| Latest Forum Topics / Grand Venture |

|

|

EXPANSION INTO THE MEDICAL INDUSTRY FOR GROWTH

|

|||||||||||

|

Joelton

Supreme |

13-Jan-2025 11:00

|

||||||||||

|

x 0

x 0 Alert Admin |

GVT Partners with A*STAR to Develop Advanced Ceramics Manufacturing Platform

Strategic partnership with A*STAR showcases GVT&rsquo s commitment to technological excellence and innovation

Collaboration will unlock opportunities to expand wallet share within GVT&rsquo s existing customer base through technological advancements

Mainboard-listed Grand Venture Technology Limited (杰 纬 特 科 技 有 限 公 司 , &ldquo GVT&rdquo , or the &ldquo Group&rdquo ), a homegrown precision manufacturing solutions provider, is pleased to announce that it is collaborating with the Agency for Science, Technology and Research (A*STAR) to develop a customised manufacturing platform for high-value advanced ceramics.

This strategic partnership underscores GVT' s commitment to innovation and technology-driven growth, which are vital in addressing the evolving demands of its customers in the life sciences and semiconductor sectors. To co-drive this partnership with GVT, A*STAR Singapore Institute of Manufacturing Technology (A*STAR SIMTech) is leading the development of the platform. Through this partnership, GVT aims to capture opportunities in high-growth industries and strengthen its competitive edge.

This will enable GVT to address increasing demand from both existing and new customers, aligning with its broader strategy to deliver value through technological excellence and operational agility. More details will be shared at a later date. Growth and Innovation GVT&rsquo s partnership with A*STAR aligns with its broader strategy to deliver exceptional value through technological excellence.

The collaboration will enable GVT to:

Meaningful development for our advanced materials R& D roadmap

Expand its differentiated capabilities in high-value ceramics manufacturing to meet growing demand from existing and new customers

Strengthen competitive edge and customer centricity by integrating innovative technologies into its manufacturing processes.

&ldquo This partnership with A*STAR is a key milestone in GVT&rsquo s journey to acquiring higher wallet share within our existing customer base by focusing on expanding technological capabilities,&rdquo said Julian Ng, Chief Executive Officer of GVT. &ldquo By co-developing this customised platform, we are not only enhancing our technological capabilities but also reinforcing our commitment to delivering highquality, innovative solutions to our customers. Thereafter, we hope to unlock greater wallet shares with our customers and potentially develop into new stream of consumable business&rdquo

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Sgvale

Supreme |

13-Jan-2025 09:04

|

||||||||||

|

x 0

x 0 Alert Admin |

Coming up.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

|

|||||||||||

|

SmallSmall

Supreme |

13-Jan-2025 05:47

|

||||||||||

|

x 0

x 0 Alert Admin |

NEWS RELEASE GRAND VENTURE TECHNOLOGY PARTNERS WITH A*STAR TO DEVELOP CUSTOMISED MANUFACTURING PLATFORM FOR ADVANCED CERAMICS Strategic partnership with A*STAR showcases GVT&rsquo s commitment to technological excellence and innovation Collaboration will unlock opportunities to expand wallet share within GVT&rsquo s existing customer base through technological advancements |

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

07-Jan-2025 09:50

|

||||||||||

|

x 0

x 0 Alert Admin |

DBS keeps &lsquo buy&rsquo on GVT, raises TP to $1.04 from 70 cents on stronger front-end opportunities

Amanda Tan and Ling Lee Keng of DBS Group Research have raised their target price for Grand Venture Technology (GVT) from 70 cents to $1.04 as they see the manufacturer with a heavy exposure to the semiconductor space riding on a strong and growing blue-chip customer base. The analysts have also retained their &ldquo buy&rdquo call on the counter.

&ldquo Over the past five years, GVT has delivered strong revenue and earnings growth with compound annual growth rates (CAGRs) of 29% and 16%, respectively. GVT also serves a blue-chip customer base &ndash in the semiconductor back-end space, it serves four of the top six in the analytical life sciences segment, it serves three of the top 10,&rdquo write Tan and Ling in their Jan 6 note.

They observe that GVT&rsquo s customers tend to be stickier, as its products supplied are made to specific specifications.

Within the semiconductor segment, GVT&rsquo s exposure to the back-end is about 90% to 95%, implying a 5% to 10% exposure to the front-end. They add that notwithstanding near-term volatility, the semiconductor industry is well poised for growth, owing to the push towards digitalisation.

