No DBS in your retirement portfolio?

newbie19 ( Date: 10-May-2026 10:51) Posted:

|

Good point. As i m growing older and retiring soon.

I only keep Keppel and Seatrium for the dividends.

I m very peaceful now not like last time 30+ years ago i already started playing shares.

Until about 6 or 7 years ago i started to sell off slowly all my shares.

Mostly penny stocks and a few blue chips.

I was quite active playing shares especially penny stocks,

and at times you have sleepless nights.

And so no more active in buying shares already..

Newbie2025 ( Date: 10-May-2026 07:39) Posted:

|

Sir why dont you keep it since it's free and just it grow..😂

newbie19 ( Date: 08-May-2026 19:34) Posted:

|

Consider one of them among all...

I also sold all my free Keppel Reits share today at $0.885.

JurongW ( Date: 08-May-2026 19:02) Posted:

|

U collect the most money

newbie19 ( Date: 08-May-2026 19:00) Posted:

|

Today everyone here should be collected the dividend money credited to your bank this evening around

5pm.

Cheers 👍 🏻 😁 😁

JurongW ( Date: 08-May-2026 18:35) Posted:

|

SBB today - 500,000 shares bought at 10.87 to 10.98 ($5,465,816)

COMPLETION AND PAYMENT OF SPECIAL DIVIDEND

https://links.sgx.com/1.0.0/corporate-announcements/04O9KR65EHX19QA2/888106_Keppel%20-%20Completion%20and%20payment%20of%20Special%20Dividend_8%20May%202026.pdf

SBB today - 200,000 shares bought at 11.04 to 11.17 ($2,220, 647)

Personally

I feel

Keppel should follow DBS

give quarterly dividends

Feb( 0.02+0.04 ) gain May(0.19 -0.04) August(0.15) November (0.09 stock in species recently )

Then when Feb grow due to new Keppel or when November due to moneitization

very clear

mean eventually if we are getting 0.15 x 4 by 2028 2029 it send a very loud and clear to the shareholder

I feel

Keppel should follow DBS

give quarterly dividends

Feb( 0.02+0.04 ) gain May(0.19 -0.04) August(0.15) November (0.09 stock in species recently )

Then when Feb grow due to new Keppel or when November due to moneitization

very clear

mean eventually if we are getting 0.15 x 4 by 2028 2029 it send a very loud and clear to the shareholder

Joelton ( Date: 07-May-2026 13:23) Posted:

|

Are Keppel&rsquo s dividends truly unsustainable &ndash or just misunderstood?

The company&rsquo s shares have rallied over the past year, generating a total shareholder return of 58.5% in 2025

[SINGAPORE] The recent clash between Keppel : BN4 -0.09% and activist research firm Corporate Monitor highlights a vital question for investors: Are the dividends from the restructured Keppel truly sustainable?

The activist report pulled no punches. It argued that Keppel&rsquo s payouts are a mirage, funded by selling off assets rather than by generating operating cash flow.

Pointing to a gap between reported profits and operating cash flow, Corporate Monitor painted a picture of a heavy balance sheet masking underlying weakness.

At Keppel&rsquo s recent annual general meeting, these hard questions &ndash fielded by proxies for Corporate Monitor &ndash also dominated the floor.

To judge the fairness of this critique, we must look at the blueprint of Keppel&rsquo s Vision 2030.

The activist argument judges Keppel by the metrics of a traditional industrial conglomerate. If a legacy builder relies on asset sales to fund its dividends, warning bells should rightly ring.

But Keppel has changed its identity. It has transitioned into a global asset manager and operator. In this new space, asset monetisation is the core operating engine.

Through sponsor stakes in and co-investments with its own private funds or affiliated real estate investment trusts, Keppel develops real assets, stabilises them, and then sells them.

