Latest Forum Topics /

Tiong Woon

Last:1.05

+0.02

+0.02

|

|

|

Tiong Woon

|

||||||||||||||||||||||||||||

|

Secret_Squirrel

Elite |

30-Mar-2026 12:49

Yells: "Stay curious but skeptical" |

|||||||||||||||||||||||||||

|

x 0

x 0 Alert Admin |

Once Iran war ended, there should be more construction projects. Tiong Woon would probably benefit. Tiong Woon Secures Frame Agreement with Samsung E& A in Saudi Arabia |

|||||||||||||||||||||||||||

| Useful To Me Not Useful To Me | ||||||||||||||||||||||||||||

|

ozone2002

Supreme |

28-Feb-2026 22:22

|

|||||||||||||||||||||||||||

|

x 0

x 0 Alert Admin |

Last:1.01 -- thanks Tiong Woon for the big Ang Pao

|

|||||||||||||||||||||||||||

| Useful To Me Not Useful To Me | ||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||

|

JurongW

Elite |

28-Feb-2026 17:25

Yells: "Earnings give weight, Chart give wings" |

|||||||||||||||||||||||||||

|

x 0

x 0 Alert Admin |

TWC SECURES AND ADVANCES MULTIPLE PROJECTS ACROSS SEMICONDUCTOR, PUBLIC INFRASTRUCTURE AND BIOPHARMACEUTICAL SECTORS SINGAPORE, 24 February 2026, SGX Mainboard-listed Tiong Woon Corporation Holding Ltd (the &ldquo Company&rdquo , together with its subsidiaries, the &ldquo Group&rdquo ), today is pleased to announce ongoing and new execution of three projects across semiconductor, public infrastructure and biopharmaceutical sectors with an estimated combined value of over $40 million. These projects, expected to be completed over the next two financial years, reflect continued customer confidence in the Group&rsquo s technical capabilities, diversified lifting fleet and proven track record in supporting complex, high-specification developments across a broad range of industries. These projects are collectively expected to have a positive financial impact on the earnings per share and net tangible asset value per share of the Group for the current financial year ending 30 June 2026. Mr. Ang Guan Hwa, Executive Director and Chief Executive Officer, said: &ldquo Across semiconductor, public infrastructure and biopharmaceutical sectors, our teams continue to deliver safe, reliable and technically robust lifting solutions for complex, high specification projects. Our diversified fleet, project management expertise and disciplined execution enable us to support a wide range of developments in both public and advanced manufacturing environments&rdquo . Save for the respective shareholdings in the Company, none of the directors, controlling shareholders or substantial shareholders of the Company, has any interest, whether directly or indirectly, in the projects secured contemplated herein. |

|||||||||||||||||||||||||||

| Useful To Me Not Useful To Me | ||||||||||||||||||||||||||||

|

MarcLim

Veteran |

22-Feb-2026 13:08

|

|||||||||||||||||||||||||||

|

x 0

x 0 Alert Admin |

No one buying? huat all 🙏 🏻

|

|||||||||||||||||||||||||||

| Useful To Me Not Useful To Me | ||||||||||||||||||||||||||||

|

SmallSmall

Supreme |

19-Jan-2026 09:11

|

|||||||||||||||||||||||||||

|

x 0

x 0 Alert Admin |

TARGET $1.23

|

|||||||||||||||||||||||||||

&bull Tiong Woon Corp, whose bright orange cranes are a familiar sight across Singapore, is entering its 27th year as a listed firm on the SGX. Longevity on the exchange, especially for a company serving the construction, oil and gas, and petrochemical industries, reflects a business that has successfully weathered more than one economic cycle. &bull For many years, investors were not attracted to this company (recent market cap: S$212 million), let alone accord it a respectable valuation. &bull More recently, the construction upturn in Singapore has boosted the company' s share price more than 30% over the past year to about 80 cents. Last week, an initiation report from CGS International helped push it further, to around 91 cents. Read excerpts of CGS' report below .... |

Excerpts from CGS report

Analyst: Natalie Ong

■ TWC is trading at CY27F P/E of 6.7x, a 45% discount to regional peers despite its global ranking (#15 on IC100) and strong track record.

■ We view TWC as a beneficiary of construction-/infrastructure-focused nation building plans implemented by many SEA and Middle East countries. ■ Initiate coverage with an Add call. Re-rating catalysts include securing larger market share in its various geographies and a higher dividend payout ratio. |

|||||

| Undervalued regional one-stop heavy lift solutions provider |

Tiong Woon Corporation (TWC) is trading at a discount to peers despite its global ranking and track record.

TWC ranks #15 globally on IC100 2024/2025, an annual ranking published by International Cranes and Specialized Transport magazine, and competes for heavier‑ tonnage work (up to 2,200 tonnes) yet trades around 0.6x CY26F P/BV, c.6.7x CFY27F P/E and 1.1x CY27F EV/EBITDA vs. peers&rsquo 2.1x, 12.1x and 5.6x, respectively.

|

Metric |

Tiong Woon |

Peers&rsquo average |

|

CY26F P/BV (x) |

0.6 |

2.1 |

|

CFY27F P/E (x) |

6.7 |

12.1 |

|

CY27F EV/EBITDA (x) |

1.1 |

5.6 |

| Late cycle beneficiary of construction boom, DC and O& G builds |

The majority of heavy lift and hauling services pertain to above-ground or superstructure work, which occurs after foundation/substructure work is largely completed.