&ldquo McKinsey projects that the semiconductor industry will become a trillion-dollar market by 2030. The long-term semiconductor outlook looks bright, which should benefit GVT, as more than half of its revenue comes from the semiconductor segment.&rdquo

While contributions from new front-end customers in FY2024 are expected to remain small, the analysts see meaningful growth in FY2025, with FY2026 contributions expected to be more significant.

Furthermore, the group was also recently selected to supply parts and components for so-called next-generation thermal compression bonding (TCB) equipment to a leading global semiconductor assembly and packaging equipment manufacturer.

Tan and Ling, noting that GVT&rsquo s share price has surged some 47% since December, except a near-term consolidation. &ldquo However, we remain positive over the long term with valuations at 14.6 times FY2026 earnings, below one standard deviation (s.d.) of the historical mean.&rdquo

Their new target price of $1.04 is based on a price-to-equity ratio (P/E) of 21 times FY2026 earnings, to account for more meaningful volume production for new front-end customers. While there have been no changes to their FY2024 estimates, Tan and Ling have revised their FY2025 topline by 4.6% to account for a higher wallet share of existing backend customers while initiating their FY2026 estimates.

&ldquo Despite the top-line raise, we retain our FY2025 earnings estimates, given our lower margin assumptions, attributable to continued investment in capabilities and dual-listing expenses.&rdquo

The analysts conclude: &ldquo We are of the view that significant opportunities lie ahead as GVT&rsquo s foray into the front-end opens up a long runway for growth, particularly in the wafer fab equipment market, which is eight times larger than the backend semiconductor equipment market.&rdquo

Key risks noted by the pair include a delay in GVT&rsquo s front-end expansion, a prolonged chip glut, and macro weaknesses.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

SLLIMJ

Senior |

07-Jan-2025 09:03

|

||||||||||

|

x 0

x 0 Alert Admin |

this one can watch closely open high | ||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

|

|||||||||||

|

Sgvale

Supreme |

06-Jan-2025 15:15

|

||||||||||

|

x 0

x 0 Alert Admin |

My target 0.95 | ||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

SmallSmall

Supreme |

06-Jan-2025 13:43

|

||||||||||

|

x 0

x 0 Alert Admin |

DBS keeps &lsquo buy&rsquo on GVT, raises TP to $1.04 from 70 cents on stronger front-end opportunities |

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

SmallSmall

Supreme |

02-Jan-2025 14:08

|

||||||||||

|

x 0

x 0 Alert Admin |

$0.795 +$0.05....Inching up again.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

|

|||||||||||

|

Joelton

Supreme |

19-Dec-2024 12:26

|

||||||||||

|

x 0

x 0 Alert Admin |

Grand Venture Technology rides semicon recovery by investing &lsquo ahead of the curve'

Over the past year, nearly 50 companies have launched IPOs on Bursa Malaysia. Each new listing adds to the market&rsquo s momentum and encourages investors to pay higher multiples for certain stocks than for similar entities listed on other exchanges.

The Bursa was so attractive that several Singapore-listed companies expressed interest in seeking a listing across the causeway. UMS Integration said so in July, followed by Grand Venture Technology JLB (GVT), which signalled its intention to do the same two months later.

Yet, in an interview with The Edge Singapore, Julian Ng, GVT&rsquo s CEO and executive director, tried to downplay the significance of this possible secondary listing. For him, the move ought to be seen as yet another round of fundraising the company has undertaken in its 12-year history.

One of the key rounds was its Singapore IPO on the Singapore Exchange S68 &rsquo s (SGX) Catalist in January 2019, when GVT raised around $13.2 million by selling shares at 27.5 cents each. Another round came just over two years after the IPO in January 2021, where GVT raised around $30 million from Novo Tellus by selling shares at 33 cents each. The investment firm, headed by Loke Wai San, is best known for its multi-bagger bet on semiconductor tester AEM Holdings AWX .

With Novo Tellus on board, GVT&rsquo s shares saw steady growth. In a subsequent fundraising round in September 2021, the company raised an additional $28.5 million by issuing shares at $1.14 each. Along the way, GVT also upgraded to the SGX&rsquo s mainboard.

However, in-line with the subsequent downturn of the semiconductor industry, GVT&rsquo s shares dropped from a peak of $1.33 back in November 2021 to as low as 44 cents in less than a year. Year-to-date, with signs of recovery more visible, GVT shares have gained nearly a fifth year-to-date to close at 63.5 cents on Dec 16, valuing the company at around $214 million.