&ldquo As an asset manager and operator, Keppel&rsquo s cash-generation sources include both operating and investing activities,&rdquo a company spokesperson said in response to queries from The Business Times. &ldquo It is incomplete to look at Keppel&rsquo s cash flow just from the perspective of &lsquo cash flow from operations&rsquo .&rdquo

Besides recurring distributions supported by the underlying operating cash flows, the assets owned by its private funds typically see valuation uplift over the development cycle. Value realised on divestment and proceeds distributed back to Keppel contribute to its investment cash inflows.

&ldquo Despite investments and capex of S$5.4 billion from 2021 to 2025, the company generated free cash inflows cumulatively over the same period of approximately S$1.7 billion,&rdquo the spokesperson said.

The way Keppel sees it, to look only at cash flow from operations is hence &ldquo inadequate and misleading&rdquo .

Similar pivot, different paths

We can see the mechanics of this strategy clearly by looking at another local giant that successfully made a similar pivot: CapitaLand : 9CI +0.38%. Both companies made a big change to become global asset managers.

CapitaLand paved the way in 2021 when it listed its investment arm. It uses its balance sheet to start real estate projects and then sells them to its private funds or trusts to earn fees. Keppel is building the same engine, but it focuses on energy, green tech and digital assets.

The main difference is in how they deal with their older, heavy assets.

CapitaLand made a clean split. It took its heavy development business private and listed only the asset management side. Keppel took a different path it kept its older assets on its books.

Keppel created a set-up where its new business drives regular income, while it slowly sells off the older, non-core assets. This makes Keppel&rsquo s balance sheet look heavier, as if it carries more debt than CapitaLand&rsquo s right now. This relatively heavier debt is the main reason for the complaints from Corporate Monitor.

Critics rightly point out that the group still carries a heavy legacy burden. Keppel has S$13.5 billion tied up in non-core assets. The overall ratio of group net debt to earnings before interest, taxes, depreciation and amortisation remains high.

However, Keppel&rsquo s leadership has clarified that the debt profile of New Keppel is far healthier. The heavier debt load sits squarely with the legacy assets, which the company is actively working to clear by 2030.

The company&rsquo s dividend policy directly reflects this dual approach. To provide clarity to the market, management has drawn a clear line between its core operations and its legacy portfolio.

The ordinary dividend is funded by the performance of &ldquo New Keppel&rdquo , which is underpinned by recurring income.

In 2025, a robust 86 per cent of New Keppel&rsquo s net profit was recurring. This gives the ordinary payout a strong, reliable foundation, much like the fee-based income that anchors CapitaLand Investment.

For FY2025, Keppel proposed an ordinary dividend of S$0.34 per share, comprising a final dividend of S$0.19 per share and an interim dividend of S$0.15 per share.

The special dividend is handled differently. Keppel has a set policy to pay out 10 to 15 per cent of the gross value of asset monetisation transactions completed in the financial year.

For 2025, the company announced approximately S$2.9 billion in divestments and completed S$1.6 billion in transactions to unlock capital, reduce debt and fund growth. This drove a proposed special dividend of roughly S$0.13 per share.

This explicit link between asset sales and special payouts removes the guesswork for investors. It provides a transparent framework for the duration of the monetisation programme.

In the year to date, Keppel has announced S$385 million in asset monetisation, with a target to monetise S$2 billion to S$3 billion of non-core assets in 2026.

Transformation in progress

Understandably, transforming a massive legacy balance sheet takes time. But the first quarter of 2026 provided encouraging signs that the transition is gaining traction.

Keppel reported that it had returned to a free cash inflow position &ndash recording cash inflows from both operating and investing activities, compared to outflows in the corresponding quarter the year before.

Asset management fees rose 13 per cent year on year to S$108 million in Q1 2026, even as overall net profit was lower on fair value losses and lower monetisation gains from the non-core portfolio.

The company is closing in on its target of S$100 billion in funds under management ahead of its 2026 deadline. Looking further ahead, the group aims to double that figure to S$200 billion by the end of the decade.

The market has largely validated this strategic pivot.

Keppel&rsquo s shares have rallied strongly over the past year. Investors were rewarded with a total shareholder return &ndash with dividends reinvested &ndash of 58.5 per cent in 2025.