Construction of mega projects Changi Airport Terminal 5 and Marina Bay Sands Integrated Resort 2 will run from 2025 till mid-2030F and are currently undergoing substructure works, with superstructure works likely to commence from 2027F onwards.

As at end-2025, contracts for the superstructure work for these two mega projects have not been tendered/awarded.

As such, we believe TWC&rsquo s revenue will grow and peak in FY28F.

| Vertically integrated with regional capabilities |

TWC&rsquo s fleet consists of 579 cranes, 359 haulage assets, 7 tugboats and 9 barges. It also has its own jetty located at its Pandan Crescent headquarters, allowing it to mobilise its cranes to capture overseas opportunities quickly.

With its haulage fleet, it provides transportation services (of cranes/counterweights) to and from the respective sites while its engineering know-how (mechanical and auxiliary engineering capabilities) enables it to offer project-specific lift plans, which we believe positions TWC as a one-stop heavy lift solutions provider.

We also believe its track record of data centre (DC), semiconductor, petrochemical and oil and gas (O& G) projects positions it as a strong contender for such projects, where safety and execution are critical to success.

We initiate coverage on TWC with an Add for its strong regional track record and vertically integrated model.  Natalie Ong, analystWe believe it stands to benefit from various construction- and infrastructure-focused nation-building plans implemented by countries in Southeast Asia (SEA) and the Middle East. Natalie Ong, analystWe believe it stands to benefit from various construction- and infrastructure-focused nation-building plans implemented by countries in Southeast Asia (SEA) and the Middle East.Our TP is based on 4x 2027F EV/EBITDA, a c.28% discount to global peers given TWC&rsquo s smaller scale, which implies FY27F P/E of 10x. Re-rating catalysts include higher fleet utilisation/market share in its various geographies and a higher dividend payout ratio. Downside risks include construction delays impacting TWC&rsquo s crane scheduling, which could lead to an increase in external equipment rental costs. |

Supreme

x 0

Alert Admin

UOB Kay Hian downgrades Tiong Woon Corp to ' hold' but raises target price

Tiong Woon Corp, ranked as the 15th largest crane operator in the world, has reported FY2025 earnings in line with expectations. However, given how the company is incurring higher capex, which is weighing on near-term cash flow and gearing, Heidi Mo and John Cheong of UOB Kay Hian have downgraded the stock from " buy" to " hold" .

Yet, given how Tiong Woon' s share price has gained more than a third in the past six months, they have raised their target price to 73 cents from 64 cents previously.

For its 2HFY2025 ended June, Tiong Woon reported revenue of $164 million, up 14% y-o-y. However, earnings dipped by 4% y-o-y to $7 million on margin pressure and less favourable project mix.

For the whole of FY2025, earnings grew by 6% y-o-y to $19 million, which was 98% of their estimates.

In FY2025, to grow its fleet, the company incurred higher capex of $65.5 million, up 5% over FY2024, which led to higher borrowings of $111.8 million, up 20% y-o-y and lower cash balance of $62.6 million, down 21% y-o-y.

Despite the lower 2HFY2025 earnings and cash balance, the company plans to increase its final dividend to 1.75 cents from 1.5 cents, equivalent to a pay out ratio of 21% from 19%.

From the perspective of Mo and Cheong, the higher dividends is an indication of the management' s confidence in sustainable earnings.

" Tiong Woon remains confident of resilient demand across its core markets, underpinned by petrochemical, semiconductor, infrastructure, and construction activity.

" Leveraging its position as a one-stop heavy lift specialist, we are of the view that Tiong Woon is well-positioned to capture opportunities while staying disciplined in cost and cash flow management. Fleet renewal and expansion should further drive efficiency and strengthen its competitive edge," they add.

For the current FY2026 and coming FY2027, Mo and Cheong have lowered their margin assumptions by around 2 percentage points, due to the expected continued cross-hiring of equipment to meet project demand.

On the other hand, they have raised their revenue forecasts by around 12% on stronger demand across Singapore, India, Saudi Arabia and Thailand.

As a result, their FY2026 earnings forecast has been trimmed by 4% and FY2027' s by 7%.

Their new target price of 73 cents is based on 0.5x FY2026 P/B, which is 0.5 sd above its historical 15-year average P/B, up from 0.45x previously, which is its historical mean.

" While demand drivers remain strong and Tiong Woon has reinforced its global standing, the ongoing high capex cycle is expected to weigh on free cash flow, raise gearing, and cap near-term upside.

" Looking ahead, successful deployment and utilisation of new cranes, coupled with margin recovery as cross-hiring eases and higher-tonnage cranes are progressively deployed, could serve as catalysts for an upgrade in the medium term," the analysts say.

Supreme

x 0

Alert Admin

Tiong Woon earnings for full year 2025 up 6% y-o-y to $19.2 mil

Tiong Woon Corporation Holding has reported earnings of $19.2 million for the full year ended June 30, up 6% y-o-y.