With funding already in hand, GVT was able to execute its multi-stage plan to bulk up and gear up. &ldquo With all of the funds we&rsquo ve raised, plus our own internal operational cash flow, we&rsquo ve invested quite heavily ahead of the curve,&rdquo Ng says. If it happens, the proposed secondary listing will go towards its broader M& A game plan to bring on additional new capabilities and capacity.

Increasing competitiveness

Originally focused on back-end semiconductor manufacturing, including wire bonding and chip testing, GVT now also offers front-end services, such as metrology and etching &mdash a market said to be ten times larger than the back-end.

&ldquo When we first started, we were a small player, and it wasn&rsquo t easy to move into the approved vendor list for the front-end space. But I think in 2020 or 2021, when we broke the $100 million mark in revenue, we were ready to undertake them,&rdquo says Ng.

In its 9MFY2024 ended September business update, GVT&rsquo s revenue from its semiconductor segment surged by 50.8% y-o-y to $59.5 million. Ng attributes the positive trend to GVT&rsquo s ability to stay up-to-date with growth areas continuously. &ldquo When we onboard our customers, we will try to understand their product line for various markets, and over the years, we have had quite a variety in terms of our clients&rsquo product range. This year, our growth has been driven by AI-related high-bandwidth memory (HBM) testing, which has led to our increasing competitiveness.&rdquo

GVT&rsquo s total revenue in 9MFY2024 was up 35.8% y-o-y to $111.9 million, and in an indication of growth gaining pace, 3QFY2024 revenue was up 52.8% y-o-y to $43.5 million. With an improved margin, GVT&rsquo s 3QFY2024 earnings were up 51.3% y-o-y to $2 million. GVT also says that earnings would have been higher if not for unfavourable forex and other one-off items.

Despite the strong performance of its semiconductor segment, which accounts for over half of its 9MFY2024 revenue, GVT has long recognised the need to diversify its customer base to better navigate the sector&rsquo s cyclical volatility.

To meet its customers&rsquo diverse needs, GVT has expanded its Penang facility from a single factory in 2013 to seven plants today, covering a total manufacturing floor space of 350,000 sq ft. Ng notes that the facility is vertically integrated, offering precision machining, complex 3D shape manufacturing, and mechatronics assembly all under one roof.

Ng adds that since the $17 million acquisition of surface treatment specialist ACP Metal Finishing (ACP) in March, GVT&rsquo s Penang facilities have acquired additional capabilities to help it capture more revenue.

While surface treatment is applicable to semiconductors by preventing corrosion in specific components, ACP&rsquo s acquisition was made to help grow GVT&rsquo s presence in another of its key pillars: the aerospace industry.

Importantly, ACP is accredited by multiple aviation agencies, including the National Aerospace and Defense Contractors Accreditation Program (NADCAP) and the Federal Aviation Administration (FAA).

GVT entered the aerospace market in 2022 by acquiring J-Dragon, a China-based precision engineering firm, for $12.2 million. This move complemented GVT&rsquo s earlier expansion into the life sciences and medical sectors.

The group&rsquo s output is used in end products ranging from mass spectrometers, microscopes, surgical microscopes and aerospace landing gears. &ldquo We are in the right space with the four verticals we are serving today,&rdquo says Ng.

In the 9MFY2024, GVT&rsquo s revenue from its electronics, aerospace and medical segment climbed 32.8% y-o-y to $36.1 million as it consolidated revenues from the newly onboarded ACP, signalling that the move was already starting to pay off.

&ldquo When we did our acquisition of J-Dragon in 2022, they were mainly a machining services provider to the aerospace industry. But if you want to serve the industry meaningfully, you have to have capabilities beyond this, and ACP adds to that. Today, around 80% of their business is probably geared towards aerospace, original equipment manufacturers, maintenance, repair and overhaul,&rdquo says Ng.

Global trade dynamics

As the new year approaches, an increasingly complex geopolitical landscape looms. The impact of the second round of the Donald Trump administration on US-China relations is still uncertain.

Still, Ng is not overly concerned. He notes that GVT&rsquo s business model is largely insulated from global trade dynamics. &ldquo Our Chinese facilities are still mainly serving the local market, so Chinese for Chinese. Most of our other customers are not Chinese but North American and European MNCs. While they do have facilities in China that serve the Chinese market, they are not actually exporting, so we don&rsquo t see a risk to our Chinese operations unless they are doing export.&rdquo

GVT also ensured that the new capabilities gained through the acquisitions of ACP and J-Dragon were quickly imparted to other company facilities. This allowed GVT to remove geographical limitations and not be confined to just one site.

