|

Back

x 0 x 0

x 0 x 0

|

Turn around or u turn? For one to decide..

Frankie Ho: Bey ong Intel: AEM&rsquo s next chapter is tak ing shape

BY FRANKIE HO frankie.ho@bizedge.com

6 Apr 2026

There was a time when AEM Hold ings could do no wrong. As a key sup plier to Intel&rsquo s eco sys tem, it rode the US chip maker&rsquo s upswing and became one of the mar ket&rsquo s clearest prox ies for backend semi con ductor test demand. The Singa pore-headquartered chip tester&rsquo s annual rev enue more than doubled from $223 mil lion in 2017 to $565 mil lion in 2021. It went on to hit an all-time high of $870 mil lion the fol low ing year. AEM&rsquo s share price surged over those years, mir ror ing its rapid growth.

Then the cycle turned as Intel stumbled. Delays in advan cing man u fac tur ing nodes allowed Intel&rsquo s rivals, such as TSMC, to pull ahead, while exe cu tion mis steps and intensi fy ing com pet i tion eroded its long-held dom in ance in per sonal com puters and data centres. Intel ended up on the back foot just as the semi con ductor industry entered a new phase driven by AI and high-per form ance com put ing.

For AEM, the con sequences were imme di ate. As its largest cus tomer faltered, growth slowed, vis ib il ity weakened and investor con fid ence ebbed. From a high con vic tion growth story, AEM sud denly became a worry for investors, who dumped its shares as they figured the com pany was too closely tied to a single cus tomer whose own tra ject ory had become unpre dict able.

The turn ing point for AEM came only after the release of its 2025 res ults in Feb ru ary this year. Rev enue rose for the first time since 2022, driven by a ramp-up in high-volume man u fac tur ing linked to AI and high-per form ance com put ing demand.

More import antly, the qual ity of earn ings improved. In 2025, AEM returned to pos it ive free cash flow, rebuilt its bal ance sheet into a net cash pos i tion, and rein stated dividends at 1.3 cents per share, equi val ent to about 24% of earn ings &mdash not far off from its min imum 25% pay out pledge.

For this year, AEM is tar get ing rev enue of $460 mil lion to $510 mil lion, up from its actual $399 mil lion top line for 2025. Growth is expec ted to be driven by increased orders from key AI and high-per form ance com put ing cus tom ers, one of which is slated to become its new top rev enue con trib utor in 2026.

Redu cing cus tomer con cen tra tion

Since the release of its 2025 res ults and 2026 rev enue guid ance on Feb 25, AEM&rsquo s share price has more than doubled. Its mar ket cap is now back above $1 bil lion.

While the rally is wel come news for share hold ers who endured AEM&rsquo s down turn in recent years, it also raises deeper ques tions. Is this simply a cyc lical rebound tied to a recov ery in semi con ductor demand? Or is AEM under go ing a more fun da mental shift?

For much of the past dec ade, AEM&rsquo s for tunes rose and fell with Intel. That&rsquo s chan ging, and one of the most vis ible signs of this shift came last month.

AEM announced on March 21 a stra tegic part ner ship with Taiwan-based ASE Tech no logy Hold ing, one of the world&rsquo s largest out sourced semi con ductor assembly and test pro viders. The tie-up includes a $12 mil lion equity invest ment by ASE, along with war rants, that could increase its stake in AEM mean ing fully if cer tain per form ance tar gets are met.

The struc ture of the deal is telling. The war rants are linked to rev enue tar gets tied to ASE, effect ively align ing both parties around growth out comes. This goes bey ond a sup plier rela tion ship. It&rsquo s a stra tegic align ment built around scal ing AEM&rsquo s tech no lo gies across ASE&rsquo s global man u fac tur ing foot print.

ASE sits at a crit ical junc ture in the semi con ductor value chain, bridging chip design and mass pro duc tion through advanced pack aging and high-volume test ing. Integ ra tion into ASE&rsquo s eco sys tem allows AEM to reach a far broader cus tomer base than it could on its own.

