| Latest Forum Topics / SATS Last:3.99 -- |

|

|

Sats

|

|||||

|

JurongW

Elite |

06-Jun-2026 17:13

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

Still have at least 10% upside to the average target price of $4.42

|

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

06-Jun-2026 16:47

|

||||

|

x 0

x 0 Alert Admin |

Resilient platform at Sats inspires higher target price elevated input costs could cause margin compression The global aviation industry is bracing for some turbulence with fuel costs testing the hedging skills of airline executives. However, for ground handler Sats (SGX:S58) , having integrated the acquisition of WFS, is revving its growth engine just fine, even if not firing on all cylinders. &ldquo The combined group now has a resilient business model, and even when there are ups and downs, because of the network and model, we were able to ride through a lot of these different challenges that came our way,&rdquo says CEO Kerry Mok at the recent results briefing on May 26. While Mok was positive on the latest set of numbers, he was also mindful of the potential impact of the rising input costs due to the ongoing Middle East conflict, as some contracts are set to expire soon. &ldquo Hence, we got to try and manage that with our customers as well,&rdquo Mok says. Nonetheless, the positivity has been reflected in its share price. Following the results, Sats&rsquo share price rose by almost 20% to close at $4.04 on June 3, as various analysts maintained their positive stance on the stock. For Ada Lim of OCBC Group Research, the company&rsquo s FY2026 earnings of 19.2 cents per share were 102.8% of her forecast. &ldquo For now, global travel demand appears to remain healthy, in our view, which should support ground handling and aviation meal volumes,&rdquo she says. However, if the conflict persists and oil prices remain elevated, consumer sentiment will be affected further. For now, she is projecting a slight margin compression in FY2027 to account for higher input and energy costs. While Lim has kept her &ldquo buy&rdquo call, she has lowered her fair value from $4.32 to $4.20, pegged to 20 times FY2027 earnings. For Tay Wee Kuang of CGS International, the company&rsquo s earnings of $50.7 million for the final quarter were slightly ahead of his $45 million forecast. In his May 27 report, Tay reiterates his &ldquo add&rdquo call and raises his earnings forecasts for FY2027 by 7.3% and for FY2028 by 2% to reflect stronger revenue growth in gateway services, resulting in a higher target price of $4.68 based on discounted cash flow, up from $4.53. &ldquo We believe that the reopening of Middle East airspace and the gradual resumption of capacity by Middle East airlines despite the ongoing crisis will augur well for Sats as it continues to gain market share within the global air cargo industry,&rdquo Tay says. He is optimistic that the company can achieve its 5% profit margin target for FY2029 earlier, in FY2028. However, the $8 billion revenue target will be contingent on a larger step-up in contributions from its food solutions business. Despite the near-term cost pressures, UOB KayHian&rsquo s Roy Chen says the company&rsquo s fundamentals remain strong. &ldquo With the diversified global network, Sats is likely to continue gaining market share in global cargo handling. While elevated energy prices may increase operating costs in the near term, cost pressures should be passed through to customers over time,&rdquo he reasons. Sats remains a &ldquo buy&rdquo for Chen, along with the same target price of $4.75, which is based on 19.7 times FY2028 earnings, which is in line with the company&rsquo s historical mean. Meanwhile, Liu Miaomiao and Eric Ong of Maybank Securities are keeping their &ldquo buy&rdquo call and DCF-based target price of $4.52. They expect Sats, with its diversified global network and resilient cargo franchise, to have the necessary buffers against ongoing macro and geopolitical headwinds. &ldquo We also anticipate more meaningful earnings contribution from the Thailand central kitchen in FY2028, as operations are expected to commence in Nov 2026,&rdquo state Liu and Ong, who have raised their FY2027 earnings forecast by 7.1% and FY2028&rsquo s by 4.9%. Jason Sum of DBS Group Research believes that with Sats&rsquo Net debt/Ebitda now broadly within management&rsquo s target range of 2.5 to 3 times, the company should be less pressured to trim its debt load, largely incurred when it acquired WFS. Instead, there&rsquo s now more scope for excess cash to be returned as dividends or buybacks. Sum has raised FY2027 core net income estimates by 2.3% and FY2028&rsquo s by 0.7% on stronger volume assumptions, driven by resilient air cargo demand, Americas ground-handling expansion and higher catering intensity from more direct long-haul flights. Based on an earlier target price of $4.20, Sum figures Sats is worth $4.40. At 17.9 times forward earnings, Sam sees this as a favourable risk-reward ratio. Finally, Hashim Osman of PhillipCapital has raised his FY2027 earnings forecast by 8% due to higher gateway services revenue from new contract wins. He expects the food solutions margins to recover gradually too, as new facilities in Bangalore, Tianjin and Thailand scale toward full utilisation, leading to improved margins. As such, in addition to maintaining his &ldquo buy&rdquo call, he has raised his target price from $4.44 to $4.52. |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