The CEO is also focused on positioning GVT as a comprehensive solutions provider in the advanced materials sector, with particular emphasis on bonding alloys and ceramics. In parallel, the company plans to broaden its market presence by opening an office in North America. This plan will enable GVT to collaborate closely with customers, assist in product introductions, and even contribute to shaping product roadmaps. As with all of GVT&rsquo s offerings, these advanced material capabilities will be applicable across its diverse verticals, serving clients from a range of industries.

Ng is optimistic about GVT&rsquo s growth over the next five years. Despite a delayed recovery in some segments, the semiconductor industry remains a promising and dynamic sector.

The US authorities may have imposed certain restrictions on the semiconductor industry, but this is still a market worth about US$1 trillion. US funding to help beef up its domestic chip-making capabilities might lead to lower utilisation rates because of new capacity. &ldquo But if you look at it from another perspective, state funding could also create plenty of opportunity,&rdquo he adds.

Whether or not GVT&rsquo s Bursa plans come true, Ng wants investors to know that the company is ahead of the curve and is distinct from many of its peers. He adds: &ldquo Rather than just being reactive, we are a bit proactive we look for innovative ideas to serve our clients better. We have invested quite heavily over the last few years, and we are excited to see all these investments bear fruit for at least the next few years.&rdquo

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

SmallSmall

Supreme |

19-Dec-2024 11:51

|

||||||||||

|

x 0

x 0 Alert Admin |

$1.00 stock in the making... NEWS RELEASE GRAND VENTURE TECHNOLOGY SELECTED AS A PREFERRED SUPPLIER FOR ADVANCED SEMICONDUCTOR PACKAGING EQUIPMENT (THERMAL COMPRESSION BONDING) Expansion of GVT&rsquo s presence in the supply chain of a leading global semiconductor assembly and packaging equipment manufacturer for key technologies like Hybrid Bonding and Thermal Compression Bonding Strong multi-year growth prospect driven by the rising demand for end-market applications Singapore, December 18, 2024 &ndash Mainboard-listed Grand Venture Technology Limited (杰 纬 特 科 技 有 限 公 司 , &ldquo GVT&rdquo , or the &ldquo Group&rdquo ), a regional precision manufacturing solutions provider, is pleased to announce that it has been selected as a preferred supplier of High Level Assembly, inclusive of precision parts and components for next generation Thermal Compression Bonding (&ldquo TCB&rdquo ) equipment by a leading global semiconductor assembly and packaging equipment manufacturer. This win was enabled by the Group&rsquo s early engineering engagement and strong collaborative relationship with the customer. This milestone reinforces GVT&rsquo s position as a trusted partner for leading semiconductor companies in delivering high-precision, high-performance components and modules that are critical in cuttingedge semiconductor technologies. Our customer&rsquo s equipment, designed for TCB, plays a vital role in advanced semiconductor packaging that enables the next generation performance of semiconductor chips. TCB enables advanced semiconductor chips that drive diverse end applications across data centres, graphic cards, AI accelerators, mobile application processors and high bandwidth memory, to address the needs of high-performance computing, advanced graphics, AI workloads and cloudbased solutions. This represents a major win for the Group, as we anticipate this achievement to play a pivotal role in driving new opportunities and revenue growth momentum starting from 2025 onwards. |

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

SmallSmall

Supreme |

16-Dec-2024 11:12

|

||||||||||

|

x 0

x 0 Alert Admin |

Excerpts from DBS Group Research report Analysts: Amanda Tan & Lee Keng Ling Grand Venture Technology Delayed but not derailed

Investment Overview High-growth company with a strong blue-chip customer base. Over the past five years, GVT has delivered strong revenue and earnings growth with CAGRs of 29% and 16%, respectively. GVT also serves a blue-chip customer base &ndash in the semiconductor back-end space, it serves four of the top six in the analytical life sciences segment, it serves three of the top 10. The products that GVT supplies are made to certain product specifications, and thus its customer base tends to be sticky in nature. Significant contributions from the front-end semiconductor space remain a crucial catalyst. Within the semiconductor segment, GVT&rsquo s exposure to the back end is about 90-95%, implying 5-10% exposure to the front end. Contributions in FY24 from new front-end customers will remain small, while FY25 contributions are expected to be more significant. A promising grand venture nonetheless, as long-term semiconductor uptrend remains intact. Notwithstanding near-term volatility, the semiconductor industry is well poised for growth, owing to the push towards digitalisation.