Elev at ing Intel ties

While con cerns remain over its heavy reli ance on Intel, AEM is seek ing to take that rela tion ship fur ther. This is evid ent in its col lab or a tion with Intel Foundry, a rel at ively new busi ness unit that marks Intel&rsquo s shift from mak ing chips mainly for itself to man u fac tur ing for other com pan ies.

The tim ing is not able. Intel is no longer deteri or at ing as rap idly as before. The chip maker has embarked on an aggress ive effort to regain com pet it ive ness, invest ing heav ily in advanced man u fac tur ing, attempt ing to close the gap with TSMC, and repos i tion ing itself in AI and foundry ser vices. Intel&rsquo s turn around remains a work in pro gress, but the tra ject ory has shif ted from decline to sta bil isa tion.

For AEM, that dis tinc tion is crit ical. It doesn&rsquo t need Intel to return to dom in ance. It only needs the situ ation to stop worsen ing.

Against this back drop, its col lab or a tion with Intel Foundry, announced in May last year, opens up AEM&rsquo s pro duc tion-proven test infra struc ture to fab less chip design ers and other cus tom ers within the foundry&rsquo s net work.

The bene fits are clear. For cus tom ers, it provides access to a scal able, high-volume test envir on ment without hav ing to build it from scratch. This shortens time-to-mar ket and lowers cap ital expendit ure. For AEM, Intel Foundry offers dir ect access to new cus tom ers, expands its address able mar ket and reduces the fric tion of cus tomer acquis i tion.

All about AI

At the heart of AEM&rsquo s repos i tion ing is a simple real ity: AI is chan ging the nature of semi con ductor demand. The shift isn&rsquo t just about more chips. It&rsquo s about dif fer ent chips.

AI work loads require higher per form ance, greater power dens ity and more com plex archi tec tures. These devel op ments place increas ing strain on test ing pro cesses, which must ensure reli ab il ity under real-world oper at ing con di tions.

AEM&rsquo s tech no lo gies are built for such demands. They&rsquo re meant to handle high-power chips, lar ger designs and com plex heat con di tions, all of which are increas ingly com mon in AI and high-per form ance com put ing. In that sense, AEM isn&rsquo t just bene fit ing from the AI cycle. It&rsquo s posi tioned within one of AI&rsquo s key enabling lay ers.

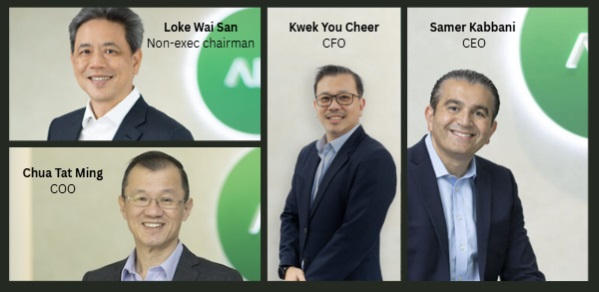

That pos i tion ing is already trans lat ing into trac tion. Since tak ing over last July, CEO Samer Kab bani has expan ded AEM&rsquo s tech no logy roadmap and strengthened its thermal cap ab il it ies, help ing the com pany win cus tom ers across AI, high-per form ance com put ing, memory and hyper scaler seg ments.

The lead er ship change itself was abrupt. Amy Leong stepped down as CEO last July after just over a year in the role, in what AEM described as a &ldquo board-led lead er ship realign ment for growth&rdquo .

The change at the top was more than cos metic. Kab bani, who joined AEM in 2020, had been closely involved in shap ing the com pany&rsquo s next-gen er a tion test tech no logy roadmap and expand ing its intel lec tual prop erty, par tic u larly in advanced thermal con trol, as chips become more power ful and gen er ate more heat.

In effect, AEM&rsquo s board was elev at ing a tech no lo gist at a time when the industry was mov ing in the same dir ec tion. As semi con ductor design shifts towards more com plex, per form ance-driven applic a tions, the import ance of test ing &mdash and the tech no lo gies that under pin it &mdash rises in tan dem.