Sell-side analysts remain overwhelmingly positive on the stock. They view the regular asset sales as clear catalysts for unlocking value.

Asset recycling inherently produces lumpy cash flows. There will be quarters where divestment gains skew the numbers. There will be periods of heavy capital expenditure as new seed assets are developed.

The upcoming Keppel Sakra Cogen Plant, for instance, requires significant upfront investment. But it will eventually provide contracted, recurring revenue before potentially being offered to investors.

The activist critique performs a useful function. It demands accountability and rigorous accounting. The questions regarding the carrying value of legacy assets and the pace of the wind-down are entirely valid.

Management will need to maintain strict discipline to ensure that the non-core portfolio is monetised at fair valuations. But to conclude that Keppel&rsquo s dividends are unsustainable is to ignore the stated mechanics of its business model.

The company has laid out a clear road map. The recurring income from its asset management and operating platforms secures the base dividend, while the managed unwinding of its legacy assets funds the special payouts.

This is a multi-year transformation taking place in full view of the market.

The transition from heavy industry to asset management is inherently messy in its middle phases. But the underlying financial engine is working as designed.

For investors willing to accept the asset-light premise proven by peers, Keppel&rsquo s current payout structure offers a credible bridge to the future.

BB is in the range of 200k to 500k shares.

Newbie2025 ( Date: 06-May-2026 21:34) Posted:

|

Thank you Sir 🫡

Is this buying aggressive?

JurongW ( Date: 06-May-2026 18:38) Posted:

|

SBB today - 200,000 shares bought at 10.94 to 10.99 ($2,197,442)

SBB today - 200,000 shares bought at 10.78 to 11.00 ($2,179,979)

The money is in the waiting.

MrBear12 ( Date: 04-May-2026 23:24) Posted:

|

PROPOSED DIVESTMENT OF 39% INTEREST IN KEPPEL MERLIMAU COGEN PLANT

Keppel Ltd. ("Keppel" or the "Company", and together with its subsidiaries, the "Group") wishes to announce that KCIF Investments Pte. Ltd. ("KCIF Investments") has entered into a sale and purchase agreement ("SPA") with Keppel Infrastructure Fund Management Pte. Ltd. (as trustee- manager of Keppel Infrastructure Trust) ("KIT") to divest, in the manner described below, KCIF Investments' entire 39% interest in Keppel Merlimau Cogen Pte. Ltd. ("KMC") to KIT (the "Proposed Divestment").

KCIF Investments is a wholly-owned subsidiary of Keppel Core Infra Fund GP Pte. Ltd. (as general partner of Keppel Core Infrastructure Fund, LP) ("KCIF"), and KCIF is in turn a subsidiary of Keppel. KMC holds the Keppel Merlimau Cogen Plant, a combined cycle gas turbine generation facility with a licensed generation capacity of approximately 1,300 MW and ancillary facilities on Jurong Island off the south-west coast of Singapore.

The current shareholders of KMC are KIT (51%), Kindle Energy Pte. Ltd. (a wh subsidiary of KCIF Investments) ("Kindle Energy") (39%), and Keppel Energy Pte. Ltd. ("Keppel Energy") (a wholly-owned subsidiary of Keppel) (10%). Following completion of the Proposed Divestment ("Completion"), KIT's aggregate interest in KMC will be 90%, with the remaining 10% of the interest continued to be held by Keppel, through Keppel Energy.

Keppel Ltd. ("Keppel" or the "Company", and together with its subsidiaries, the "Group") wishes to announce that KCIF Investments Pte. Ltd. ("KCIF Investments") has entered into a sale and purchase agreement ("SPA") with Keppel Infrastructure Fund Management Pte. Ltd. (as trustee- manager of Keppel Infrastructure Trust) ("KIT") to divest, in the manner described below, KCIF Investments' entire 39% interest in Keppel Merlimau Cogen Pte. Ltd. ("KMC") to KIT (the "Proposed Divestment").