McKinsey projects that the semiconductor industry will become a trillion dollar industry by 2030. Long-term semiconductor outlook looks bright, which should benefit GVT, as more than half of its revenue comes from the semiconductor segment. The other segments GVT has diversified into should remain resilient, which should help cushion semiconductor weaknesses in the near term.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

SmallSmall

Supreme |

16-Dec-2024 11:09

|

||||||||||

|

x 0

x 0 Alert Admin |

Major breakout on the chart ! $0.063....+$0.035 | ||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

|

|||||||||||

|

Joelton

Supreme |

09-Nov-2024 11:15

|

||||||||||

|

x 0

x 0 Alert Admin |

Grand Venture Tech registers 9MFY2024 adjusted net profit of $6.74 mil, up 59% y-o-y

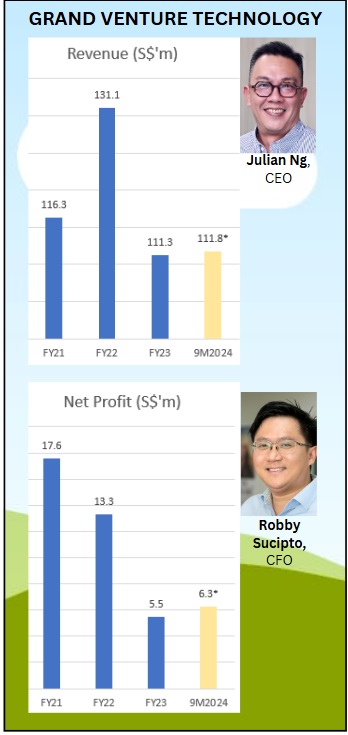

Grand Venture Technology (GVT) has posted 9MFY2024 adjusted net profit of $6.74 million, up 59% y-o-y.

Revenue for the period grew 35.8% y-o-y to $111.9 million, largely due to growth across all key business segments. Growth was more prominently recorded in the semiconductor segment, with a y-o-y increase of 50.8%.

Adjusted ebitda grew by 24.8% y-o-y to $21.6 million. Gross profit margin and adjusted ebitda margin stood at 26.4% and 19.3% respectively.

Although there are early signs of improvement in semiconductor demand, GVT remains cautiously optimistic for the next quarter with further strengthening expected in 2025.

The company is winning higher wallet share from its key aerospace customers and expects the healthy demand momentum to continue. This is on the back of resilient performance from the life sciences and medical segments

GVT is confident in achieving the higher end of previous target revenue guidance of between $80 million and $86 million for the 2HFY2024 ended December 31.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

12-Sep-2024 08:31

|

||||||||||

|

x 0

x 0 Alert Admin |

Singapore-traded Grand Venture Technology eyes second listing in Malaysia

The company&rsquo s shares are about 60% lower than a peak three years ago as it aims for a higher valuation on Bursa Malaysia

GRAND Venture Technology (GVT), which produces components for semiconductor makers and other industries, is targeting a second listing in Malaysia, sources said.

GVT is working with advisers for a listing as soon as 2025, they said, asking not to be identified discussing private information.

It is considering a listing by introduction, meaning it would not be raising funds, one of the sources added. Deliberations are ongoing.

Grand Venture Technology (GVT) confirms that it is in discussions for a potential secondary listing of its shares on the Main Market of Bursa Malaysia.

In a filing pre-market opening on September 12, the company says it is still planning the details and structure of the proposed secondary listing, further clarifying that no application has been made to the relevant authorities.

GVT will make the necessary announcements as and when there are material developments.

GVT&rsquo s shares are down about 7 per cent in Singapore over the past 12 months, and some 60 per cent lower than a peak three years ago.

This gives the company a market value of S$188 million. GVT is aiming for a higher valuation by listing in Kuala Lumpur, where initial public offerings (IPO) have been on the rise this year, the sources noted.

The IPO would extend a reversal in a trend of Malaysia-based companies seeking listings in Singapore, which is viewed as more of a financial hub with access to global investors.

UMS Holdings, another Singapore-listed maker of semiconductor components, said in July it was also considering a second listing in Malaysia to widen its investor base and boost the liquidity of its shares.

