good if YZJ delist from SGX and list in HKEX...

Huat big big!!!

Huat big big!!!

Yes. SGX pennies wise pound foolish 😜

Panda8 ( Date: 01-Apr-2026 08:39) Posted:

|

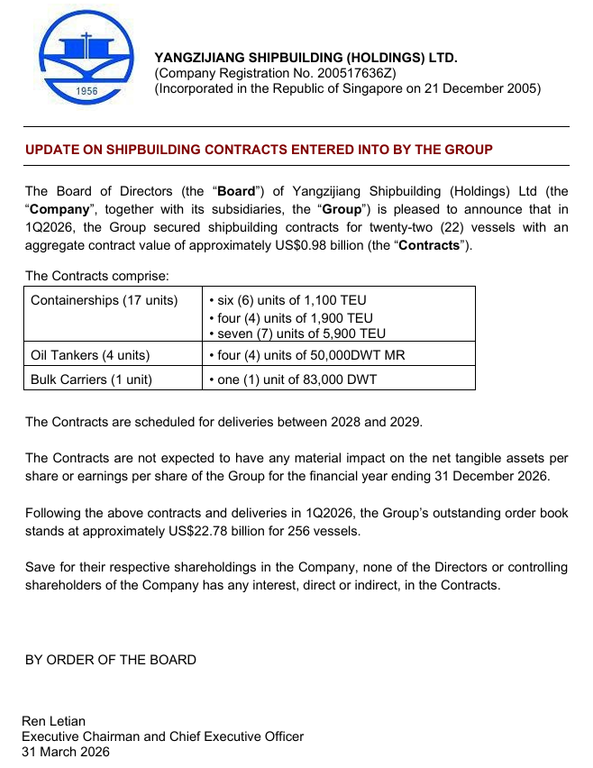

Yangzijiang Shipbuilding bags US$980 million in vessel contracts in Q1

The group&rsquo s outstanding order book stands at about US$22.8 billion

[SINGAPORE] Yangzijiang Shipbuilding said on Tuesday (Mar 31) that it secured shipbuilding contracts for 22 vessels in the first quarter of 2026, with an estimated aggregate value of about US$980 million.

The contracts are for 17 container ships, four oil tankers and one bulk carrier. These are scheduled for deliveries between 2028 and 2029.

The mainboard-listed shipbuilder does not expect the contracts to have any material impact on its net tangible assets per share or earnings per share for the financial year ending Dec 31, 2026.

The group said its outstanding order book stands at about US$22.8 billion for 256 vessels, after factoring in the latest quarter&rsquo s contracts and deliveries.

Shares of Yangzijiang Shipbuilding : BS6 -0.79% closed at S$3.78, down 0.8 per cent or S$0.03, on Tuesday, before the announcement.

It is time for SGX to wake up and do something about it before too late. Once they leave, will be no return. And SGX market will be getting smaller and smaller.

cltang ( Date: 31-Mar-2026 22:21) Posted:

|

Yangzijiang Considers Delisting From SGX .....31 March 2026

https://mp.weixin.qq.com/s/hs_9d530FZQlEtKqV-SuUA

https://mp.weixin.qq.com/s/hs_9d530FZQlEtKqV-SuUA

cltang ( Date: 31-Mar-2026 22:21) Posted:

|

https://mp.weixin.qq.com/s/hs_9d530FZQlEtKqV-SuUA

他 进 一 步 给 出 了 一 个 极 具 震 撼 力 的 对 比 :若 核 心 资 产 扬 子 江 船 业 转 赴 香 港 上 市 , 其 目 前 约 4新 元 的 股 价 水 平 , 在 两 地 市 场 估 值 逻 辑 的 差 异 下 , 理 论 上 有 望 获 得 接 近 10新 元 的 估 值 重 塑 。 这 种 显 著 的 &ldquo 估 值 分 化 &rdquo , 正 是 驱 使 扬 子 江 系 重 新 审 视 资 本 主 战 场 的 关 键 诱 因 。

" He further provided a striking comparison: if core asset Yangzijiang Shipbuilding were to shift its listing to Hong Kong, its current share price of approximately SGD 4 could theoretically undergo a valuation re-rating to nearly SGD 10, driven by the divergent valuation logics of the two markets. This significant " valuation divergence" is precisely the key driver compelling the Yangzijiang group to re-evaluate its primary capital battleground."

他 进 一 步 给 出 了 一 个 极 具 震 撼 力 的 对 比 :若 核 心 资 产 扬 子 江 船 业 转 赴 香 港 上 市 , 其 目 前 约 4新 元 的 股 价 水 平 , 在 两 地 市 场 估 值 逻 辑 的 差 异 下 , 理 论 上 有 望 获 得 接 近 10新 元 的 估 值 重 塑 。 这 种 显 著 的 &ldquo 估 值 分 化 &rdquo , 正 是 驱 使 扬 子 江 系 重 新 审 视 资 本 主 战 场 的 关 键 诱 因 。

" He further provided a striking comparison: if core asset Yangzijiang Shipbuilding were to shift its listing to Hong Kong, its current share price of approximately SGD 4 could theoretically undergo a valuation re-rating to nearly SGD 10, driven by the divergent valuation logics of the two markets. This significant " valuation divergence" is precisely the key driver compelling the Yangzijiang group to re-evaluate its primary capital battleground."