JurongW

Elite |

03-Jun-2026 16:05

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

LIM & TAN

SATS ($3.95, up 10 cents) recently released their results and stated that it achieved 4Q FY26 revenue of S$1.62 billion, an increase of 9.8% compared to the same period last year with growth across all business segments. The Middle East conflict, which escalated in the final month of the quarter, weighed on revenue, costs, operating profit and associates and joint ventures&rsquo earnings. SATS market cap stands at $5.8bln and currently trades at 18.2x forward PE and 2.2x PB, with a dividend yield of 1.8%. Consensus target price stands at $4.42, representing 11.9% upside from current share price. Given the current Middle East conflict that would likely weigh on earnings moving forward and that share price has increased c.24% since our last recommendation, we post an Accumulate on Weakness rating on SATS. |

||||

| Useful To Me Not Useful To Me | |||||

|

Luzern

Supreme |

03-Jun-2026 10:11

Yells: "9" |

||||

|

x 0

x 0 Alert Admin |

Nice. Finally $4 + | ||||

| Useful To Me Not Useful To Me | |||||

|

seanpent

Supreme |

03-Jun-2026 10:03

|

||||

|

x 0

x 0 Alert Admin |

Steady pom-pi-pi ! |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

beng1102

Elite |

03-Jun-2026 09:48

|

||||

|

x 0

x 0 Alert Admin |

Above $4 now.

|

||||

| Useful To Me Not Useful To Me | |||||

|

beng1102

Elite |

03-Jun-2026 09:39

|

||||

|

x 0

x 0 Alert Admin |

Hit $4.

|

||||

| Useful To Me Not Useful To Me | |||||

|

beng1102

Elite |

02-Jun-2026 10:37

|

||||

|

x 0

x 0 Alert Admin |

Easily go back up to above $4. Last closed still above 100% traded volume compares to the average of the last 432 days and closed positive.

|

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

seanpent

Supreme |

02-Jun-2026 10:31

|

||||

|

x 0

x 0 Alert Admin |

We need more hindsight info like this, not after it has happened

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

01-Jun-2026 15:55

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

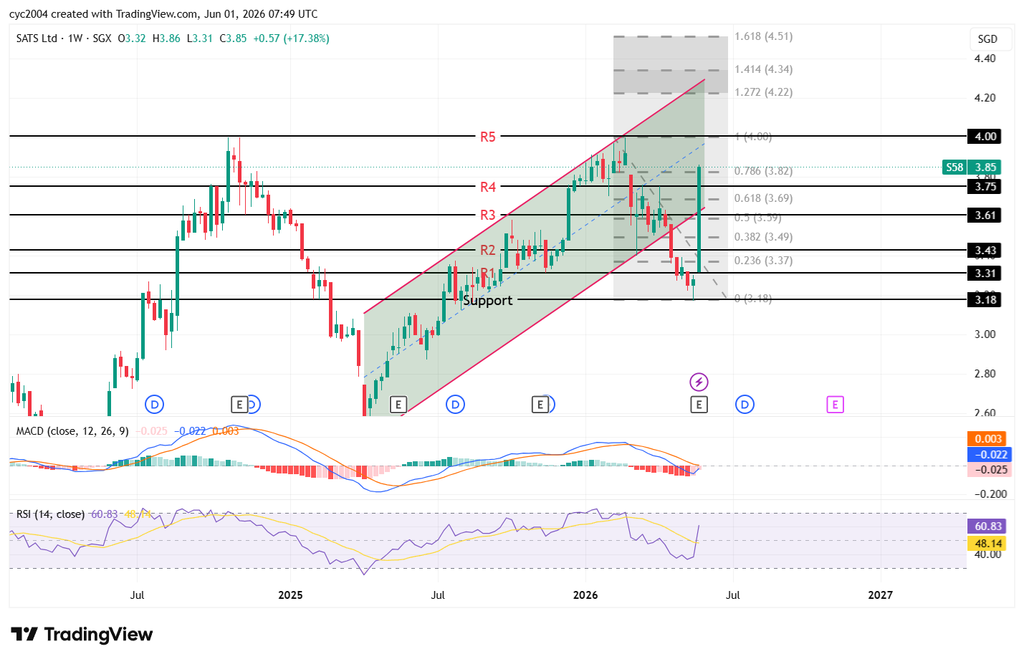

SATS has erased 11 weeks of decline in just 2 weeks. With momentum this strong, a triple top breakout in June could open the runway toward 4.22, 4.34, and even 4.51.

