Latest Forum Topics /

SIA

Last:6.97

-0.08

-0.08

|

|

|

SIA

|

|||||

|

gregtan123

Supreme |

17-May-2020 17:28

|

||||

|

x 0

x 0 Alert Admin |

That' s a smart move. Almost all people i know will let the MCB R lapse. But I think the fair question to ask is should T pay u 0.001 or 0.002 or any money to buy your Right to Subscribe the MCB? It seems like they are trying to take advantage of shareholders here. Note key word: seems.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Goldfinger

Supreme |

17-May-2020 17:24

|

||||

|

x 0

x 0 Alert Admin |

Okay thanks - I am now inclined to let the SIA MCB Rights lapse. The risk of it trading below SGD1 is not small in my view, and actually quite likely. Meaning, it could be cheaper to buy this on the open market after it begins trading?

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

gregtan123

Supreme |

17-May-2020 17:22

|

||||

|

x 0

x 0 Alert Admin |

But short MCB R no issue right? Short at 0.002 then last day buy back 0.001?

|

||||

| Useful To Me Not Useful To Me | |||||

|

stanleytay

Master |

17-May-2020 17:20

|

||||

|

x 0

x 0 Alert Admin |

I rem Muddy Waters shorted Olam many years ago.. and in the end it failed to bring Olam down. In their statement, they wrote something like if not for govt intervention in Temasek, Olam would have gone down like Noble. Shorting SIA requires precision and timing... its not that SIA will do well now, when the big boys move in, the shorts will be taken out for sure.

|

||||

| Useful To Me Not Useful To Me | |||||

|

CheeryVGoh

Supreme |

17-May-2020 17:16

|

||||

|

x 0

x 0 Alert Admin |

SIA&rsquo s Rights Issue and MCB Explained &ndash Is Singapore Airlines a good investment?

Quite a few readers have asked that I do a piece on SIA. And it&rsquo s a really interesting topic, so I was happy to oblige. A reader also helpfully sent across the following questions, which we&rsquo ll use as the framework for discussion today: Sign up for Weekly Updates

1) Some interpretation about the complex structure Rights + MCB 2) The valuation of SIA after the rights/MCB? 3) Your recommendations to FH followers on SIA &ndash whether we should subscribe to entitlement or even excess rights? FYI we&rsquo ll share commentary on the 2020 crisis every weekend going forward, so for those of you who haven&rsquo t signed up for our mailing list, please do &ndash its absolutely free. It&rsquo s a weekly newsletter that goes out at noon every Sunday, and rounds up the week&rsquo s posts so you never miss anything. Sign up below (you get a free guide when you sign up): Email address:

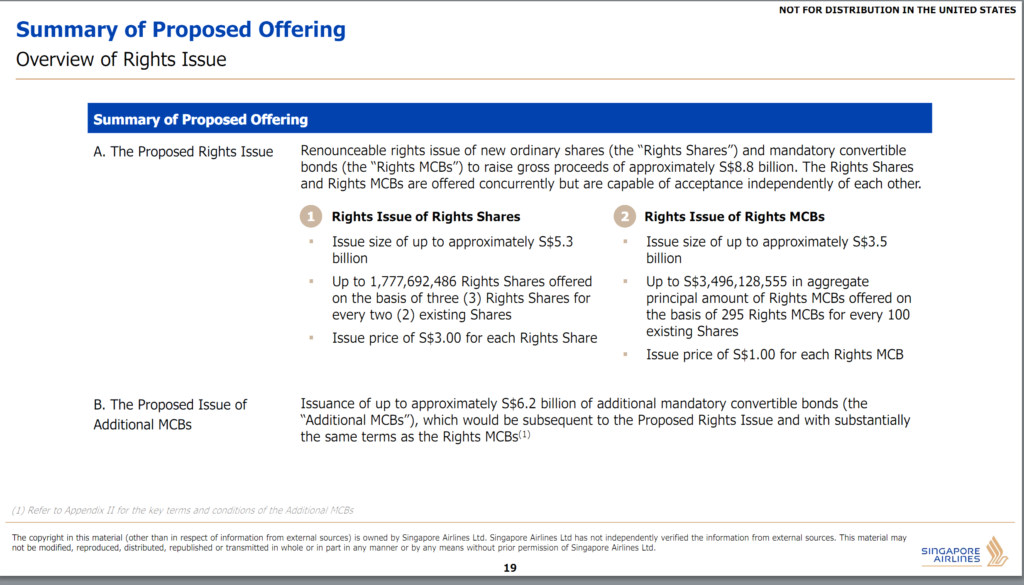

1) Breaking down the Rights Issue and MCBsAll of the relevant documents are available here: https://www.singaporeair.com/en_UK/sg/about-us/information-for-investors/rights-issue/.