KCIF Investments is a wholly-owned subsidiary of Keppel Core Infra Fund GP Pte. Ltd. (as general partner of Keppel Core Infrastructure Fund, LP) ("KCIF"), and KCIF is in turn a subsidiary of Keppel. KMC holds the Keppel Merlimau Cogen Plant, a combined cycle gas turbine generation facility with a licensed generation capacity of approximately 1,300 MW and ancillary facilities on Jurong Island off the south-west coast of Singapore.

The current shareholders of KMC are KIT (51%), Kindle Energy Pte. Ltd. (a wh subsidiary of KCIF Investments) ("Kindle Energy") (39%), and Keppel Energy Pte. Ltd. ("Keppel Energy") (a wholly-owned subsidiary of Keppel) (10%). Following completion of the Proposed Divestment ("Completion"), KIT's aggregate interest in KMC will be 90%, with the remaining 10% of the interest continued to be held by Keppel, through Keppel Energy.

With the monetisation

I think they have sufficient cash in future to announce another 500 million sharebuyback too

Personally I think the easier way to attract AUM is to become a bigger market capitalisation company too

I think they have sufficient cash in future to announce another 500 million sharebuyback too

Personally I think the easier way to attract AUM is to become a bigger market capitalisation company too

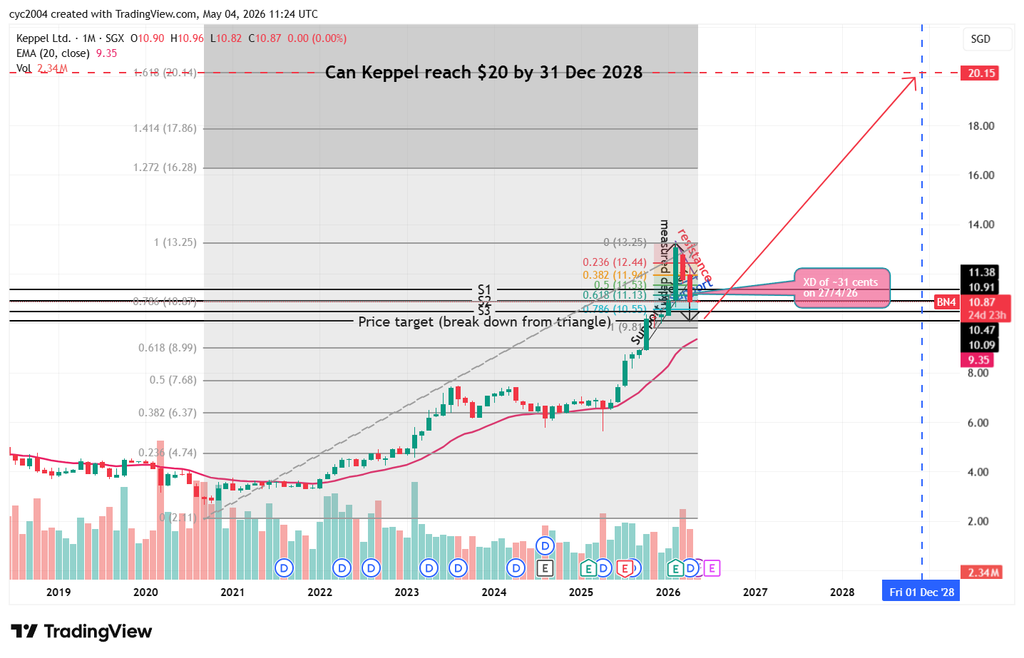

spore1 ( Date: 04-May-2026 23:15) Posted:

|

definitely. vision 2028 in progress.

Let Keppel double in less than three years. ...

We are well on our way. having touched 13 earlier this year.

2025 was a great year, 2026 is even better, then 2027 will be the year when Keppel becomes totally renewed before the year of celebrations 2028.

Keep faith with Keppel.

JurongW ( Date: 04-May-2026 19:27) Posted:

|

Let's see how it turns out!

JurongW ( Date: 04-May-2026 19:13) Posted:

|