Published 31 March 2026, 18:19

Alpha Omega Marine, a Singapore-based shipping investment platform managed by two Greek partners, confirmed on Tuesday that it has inked its first bulker newbuildings.

TradeWinds already reported in November about market sources naming Alpha Omega as a partner in a quartet of 40,000-dwt handysizes that Yangzijiang Maritime Development (YZJ Maritime) announced ordering at an undisclosed shipyard.

Panda8 ( Date: 31-Mar-2026 18:14) Posted:

|

Thanks for the update

JurongW ( Date: 31-Mar-2026 17:37) Posted:

|

Cool, just ignore the noises.

Winnertakeall ( Date: 30-Mar-2026 11:48) Posted:

|

SITC orders feeder container ships

worth $137m at Yangzijiang Shipbuilding

The six 1,100-teu newbuildings were option vessels that the company held at shipyard

Intra-Asia liner specialist SITC International Holding has lifted its growing orderbook with six 1,100-teu container ship newbuildings.

The Hong Kong-listed company said it has contracted Yangzijiang to build the series of feeder vessels to be delivered between March and August 2028.

pkli899 ( Date: 27-Mar-2026 16:13) Posted:

|

Yangzijiang Shipbuilding (2026) Analysis:

Earnings Outlook, Margins, and Investment Risks Explained

Posted on March 27, 2026

Excerpt from Maybank Research Pte Ltd report.

- Maybank initiates coverage on Yangzijiang Shipbuilding with a HOLD rating and a DCF-based target price of SGD 4.15, citing that the shipbuilding cycle and margins are past peak levels.

- Yangzijiang is supported by a strong balance sheet and a robust orderbook (~USD22.4b), ensuring medium-term revenue visibility but with earnings CAGR moderating to 5% for FY25&ndash 28.

- Gross margins have risen sharply (from 14% in FY21 to 34% in FY25), but are expected to normalize to around 29% by FY28 as pricing softens and competition rises.

- Order momentum is slowing, with new shipbuilding orders forecast to decline further in 2026 due to high orderbook levels, softer demand, and FX headwinds from a stronger RMB.

- While the dividend yield is attractive (5&ndash 6%) and supported by a 50% payout, further upside is limited due to capital needs for investments and capex.

- Risks include faster margin normalization, weaker demand, and FX fluctuations upside risks are stable steel prices, stronger execution, and order reallocation from weaker yards.

- Maybank prefers Seatrium and Marco Polo Marine for better upside due to their offshore order exposure and margin recovery potential.

Is exercise option la.....USD137m.

YZJ NEW ORDER WON AS AT 27/3 6X1,100TEU WORTH US$130M FROM SITC

$YZJ Shipbldg SGD (BS6.SG)$

3月 27日 , 海 丰 国 际 控 股 有 限 公 司 ( 以 下 简 称 ?海 丰 国 际 ?) 发 布 《 须 予 披 露 交 易 建 造 集 装 箱 船 舶 》 的 公 告 , 其 全 资 附 属 公 司 海 丰 船 东 有 限 公 司 将 行 使 与 造 船 商 所 订 立 造 船 期 权 合 约 项 下 建 造 另 外 六 艘 船 舶 的 期 权 , 总 代 价 为 1.37亿 美 元 ( 约 合 人 民 币 9.5亿 元 ) 。

Let's see if it can close gap at 3.98.....

finally break 4.03. Now 4.09.... heading to 4.15 very soon. Maybe today.........

403 done...nice...more upside...

kt3152 ( Date: 17-Mar-2026 09:25) Posted:

|

💰 1. Strong profitability and margins

📦 2. Huge orderbook = strong future earnings visibility

🚢 4. Benefiting from industry tailwinds

🌱 5. Exposure to green shipping trend

🌍 6. Strong global customer base

📈 7. Attractive valuation (historically)

⚙ ️ 8. Operational track record

- YZJ consistently delivers high profit margins (30%+ gross margin in some periods).

- Net profit has been growing strongly (e.g. +30% YoY in FY2025).

- Efficient cost control (like lower steel costs + better pricing) boosts margins further.

📦 2. Huge orderbook = strong future earnings visibility

- Orderbook of ~US$20B+ extending to 2028 - 2029.

- New orders keep coming in, including record wins in recent years.

- 👉 This is a big deal: shipbuilders live or die by backlog, and YZJ is very solid.

- Holds massive net cash (billions of RMB) and low gearing.

- Financial strength allows:

- Expansion

- Dividend payments

- Downside protection in downturns

🚢 4. Benefiting from industry tailwinds

- Global demand for ships is rising due to:

- Fleet replacement

- High freight rates

- Supply constraints

- Orders for new ships grew significantly into 2026.

🌱 5. Exposure to green shipping trend

- Large portion of orders are eco-friendly / dual-fuel vessels (~70%+).

- Investing in energy-efficient ship designs and ESG initiatives.

🌍 6. Strong global customer base

- Serves major international shipping companies (e.g. large container operators).

- Diversified across regions (Asia, Europe, North America).

📈 7. Attractive valuation (historically)

- Trades at relatively low P/E vs growth and ROE (~20 - 25% ROE).

- Often seen as undervalued vs peers in Korea/Japan.

⚙ ️ 8. Operational track record

- Consistently delivers ships on time and at scale (dozens per year).

- Known for efficient execution and cost control.

- 👉 Reliability matters a lot in shipbuilding and YZJ has it.

been waiting so long for it to chiong.... hopefully can see 4.15 today