Very simply, SIA&rsquo s &ldquo bailout&rdquo is split into 3 parts:

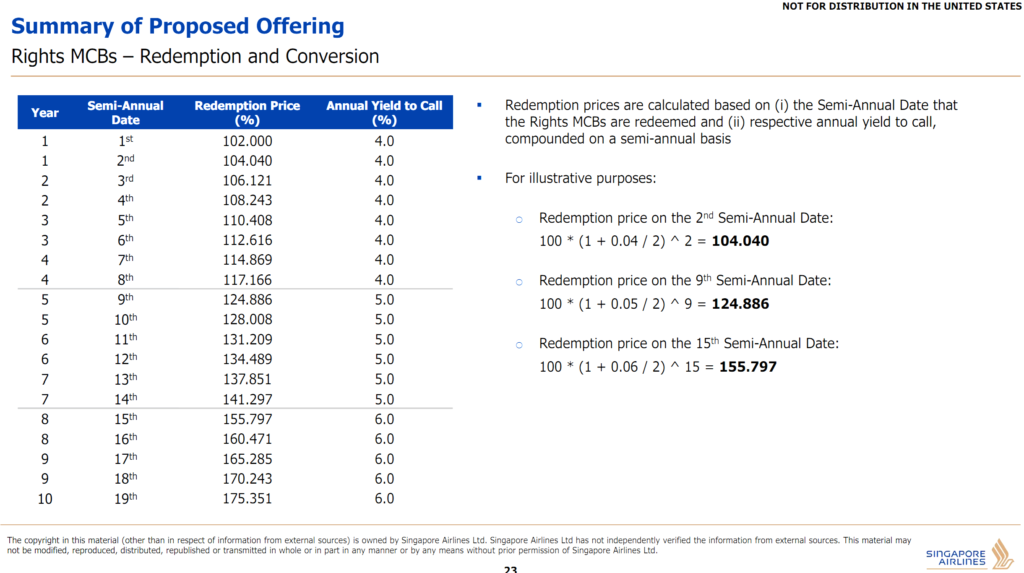

Parts 1 and 2 are happening right now, whereas Part 3 may happen later depend on how much cash SIA needs down the road. Part 1 &ndash Rights issue of Rights Shares (raising $5.3 billion) Plain vanilla rights issue. For every 2 shares in SIA you own, you get3 rights at $3.00 each. You can either choose to (1) exercise the rights to get a share in SIA &ndash in which case you need to pay $3.00 per right, or you can (2) sell the rights on the open market &ndash in which case you take the price of the rights on the open market, which is about $3.8 as of today. This will raise a total of $5.3 billion for SIA Part 2 &ndash Rights Issue of Rights Mandatory Convertible Bonds (MCB) (raising $3.5 billion) The MCBs are more unique. I don&rsquo t think I&rsquo ve seen these ever being offered to retail investors, at least not in this debt cycle. The MCBs are pretty technical, so we&rsquo ll skip all the mumbo jumbo and go right into what it means. Imagine that you own $1000 of MCBs. These are zero coupon, so you&rsquo ll not get paid any interest (or coupon) each year. But these MCBs can be redeemed by SIA any time within 10 years. And on redemption date, they will pay you $1000 (being the principal) + an extra amount equivalent to the interest that would have been due on the bonds for the duration that you held it. And the interest is 4% for the first 4 years, 5% for year 5 to year 7, and 6% for year 8 to year 10. So basically, if SIA redeemed the bonds in year 4, you will get no interest payments for the first 4 years, but on redemption date you get a lump sum payment equivalent to $1117.166, which is the $1000 you put in originally, and $117.166 which is equivalent to the 4 years interest at 4% a year. If redeemed in Year 5 &ndash then SIA basically pays 5% a year to you, but as a lump sum at the end. Full numbers are set out in the table below.