Singapore has had only one listing this year, with the Singapore Institute of Advanced Medicine Holdings raising US$20 million, while IPOs in Malaysia have brought in US$1.3 billion, Bloomberg data showed.

Bursa Malaysia had 34 IPOs year-to-date and believes that it would reach its 2024 goal of 42.

Founded in 2012, GVT makes parts such as sheet metal components and modules for semiconductor, life sciences, aerospace, medical and other industries, its website shows.

Its revenue for the first half of 2024 rose 27 per cent from a year earlier to S$68 million, with sales from the semiconductor segment contributing to half of that, the company said in a filing. Net profit was S$4.3 million.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

15-Aug-2024 12:18

|

||||||||||

|

x 0

x 0 Alert Admin |

Grand Venture Technology announces 26.6% growth in net profit in 1HFY2024

Precision manufacturing solutions provider Grand Venture Technology reported a 26.6% rise in net profit to $4.3 million in 1HFY2024 for the six months to June 30. Revenue for 1HFY2024 increased by 26.8% to $68.3 million, exceeding the top end of GVT&rsquo s revenue guidance of between $58 million and $64 million.

The group saw stronger business activities across its key segments including semiconductors, Life Sciences, as well as Electronics, Aerospace, Medical and Others (EAMO).

Sales from the Semiconductor segment remained the largest revenue contributor at 50.2%. Revenue from the segment rose 31.6% y-o-y to $34.3 million for 1HFY2024 driven by progressive improvement in orders from its key back-end customers, including the shipment of testing equipment for high-bandwidth memory, a critical component in AI processors. Revenue from the life sciences segment was up by 4.3% to $10.2 million for 1HFY2024 on the back of expanded wallet shares with key customers.

Revenue from the EAMO segment surged by 32.2% or $5.8 million to $23.8 million. The group also saw organic growth from aerospace, medical, andothers industries, offsetting the soft demand from the Electronics segment.

As of end June, the group had total borrowings of $67.6 million, up from $49.0 million as of December 31 2023. The increase in borrowings was partially due to the debt raised for the ACP acquisition. GVT&rsquo s debt-to-equity ratio stood at 0.55 times as at end-June.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

30-May-2024 09:39

|

||||||||||

|

x 0

x 0 Alert Admin |

Grand Venture Technology registers 1QFY2024 net profit of $2 mil, up 34.1% y-o-y

Grand Venture Technology (GVT) has posted net profit of $2 million for its 1QFY2024 ended March, up 34.1% y-o-y driven by continued wallet share expansion with its key customers.

Revenue grew 14.4% y-o-y to $30.8 million, while ebitda grew 10.6% to $6.47 million.

Gross profit margin and ebitda margin were relatively stable in the quarter, with continued ongoing absorption of expanded capacities and capabilities in preparation for future growth, the company says in a filing.

Segment-wise, revenue from the semiconductor segment increased by 14.8% y-o-y to $15.7 million, mainly due to gradual demand recovery.

The life sciences segment recorded a 6.2% growth y-o-y to $5 million. This is attributed to the commencement of mass production of certain mass spectrometers and its bolt-on instruments as well as expanded wallet share in the segment.

Revenue from the electronics, aerospace, medical and others segment rose 18.4% y-o-y to $10.1 million in 1QFY2024. This is due to robust demand from customers from the aerospace and medical industries, which was partially offset by weakness in the electronics segment.

Following its acquisition of ACP Metal Finishing (ACP) in March 2024, GVT has commenced integration of ACP&rsquo s operations, employees and resources with GVT&rsquo s. Apart from the anticipated post-integration synergies, the company expects to leverage the combined offerings to strengthen its competitive position among current and potential customers in the front-end semiconductor industry.

While rapid innovation in artificial intelligence (AI) is driving additional chip demand around graphic processing units (GPU) and high bandwidth memory (HBM), the outlook is uneven across the customers in this sector, the company says. As such, GVT is cautiously optimistic about a gradual improvement in semiconductor demand in the later part of 2024.

GVT is confident in achieving the higher end of its February 26 target revenue guidance between $58 million and $64 million for the financial period ending June 30.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

06-Jan-2024 08:51

|

||||||||||

|

x 0

x 0 Alert Admin |

CGS-CIMB stays upbeat on Grand Venture Technology following $17 million acquisition of ACP

CGS-CIMB' s William Tng has kept his " add" call on Grand Venture Technology JLB 0.00% , following the manufacturer' s move to acquire ACP Metal Finishing.

