return capital to investors. Earlier this month, shareholders approved a mandate for the company to buy back up to 10% of its issued shares. The initiative is part of a broader capital management strategy that allows it to deploy excess cash when its share price falls below its intrinsic value.

The company also intends to return a meaningful portion of its earnings to shareholders. While it is cash-rich, dividends should be based only on profitability rather than its balance sheet reserves, which are intended primarily for operations and future investments, says Ren. &ldquo Some people have asked whether we can give dividends from our cash reserves. We can&rsquo t.&rdquo

Between 40% and 50% of its annual profits will eventually be distributed as dividends, according to Ren. For 2025, the company has proposed a final dividend of 0.5 cent a share. Based on its 2025 earnings per share of 3.73 US cents, that translates into a payout ratio of just over 10%.

Tariffs and turbulence

Beyond capital management and the war in Iran, Ren is also watching broader forces shaping global trade. Chief among them is how the US tariff regime will evolve following the US Supreme Court&rsquo s recent ruling that President Donald Trump&rsquo s sweeping import duties were illegal.

For now, Ren believes the immediate impact on China&rsquo s exports &mdash and, by extension, on shipping demand &mdash may be limited. Existing US tariffs on Chinese goods are already higher than Trump&rsquo s newly proposed tariff rate of up to 15%, he notes. &ldquo In that context, the new tariff rate is not that big a threat to China.&rdquo

Any further upward revision to US tariffs on Chinese goods will most likely not be well received by American consumers, who could take their dissatisfaction to the ballot box in the US midterm elections due in November, he lets on.

&ldquo China&rsquo s goods will end up very expensive in the US. American consumers will object to this. Having said that, the tariffs have no direct impact on Yangzijiang Maritime&rsquo s business.&rdquo

The current global operating environment underscores a familiar truth about shipping: periods of uncertainty often create the most compelling investment opportunities. While conflicts, trade disputes and shifting energy routes can disrupt markets overnight, they also reshape global trade flows in ways that reward companies positioned to move quickly.

For Ren, getting Yangzijiang Maritime ready to capitalise on these dislocations is key. He is banking on the company&rsquo s growing fleet pipeline, substantial liquidity, and ready access to Chinese shipyards to do just that. If geopolitical disruptions continue to reshape global trade routes, the company could find itself on the right side of the turbulence.

Current share price: 57c.

Eps : 4.8c.

Pe : 11.9.

Outstanding shares : 3.46b.

Cash : S$680m.

Cash per share : 19c.

Nta : 60c.

No debt.

Good to buy now? Dyodd.

Eps : 4.8c.

Pe : 11.9.

Outstanding shares : 3.46b.

Cash : S$680m.

Cash per share : 19c.

Nta : 60c.

No debt.

Good to buy now? Dyodd.