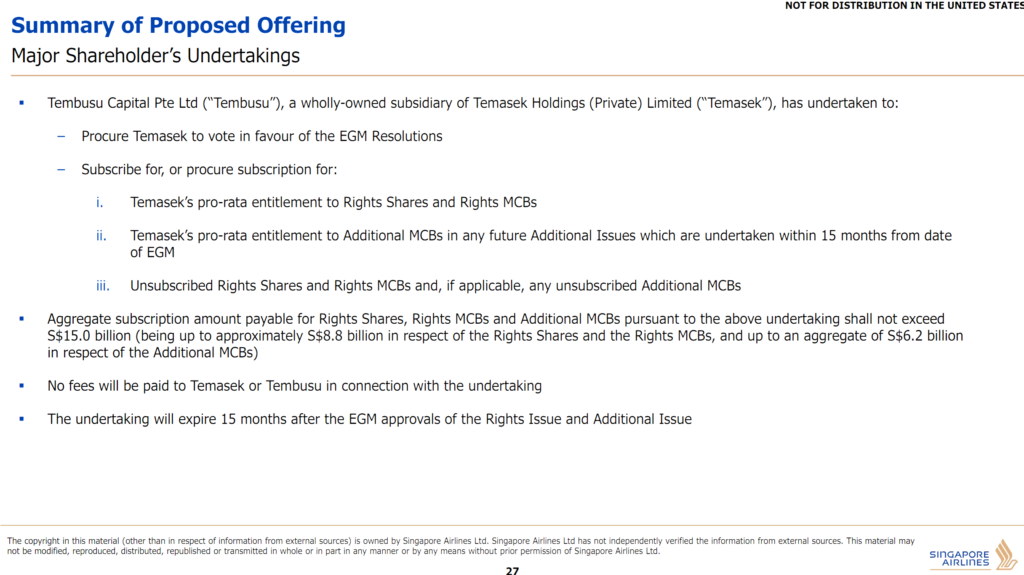

So no interest is payable by SIA every year, which is great because nobody knows when COVID19 goes away. This gives SIA lots of flexibility to repay the MCBs only when cash flow has recovered to a point where they are comfortable paying these off. What if SIA doesn&rsquo t have the cashflow to redeem the MCBs? Then in year 10, you still get paid a lump sum of $1,806.11, which is the $1000 principal and 10 years&rsquo worth of 6.0% coupons. Only difference is that instead of being paid in cash, you&rsquo ll be paid in SIA shares. So you will get the number of shares equivalent to $1,806.11 dollar value &ndash based on S$4.84 per Share (subject to adjustments). This works out to roughly 373 Shares per 1000 MCBs. For every 100 shares in SIA you hold, you will get 295 Rights MCBs. The MCBs will raise $3.5 billion. Part III &ndash A proposed further issuance of Additional MCBs (up to $6.2 billion) Part III is basically just an option to issue even more MCBs down the road, up to $6.2 billion more. So if 3 months (or 1 year) later SIA is still not doing well, then they can tap the additional MCBs to raise up to another $6.2 billion. Same mechanic as how they work in Part II. Summing it up So to sum it up &ndash for every 100 shares in SIA you hold, you get 150 rights shares at $3 each, and 295 rights MCB at $1 each. Assuming a pre-rights but post-COVID price of about $6 per SIA share, this means that for every $600 in SIA shares you hold, you&rsquo re being called on for $450 in rights, and $295 in MCBs, totaling $745. That&rsquo s quite a big capital call from shareholders now that I think about it. Undertaking from Temasek In any case, Temasek is backstopping the entire offering. So if you don&rsquo t want the rights or MCBs, Temasek will buy the remainder. The total amount being raised is $8.8 billion Part I and II, and up to another $6.2 billion in Part III. To put things in contrast, SIA&rsquo s current market cap is about $11 billion, so that&rsquo s a big bailout package.