The group&rsquo s revenue for the full year grew 14% y-o-y to $163.5 million, while gross profit grew 4% y-o-y to $61.4 million. However, gross profit margin declined 3.6 percentage points (ppts) to 37.6%.

The group says that revenue growth is due to the increase in contributions from heavy lift and haulage segment, but the lower gross profit margin was attributed to sales mix of projects undertaken during the year.

The group&rsquo s heavy lift and haulage segment external revenue grew 15% y-o-y as the company undertook more heavy lift and installation projects in Singapore, Thailand, Malaysia, Middle East and Indonesia during FY2025.

Its marine transportation segment external revenue remained stable at $2.2 million, while trading segment external revenue decreased to $1.4 million.

The group&rsquo s net assets stood at $322.3 million as at June 30, translating to a net asset value per share of $1.39.

Tiong Woon says that it maintains a positive outlook, as customer demand for heavy lift and haulage solutions is expected to remain resilient in Singapore and key regional markets such as India, Saudi Arabia and Thailand, particularly in the petrochemical, semiconductor, infrastructure, logistics and heavy transport, as well as construction sectors.

Supreme

x 0

Alert Admin

https://links.sgx.com/1.0.0/corporate-announcements/3R9KT3VQACR3Q1MZ/857555_FY25_Press%20Release.pdf

Elite

Yells: "Stay curious but skeptical"

x 0

Alert Admin

Queue at 78.5 cents, not successful.

Master

x 0

Alert Admin

Supreme

x 0

Alert Admin

Elite

Yells: "Stay curious but skeptical"

x 0

Alert Admin

Senior

x 0

Alert Admin

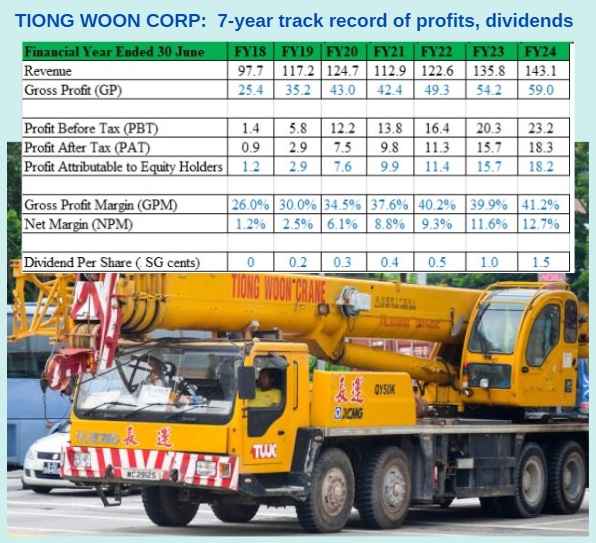

Tiong Woon Corporation, is a laggard and has low liquidity, even when it has delivered 7 consecutive years of profit growth.

https://www.nextinsight.net/story-archive-mainmenu-60/948-2025/16207-tiong-woon-hong-leong-asia-undervalued-winners-in-singapores-construction-surge

UOB KAY HIAN HAS TARGET PRICE OF 64 CENTS .

Member

x 0

Alert Admin

antifragile ( Date: 14-Mar-2025 20:52) Posted:

|

Senior

x 0

Alert Admin

Sin Heng Heavy Machinery receives privatisation offer with S$0.58 per share cash option

https://www.businesstimes.com.sg/companies-markets/sin-heng-heavy-machinery-receives-privatisation-offer-s0-58-share-cash-option

antifragile ( Date: 06-Jan-2025 16:20) Posted:

|

Supreme

x 0

Alert Admin

Tiong Woon reports 12% y-o-y increase in earnings of $12.06 mil for 1HFY2025

Crane operator Tiong Woon Corporation Holding reports earnings of $12.06 million for the 1HFY2025 ended Dec 31, 2024, up 12% y-o-y.

Earnings per share for the reporting period came in at 5.20 cents, also up 12% y-o-y from 4.65 cents in the same period a year ago.

The group&rsquo s revenue grew by 5% y-o-y to $78.8 million, while gross profit decreased by 8% y-o-y to $30.35 million.

Cash and cash equivalents per consolidated statement of cash flows decreased by $8.7 million to $70.5 million as at Dec 31, 2024 due to net cash outflows from financing activities and investing activities of $19.1 million and $8.2 million respectively.

Revenue from the heavy lift and haulage segment grew mainly due to business in Malaysia, Middle East, SIngapore and Indonesia, offset by lower revenue from Brunei. Trading segment revenue also increased.

Gross profit decreased mainly due to external heavy equipment rental, manpower and other costs outpacing revenue growth for the above segments.

Senior

x 0

Alert Admin

Brewing.....

Supreme

x 0

Alert Admin

UOB Kay Hian target $0.87

NAV $1.33

Cash per share $0.3379

Elite

Yells: "Stay curious but skeptical"

x 0

Alert Admin

Supreme

x 0

Alert Admin

Secret_Squirrel ( Date: 20-Nov-2024 16:23) Posted:

|