The acquisition was announced on Nov 30 and will add surface treatment to GVT' s existing capabilities in precision manufacturing.

Surface treatment is a critical last-stage process that is required by GVT&rsquo s customers in the aerospace, front-end semiconductor, life sciences and medical segments.

The proposed acquisition of ACP enables GVT to reduce its reliance on external parties for surface treatment services.

At $17 million, the acquisition price translates into a historical P/B of 1.13x, based on ACP' s end Sept 2023 book value of $15.1 million.

For ACP' s FY2023 ended Sept 23, it incurred a slight loss of $0.76 million, from earnings of $1.53 million in the preceding year. Revenue in the same period was down from $18.07 million to $14.96 million.

Since it was listed in Jan 2019, GVT has undertaken a rather active grow-by-acquisition strategy. According to Ting, GVT is next eyeing a business in advanced materials, giving itself a broader portfolio of related services to offer clients.

In the meantime, Tng has pencilled in a 5% reduction in earnings forecast for FY2023 ended Dec, no thanks to unfavourable forex.

In addition, with expected integration costs from ACP, Tng expects operating costs to increase by 6.9% in the current FY2024, leading to a 15.5% cut in projected earnings for the year. " Our FY2025 forecasts are unchanged," he adds.

Nonetheless, Tng is upbeat that GVT will enjoy earnings growth this current FY2024 and coming FY2025. His target price of 62 cents is based on FY2025 PE of 11.6x, which is the average earnings multiple in the last earnings growth cycle seen between FY2019 and FY2021.

Downside risks include a slower-than-expected recovery in the semiconductor cycle, and sluggish or delayed resumption in demand from customers.

On the other hand, re-rating catalysts include potential new customer wins and accretive M& As leading to higher revenue and earnings potential.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

01-Dec-2023 12:03

|

||||||||||

|

x 0

x 0 Alert Admin |

Grand Venture to acquire surface treatment specialist for S$17 million

MANUFACTURING service provider Grand Venture Technology : JLB +1% is looking to acquire Singapore-based ACP Metal Finishing for an aggregate consideration of S$17 million in cash.

The company intends to fund this through a combination of internal resources and bank borrowings.

ACP Metal is a surface treatment specialist involved in various electrochemical and chemical processes to coat metals for industries including precision engineering manufacturers, life sciences, optics, medical, and semiconductor companies. It also provides customised electroplating services.

It is currently held by investment holding company Ardille, which is 37.5 per cent-owned by recently delisted property player Chip Eng Seng. The remaining majority of 62.5 per cent is held by Budleigh Engineering, who primarily invests in precision engineering companies.

On Thursday (Nov 30), Grand Venture highlighted surface treatment as a &ldquo critical process&rdquo required by many of its customers &ndash particularly in the aerospace, semiconductor, life sciences and medical segments.

By expanding the group&rsquo s capabilities to surface treatment, Grand Venture said the deal was in line with its overall strategy to better serve its customers while reducing its external reliance for such services.

&ldquo The proposed acquisition aligns with Grand Venture&rsquo s strategy to provide a one-stop full suite of services, alongside its current capabilities in ultra-precision machining, sheet metal fabrication, mechatronics assembly and testing.&rdquo

The deal is also seen to enhance the group&rsquo s competencies in the aerospace segment while expanding its customer touchpoints in this segment, from mainly China, to include Singapore and the region.

Grand Venture added that acquiring ACP Metal was &ldquo essential&rdquo for the group&rsquo s long-term competency build to &ldquo further penetrate the front-end semiconductor segment and equip the group with a differentiated advantage&rdquo .

Based on unaudited financial statements, ACP Metal&rsquo s net tangible asset value and book value stood at S$14.4 million as at end-June 2023.

Grand Venture estimates the acquisition would have reduced its net tangible assets per share as at Jun 30, 2023, to S$0.3079 from S$0.3165, had the deal been completed on Dec 31, 2022.

Assuming that the acquisition of ACP Metal took place on Jan 1, 2022, the group&rsquo s earnings per share as at Jun 30, 2023, would have stood at a lower S$0.007 compared to S$0.01.

An extraordinary general meeting will be convened to seek Grand Venture shareholders&rsquo approval for the acquisition.