2) The valuation of SIA after the rights/MCB?This was what I wrote for Patrons back in March: &ldquo The key thing about this bailout is that it is massively dilutive. Some back of the envelope calculations &ndash assuming an original share price of $9 pre-COVID19, after the dilutive rights, the final price of the shares will be about $5.4, give or take. So assuming SIA recovers to its pre-COVID19 earnings and valuations, the share price for SIA should be around the $5+ range (really rough calculations). Which means the current post-rights effective share price of SIA of $4.4 isn&rsquo t looking so attractive (assumes you buy now and subscribe for the rights in full). I haven&rsquo t taken a look at SIA so closely yet because I think it&rsquo s way too early to be touching airlines, but ballpark number to get me interested will probably be in the $2 to $3 range. It may never get to that price, in which case I just skip the stock entirely. Too many other bargains out there, with bigger upside and less risk. If I did want to play SIA though, I think the right time to start looking is probably when the rights entitlement start to trade.&rdquo Traditionally, the best time to get into a stock is when the rights entitlement start to trade. Applying that here, it would mean now is the perfect time to open a position in SIA if one is so inclined. But of course, I do have my doubts on whether that rule will hold true here. Valuations I am a big fan of the rubbish in rubbish out theory. This is the simple idea that any model you build, is only as good as its inputs. And to build a valuation model of SIA, what is the most important input that I would need right now? If you guessed earnings, you&rsquo re absolutely right. If you can tell me what SIA&rsquo s earnings will be like for 2021, and 2022, and 2023, I can give you a valuation for SIA. So let&rsquo s go back to basic principles. What do I need to forecast SIA&rsquo s earnings? I need to know revenue &ndash and for this I need to know what international airtravel will be like in 2021 and out (because Singapore doesn&rsquo t have domestic air travel). So I basically need to know what the COVID19 situation will be like, what kind of measures global governments are taking to combat the spread, and just much of a pain in the ass it will be to take an international flight. Because if I need to do a swab test and mandatory quarantine each time I cross international borders, I&rsquo m probably just not going to travel internationally for a while. The CEO of AirBnb came out with a bold prediction what going forward, travel for business will drop drastically (replaced by Zoom calls), and people will travel more for leisure. Didn&rsquo t make sense at first, but the more I think about it, the more I appreciate the genius of this comment. Nobody wants to put up with all that hassle for a business trip, but a leisurely trip to Japan for some Sashimi? Hell yeah. But coming back, I think the simple answer here is that no one has any clue what international travel will be like 3 months out, 6 months out, or 12 months out. So valuation of SIA? I have no clue. Ballpark numbers Okay but let&rsquo s run some rough, ballpark numbers to give ourselves a gauge. Taking SIA&rsquo s pre-COVID price of about $9 per share, and adjusting for 3 for 2 rights are $3 per share, we have an adjusted price of about $5.4. So if everything recovers and we go back to Dec 2019 flight numbers and valuations, SIA will go to about $5.4, which is about a 40% upside from here. Investing is about risk reward, so the question is how likely is that 40% upside, and how much are you risking for that 40% upside. And genuinely &ndash your guess is as good as mine. 3) Your recommendations to FH followers on SIA &ndash whether we should subscribe to entitlement or even excess rights?Okay first things first &ndash I don&rsquo t do recommendations. Investing is a very personal decision, and you need to decide based on your risk appetite, and your goals. I can&rsquo t make that decision for you. It&rsquo s your money, and yours alone. All I can do it share my thought process, and hopefully it will be helpful for you in making your decision. What would I do? There are 2 kinds of people in this world. Those who think that air travel will recover over the next 2 to 3 years. And those who think that there is no way of knowing for sure. Which now that I think about it, is kinda like how religion works. Anyway, I belong in the second camp &ndash the agnostic camp. This camp includes guys like Warren Buffet, who some would say has lost his edge in his old days. Whatever the case, my position is that it&rsquo s impossible to know for certain how air travel will play out the next 2 to 3 years. Maybe COVID19 goes away, and everything goes back to normal. Maybe the virus mutates into a more deadly