|

||||

| Useful To Me Not Useful To Me | |||||

|

Joelton

Supreme |

30-May-2026 13:36

|

||||

|

x 0

x 0 Alert Admin |

Can Sats sustain growth amid global supply chain disruption? Looking at Sats&rsquo s latest results, the company appears to tick all the boxes financially. For the year ended March 31, revenue was at a record high of $6.3 billion, which represents a growth of 9% y-o-y, while its ebitda margin improved 0.3 percentage points to 18.1%. Patmi rose 17% y-o-y to $285.2 million, while total dividend per share increased 40% to 7 cents. The company&rsquo s shares also climbed 19 cents, or 5.64%, to close at $3.56 on May 26. At the results briefing, Sats president and CEO Kerry Mok says the company was not directly affected in the early stages of the Middle East conflict, as it only has a presence in Saudi Arabia and Oman. &ldquo Due to the chaos, our Middle East operations were affected as the Gulf airline carriers cancelled their flights, which affected us because we are also their cargo handlers in Europe and the United States as well. Hence, if they are not flying, imports will be reduced, and therefore volumes are affected.&rdquo Despite the flight cancellations, Mok says Sats&rsquo s network was able to capture rerouting opportunities, owing to a major investment the company made even as the pandemic&rsquo s effects were still being felt. &ldquo We are proud to state that the platform we created, which was the combination of Sats and WFS, has proven its resiliency in how we navigate any tensions across the global network. From the Ukraine War to the recent Middle East conflict, we were able to withstand some of these shocks and find new paths to grow and find ways to work with our customers and manage the global supply chain.&rdquo Sats has witnessed growth in cargo volume due to the re-routing. For FY2026, total cargo processed grew 7% y-o-y to 9.65 million tonnes, with the majority of the growth coming from Europe, the Middle East, Africa and Asia (EMEAA), which saw 15.3% y-o-y growth to 4.07 million tonnes. Mok believes that Sats is in a privileged position where the company is now talking to customers on a global basis and sharing its network, expertise and ways it can work with them to help manage their businesses. Even so, as the conflict drags on, rising oil prices have pushed up Sats&rsquo s input costs, particularly in utilities and energy. Mok says that food costs remain a significant expense driver, especially for the company&rsquo s food solutions business. &ldquo Those costs will start to come in as our contracts with our partners are expiring, and once we negotiate the new contracts, you will start to see those costs coming through.&rdquo Sats CFO Timothy Tang adds that Sats will have to manage these rising cost inputs for as long as the Middle East conflict continues. &ldquo Longer term, this will normalise, and that is where the growth in our network will offset that cost increase. Right now, we need to ensure that we can manage this shock for the short and medium term and use our internal efficiencies to offset the rising cost.&rdquo Meanwhile, Mok believes that there will be a lagging impact from the higher price resulting from the new negotiated contracts, and the company will have to think about how to pass it on to customers. He adds: &ldquo While there is growth in our top line, we cannot allow costs to run ahead too much, and therefore improving productivity and efficiency within our operations will help to offset some of these cost increases.&rdquo Following a results briefing marked by both opportunities and challenges, the key question is whether Sats can sustain its growth trajectory in the coming years amid the ongoing conflict. But for now, Mok is confident that Sats is still on track in achieving its FY2029 targets of more than $8 billion in revenue, 20% or more ebitda margin and above 15% ROE. |

||||

| Useful To Me Not Useful To Me | |||||

|

Delvyss

Elite |

29-May-2026 10:23

|

||||

|

x 0

x 0 Alert Admin |

SATS: Steady As She Cargoes https://sginvestors.io/analysts/research/2026/05/sats-dbs-research-2026-05-28 |

||||

| Useful To Me Not Useful To Me | |||||

|

|

|||||

|

seanpent

Supreme |

29-May-2026 09:24

|

||||

|

x 0

x 0 Alert Admin |

Several bids bought up at one go? | ||||

| Useful To Me Not Useful To Me | |||||

|

seanpent

Supreme |

29-May-2026 09:11

|

||||

|

x 0

x 0 Alert Admin |

$4 will be back soon

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

28-May-2026 23:26

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

The Return of the Prodigal Son - Exponential Recovery with a steep slope, snapping back into the ascending channel.

|

||||

| Useful To Me Not Useful To Me | |||||

|

beng1102

Elite |

28-May-2026 23:01

|

||||

|

x 0

x 0 Alert Admin |

The closing today is even stronger than the previous day. Traded volume surge by 375.61% compares to the average of the last 431 days and price closed even stronger. So still very strong and likely to continue going up.

|

||||

| Useful To Me Not Useful To Me | |||||

|

beng1102

Elite |

28-May-2026 14:38

|

||||

|

x 0

x 0 Alert Admin |

The trading volume surged 340.52% on closing of 26 May 2026 compares to the average of last 430 trading days. Price closed up strongly. This simply show how bullist the buying is.

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

28-May-2026 12:38

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

Add: OCBC - 4.20 Maybank - 4.52

|

||||

| Useful To Me Not Useful To Me | |||||

|

JurongW

Elite |

28-May-2026 12:15

Yells: "Earnings give weight, Chart give wings" |

||||

|

x 0

x 0 Alert Admin |

Price target post result annoucement: DBS - 4.40 CGSI - 4.68 UOBKH- 4.75 |

||||

| Useful To Me Not Useful To Me | |||||

|

beng1102

Elite |

28-May-2026 09:44

|

||||

|

x 0

x 0 Alert Admin |

Easily go back up to above $4.

|

||||

| Useful To Me Not Useful To Me | |||||