Grand Venture&rsquo s executive deputy chairman Lee Tiam Nam, its chief executive and executive director Julian Ng, and its controlling shareholder NT SPV 12 have irrevocably undertaken to vote in favour of the deal.

As at Nov 30, 2023, Lee holds shares representing 15.37 per cent of the company, with Ng holding 3.55 per cent. NT SPV 12 owns a 26.68 per cent stake.

Shares of Grand Venture closed unchanged at S$0.50 on Wednesday before the group requested a trading halt on Thursday morning. The counter resumes trading after Thursday&rsquo s midday break.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

16-Nov-2023 08:23

|

||||||||||

|

x 0

x 0 Alert Admin |

Grand Venture Technology net profit down 61.6% to $1.3 million for 3QFY2023 as semicon headwinds persist

Manufacturer Grand Venture Technology (GVT) has reported a net profit of $1.3 million for its 3QFY2023 ended Sept 30, a 61.6% slump compared to its net profit for the same period last year.

Revenue for the period also fell 13.4% to $28.5 million, with a decrease in business activity in GVT&rsquo s back-end semiconductor and electronics segments year-to-date.

As a result, gross profit decreased by 22.9% to $6.6 million while gross profit margin lost 2.9 percentage points, falling to 23.0% in 3QFY2023.

The ongoing absorption of expanded capacities and capabilities also contributed to the decline in gross profit and margins.

The company says that while the global semiconductor and electronics industry downturn looks to be bottoming out, it expects headwinds to continue for the rest of 2023.

However, GVT is cautiously optimistic of a gradual improvement in operating conditions from 2024, with a more pronounced uptick in the second half of 2024 to be driven by global semiconductor demand for innovations in artificial intelligence and high-performance computing, and the need for inventory replenishment.

The company&rsquo s facility in Penang, Malaysia, which will be dedicated to front-end semiconductor activities, is expected to be operationally ready by the end of the year, in preparation for a pick-up in order momentum next year.

Meanwhile, GVT continues to work closely with its new back-end semiconductor customer on first article inspections and qualifications.

For its life sciences business, the company has commenced work internally to develop capabilities in the area of advanced materials in order to carry out new projects. GVT adds that it is also actively capitalising on the recovery of the global aviation industry to secure new orders and expand its customer wallet share in the aerospace segment.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

|

Joelton

Supreme |

27-Sep-2023 10:57

|

||||||||||

|

x 0

x 0 Alert Admin |

Citing ' gradual' recovery, CGS-CIMB maintains ' reduce' call on Grand Venture Technology

William Tng of CGS-CIMB, in his Sept 26 note, has reiterated his ' reduce' call on Grand Venture Technology JLB 0.88% , given limited visibility of an early recovery to be enjoyed by the electronics manufacturing industry.

GVT reiterates that the industry remains affected by geopolitical tensions and weakness in the global economy.

" The semiconductor recovery could be gradual and the pace of orders from new front-end customers could be slow in FY2024," says Tng.

Nonetheless, GVT is optimistic that there are some signs of easing of excess inventory and expects order momentum to pick up towards the year end and into the coming FY2024, says Tng.

In addition, GVT maintains that the mid- and long-term outlook of the semiconductor industry is strong, led by growing investment in AI and its applications.

" Hence, GVT continues to grow its capabilities, expand production capacity, and enhance its service offerings to be ready for the next industry uptick," says Tng, adding that the company is making progress to bring on board frontend

semiconductor customers in the metrology, inspection, etch, and wafer deposition segments of the semiconductor industry.

A new plant dedicated for front-end customers is on track to be ready by the end of the year and production equipment has been installed.

Meanwhile, GVT sees " stable" orders for its other businesses such as life sciences, medical, electronics, and aerospace.

However, Tng prefers to maintain his " reduce" call on the stock, along with a target price of 51 cents. He notes that GVT now trades at 12.5x FY2024 earnings while he values the stock at 11.3x earnings, which is 0.5 standard deviations below its 3-year average given limited visibility of an early recovery.

Tng warns that possible de-rating catalysts might include a severe drop in customer orders if the world slips into a recession and higher-than-expected spending for long-term growth.

Upside risks, on the other hand, will be potential new customer wins with significant purchase orders and accretive M& As, resulting in better earnings and quicker-than-expected return of customer demand.

|

||||||||||

| Useful To Me Not Useful To Me | |||||||||||

Asked about this at the recent 3Q2024 results briefing

Asked about this at the recent 3Q2024 results briefing