strain, and it&rsquo s the end of the world. Maybe we are just stuck in this status quo where you need a 2 week quarantine when you cross borders. The way I see it, all of them are possible futures, and because this isn&rsquo t a financial problem, I don&rsquo t see how I can assign probabilities to each of the possible futures. So if I buy now, I&rsquo m just making a blind bet that everything will get better, and to convince me to do that, I need a big upside, and a big margin of safety. If I were a shareholder? I think if I were a shareholder (and I&rsquo m not), I probably would have sold all of my shares in April when it was at the $6 range. I just have no clue what air travel will be like for the next few years, and at $6, the price was too good to not exit. If I somehow missed the boat then, and held on till now, then I think I have no choice but to take up the rights, because otherwise I would get diluted out (in any case the rights are cheaper than the market price of the shares, so it&rsquo s a no brainer). History shows that the time when rights are selling are usually a poor time to exit your investment, so I would take up the rights and hope for a small bounce after this goes away. This also gives me time to watch COVID play out. If everything clears up quicker than expected, SIA could just turn out to be a great investment. If I were not a shareholder? As a non-shareholder, I think there are 2 potential ways to play this: Short term flip One way is to buy SIA now at the $3.8 range. Short term there is the possibility of a bounce into $4+, and if it does, I exit the investment completely. But the question really is how much am I risking for this return. This is essentially a trading-style strategy, which I am not good in, so I&rsquo ll leave it to the traders out there. Long term investment A lot of readers have asked me for my view on SATS. And the views are very similar to SIA. The simple answer is that I don&rsquo t know that the recovery will look like. If I buy into airtravel now, I&rsquo m basically taking a position that airtravel will eventually recover in some form. So then the question is one of pricing. With all the uncertainty, at what price would I be tempted in? I think for SIA, I will stick to the ballpark I threw up in my original Patron post back in March: the $2 to $3 range (between $2.00 and $3.00). Subject of course, to no material deterioration in the COVID19 situation. That said, I genuinely don&rsquo t think SIA will ever drop that low, so I&rsquo ll probably never end up buying this stock. But that&rsquo s fine too, because there are lots of other great buys out there. MCBs look really good though I really like the MCBs though. I think the best way to play SIA could be via the debt, rather than the equity. With debt you&rsquo re taking on credit risk rather than P& L risk, which looks a lot more attractive. The Rights MCBs will be listed on the SGX in due course, so it will be interesting to watch the pricing and liquidity there. Closing Thoughts: View on Temasek BailoutA blogger had a great post back in March on SIA&rsquo s cashflow issues: What this means from a cashflow point of view is that should the situation prevails, the company is burning approximately $1,461m in cash every quarter, or $487m every month. The company&rsquo s balance sheet is in precarious condition by having only $1.5b in cash while having a borrowings that is almost 4 times the amount. Out of those borrowings, $3.75b belongs to the bond issuance which they did over the years while the rest of the $2.35 belongs to bank borrowings. What is more worrying at this point is that the company have a $500m bond that is maturing in Jul 2020 this year, which is simply just 3 months away from today. The next call will mature in Apr 2021, amounting to a smaller amount of $200m. There&rsquo s a fair bit of assumptions going in, but the core message is there &ndash without a bailout, SIA was in real danger of running out of cash. So the way I see it, this bailout is one that absolutely needs to be done. Every country is bailing out their airlines. Singapore would be foolish not to do the same. SIA is our national carrier, and the pride of our nation. It would be a shame to undo all that hardwork because of some squabbles over how to bail them out. So as investors, we can criticize how the deal was done, and maybe we can even come up with a better idea, but we must recognize that it had to be done, and done fast. It&rsquo s easy to criticize when sitting in the comfort of our homes, but when you&rsquo re in the midst of things, scrambling to put together a $15 billion bailout package and satisfying all stakeholders, it&rsquo s a lot harder than you imagine. So I would be slow to criticize how the bailout package was put together. What do you think? Share your comments below!

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

gregtan123

Supreme |

17-May-2020 17:16

|

||||

|

x 0

x 0 Alert Admin |

It depends if T supports. 90% of the layman will say wait for open then buy below. 10% say T support, open 1.01 or 1.02 but then again accounting for Comms, may not be worth it? Long Term answer (everyone reach consensus): better ways to lock ur money then the bad MCB.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Justice888

Supreme |

17-May-2020 17:15

|

||||

|

x 0

x 0 Alert Admin |

Then now short sure make big money . Set stop loss. But stop loss not applicable during balancing. So got risk. If got any good news . Short covering will be crazy.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Goldfinger

Supreme |

17-May-2020 17:08

|

||||

|

x 0

x 0 Alert Admin |

Can I re-ask the question that is probably relevant to most SIA shareholders now - does it make sense to subscribe for the SIA MCB Rights??? If you put in SGD1 now, given the high conversion price of SGD4.84 for the MCBs in 10 years - would this imply that the MCBs will trade below SGD1 after they are listed? If so, throwing money down the drain which goes directly to SIA. Thanks. | ||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

DooDoo

Senior |

17-May-2020 17:04

|

||||

|

x 0

x 0 Alert Admin |

Brace, might hit 3.5 or 3. If i?m not wrong i read somewhere it takes years for the aviation industry to even start to climb back up. That my opinion. Do your own due diligence, make your own choice. Happy trading folks.

P.S if i?m not wrong warren buffet sold all his airline stocks, that should be saying something i guess... dyodd |

||||

| Useful To Me Not Useful To Me | |||||

|

CheeryVGoh

Supreme |

17-May-2020 17:03

|

||||

|

x 0

x 0 Alert Admin |

If sold at $4.4X Ex Rhts & boughtback on Friday at 3.90, already profit, in hindsight.

|

||||

| Useful To Me Not Useful To Me | |||||

|

CheeryVGoh

Supreme |

17-May-2020 16:57

|

||||

|

x 0

x 0 Alert Admin |

CGM CIMB on 6th May 2020 : Post-rights target price of S$4.45 Calculation of ex-rights target price Our financial forecasts for FY21F (year ending March 2021) already incorporate the post-rights and post-MCB issuance position of up to S$8.8bn. We have not yet assumed that SIA will issue the additional MCBs of S$6.2bn. Our target price is based on a slightly lower P/BV multiple of 0.84x, from 0.86x previously, which is still pegged to an unchanged 1 standard deviation (s.d.) below the average since 2011. Since 2011, SIA&rsquo s P/BV multiples have de-rated due to competition issues and SIA continues to trade within these P/BV bands. We have based our target on 1 s.d. below the mean because of the tough conditions which we believe SIA will continue to find itself in over the next 12 months. We think it is unfair to base our target on 2 s.d. below the mean because we have already incorporated the Covid-19 losses into our FY21F P& L forecasts as well as the dilutive impact of the rights issue into our BVPS forecast. The main valuation issue that we have to grapple with is how to treat the Mandatory Convertible Bonds (MCB). According to SIA, the MCBs will be treated as equity on its balance sheet. This is because SIA has an option, but not the obligation, to redeem the MCBs. If SIA chooses not to redeem the MCBs, they will automatically be converted into new ordinary shares on their 10th anniversary of issue, which is also the maturity date. On the basis that the MCBs are treated as wholly equity, we calculate SIA&rsquo s post-rights BVPS to be S$5.89 at the end of FY21F (as at 31 March 2021F) see Figure 4 below. Conversely, SIA may want to redeem the MCBs fully, if possible, and it has a long time frame of 10 years to do so. Our belief is that if industry conditions and SIA&rsquo s balance sheet improve sufficiently during this time frame, it will do its best to redeem the MCBs in order to avoid further dilution for shareholders. As such, the MCBs can be viewed as wholly debt and not as equity. Under this assumption, we forecast the post-rights BVPS of SIA to be S$4.71. In this report, we have decided to take the middle route, i.e. to treat the MCBs as half equity and half debt. On this basis, we forecast the post-rights BVPS of SIA to be S$5.30. Against the post-rights BVPS of S$5.30, we apply our target P/BV multiple of 0.84x to arrive at our post-rights target price of S$4.45. We highlight that our book value forecasts have been reduced by the estimated mark-to-market losses on SIA&rsquo s fuel hedges, based on the current oil price forward curve. |

||||

| Useful To Me Not Useful To Me | |||||

|

gregtan123

Supreme |

17-May-2020 16:50

|

||||

|

x 0

x 0 Alert Admin |

I saw Li Guang Sheng video (investingnote) on the arbitrage. sell mother share, then exercise the rights? I think quite sensible. but of course at this point opportunity may be lost?

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

CheeryVGoh

Supreme |

17-May-2020 16:48

|

||||

|

x 0

x 0 Alert Admin |

Should sell the Rights on the first day if no intention of subscribing IMO.

|

||||

| Useful To Me Not Useful To Me | |||||

|

gregtan123

Supreme |

17-May-2020 16:47

|

||||

|

x 0

x 0 Alert Admin |

I know many say this is gambling with the MCB R issue. But that aside, there' s a very crucial question to be asked: What is the MECHANISM that Temasek gets to exercise the MCB Rs? I mean after all the Right to exercise the MCB belongs to the Right Holder? The logic from a lot of pros that commented is that your Right to MCB becomes worthless on 28 May 2020 when you do not exercise it. But then how does this magically give Temasek the right to exercise the right that has lapsed? Further, assuming that' s the case and logic, then technically if we short 100 million MCB Rs, and the MCB Rs become zero or non-existent, we do NOT have to return something that does NOT exist? To put all in context, and how this relates to the every day man (i.e Long Term holders for SIA say your grandparents or parents, BOOMERS who love the PAP and everything PRO Singapore). Say they got 8,000 shares of SIA (bought at 9 dollars donkey years ago), they are given 23,600 MCB Rs but for them to sell 23,600 at 0.001, it is 23.60 SGD MINUS Commission/Brokerage = it is NEGATIVE. So they cannot sell, only can lapse. Isn' t this T/SIA/Govt way of stiffing the every day investor? Shouldn' t T pay fair value for it? Hope for a meaningul discussion because im sure alot of Uncles and Aunties are being Short-Changed here?

|

||||

| Useful To Me Not Useful To Me | |||||

|

TheDuellist

Senior |

17-May-2020 16:41

|

||||

|

x 0

x 0 Alert Admin |

Yup, I guess the worst is over for SIA. It is highly unlikely price will go below $3. In fact, 3.7x is the best price to enter. Now it has probably turned the corner. However may take a year to see the big difference. Globally, all airlines are affected. The weaker ones will close shop, some may merge to form bigger entities. The stronger ones will become even stronger. SIA is good branding. It will recover fast. Airline businesses mostly depends of passengers. And this pool of passengers is always there. Added bonus is when oil prices weaken when demand for oil becomes lesser and lesser. Not for STengg...but this is not the thread to discuss.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Justice888

Supreme |

17-May-2020 16:35

|

||||

|

x 0

x 0 Alert Admin |

If Temasek do this . Need to declare . Interested parties

|

||||

| Useful To Me Not Useful To Me | |||||

|

gregtan123

Supreme |

17-May-2020 16:31

|

||||

|

x 0

x 0 Alert Admin |

Can someone answer the Key 3rd Question? What if Temasek is selling now and then get back all for free?? Also what if we short 10 million shares, do we even need to deliver? | ||||

| Useful To Me Not Useful To Me | |||||

|

Goldfinger

Supreme |

17-May-2020 16:29

|

||||

|

x 0

x 0 Alert Admin |

Is it even worth the while to take up the SIA MCB RIghts, given the high conversion price of SGD4.84 in 10 years time? Would this erode the implicit yield of 6 percent? thanks.

|

||||

| Useful To Me Not Useful To Me | |||||

|

AhLiang

Elite |

17-May-2020 16:18

|

||||

|

x 0

x 0 Alert Admin |

Most probably no buyer even at 0.001 on the last day. Whoever buys now must take a calculated risk.

|

||||

| Useful To Me Not Useful To Me | |||||

|

gregtan123

Supreme |

17-May-2020 16:03

|

||||

|

x 0

x 0 Alert Admin |

On the MCB R, (1) Can short? What happens if on 21 May when it ends trading you don' t have the MCB R to deliver? But in any case it will lapse so do you need to return? (2) Who is Buying the MCB Rs beyond retail punters like myself (though only 1k worth), the rest of the volume should be a by a BB? (3) Could Temasek be SELLING? Cause they SELL ALL their MCB Rs for 0.001 or 0.002, get FREE cash. then wait for MCB R no one take up. They take for free? Then they earn the " arbitrage" spread? Sounds possible. |

||||

| Useful To Me Not Useful To Me | |||||