But whether that pos i tion ing is fully under stood or appre ci ated is an open ques tion. Much of the mar ket&rsquo s atten tion remains focused on chip design ers and man u fac tur ers, the com pan ies at the front end of the value chain.

Test ing, by con trast, is often seen as a sec ond ary activ ity, even though it&rsquo s increas ingly crit ical as com plex ity increases.

Rais ing the bar

Des pite its pro gress, AEM&rsquo s trans form a tion is not without risks. Diver si fy ing a cus tomer base isn&rsquo t a one-off event. The trans ition from a single-anchor model to a multi-cus tomer plat form comes with com plex it ies. These include greater coordin a tion, deeper engin eer ing cap ab il it ies and a more scal able oper at ing model.

There&rsquo s also the ques tion of sus tain ab il ity. Mar gins, for one, remain below his tor ical highs. That sug gests AEM&rsquo s recov ery is still in its early stages. The com pany&rsquo s oper at ing profit mar gin for 2022, when rev enue reached an all-time high, was 18.4%. Last year&rsquo s mar gin was 5.5%.

It also sug gests that while AEM has sta bil ised, it hasn&rsquo t fully regained its former earn ings power. The rebound in rev enue and cash flow in 2025 is encour aging, but it doesn&rsquo t, on its own, sig nal a com plete turn around.

The mar ket, however, appears to be look ing ahead. The sharp re-rat ing in AEM&rsquo s share price in recent weeks sug gests investors may be expect ing something more than a cyc lical recov ery.

The ques tion now is whether AEM can evolve from a com pany defined by a single cus tomer into one posi tioned across a broader, struc tur ally grow ing seg ment of the semi con ductor industry.

The early signs are there. AEM&rsquo s expos ure to AI and high-per form ance com put ing is deep en ing. Its part ner ships, with ASE on one hand and Intel Foundry on the other, are expand ing its reach bey ond tra di tional bound ar ies. Its solu tions are also increas ingly rel ev ant as chip designs grow more com plex and test ing becomes more crit ical.

The next phase will depend less on nar rat ive and more on exe cu tion. AEM will need to con vert part ner ships into rev enue, show that new cus tom ers can scale mean ing fully, and rebuild mar gins closer to his tor ical levels. It will also need to show that its diver si fic a tion efforts can off set the inher ent cyc lic al ity of the semi con ductor industry.

In that sense, the bar has been raised. AEM is no longer being judged on whether it can recover from its down turn. It&rsquo s being assessed on whether it can sus tain a new phase of growth, one that&rsquo s less depend ent on any single cus tomer and more anchored to broader industry trends.

The dis tinc tion is import ant. Recov ery is cyc lical, while rein ven tion is struc tural. AEM has made mean ing ful pro gress on the former. Whether it can achieve the lat ter will determ ine if its recent rally marks the start of a new chapter or simply another turn in the cycle.

JurongW ( Date: 08-Apr-2026 16:39) Posted:

RL - Guess u have run far away by now. Any plans to u-turn back ?

ruanlai ( Date: 07-Apr-2026 10:08) Posted:

No volume for the 3 musketeers (A F U) to run road

Sellers / shortlist will deep dive all the way down few pips.

Doom day at noon said trump.

Good luck and DYODD |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Will this prove to be a Win-Win Partnership now that Intel is going to supply chips to Tesla and will AEM benefit and by how much?

General Announcement: AEM Receives Intel EPIC Supplier Award

AEM Receives Intel EPIC Supplier Award

Singapore, 19 March 2026 &ndash AEM Holdings Ltd. (&ldquo AEM&rdquo or &ldquo the Group&rdquo ), a global leader in test innovation, today announced that it has received the 2026 Intel EPIC Supplier Award, the highest supplier recognition from Intel for its performance, innovation, and collaboration within Intel&rsquo s global supply chain.

The Intel EPIC Supplier Award recognizes top-performing suppliers that demonstrate excellence in quality, technology innovation, operational performance, and continuous improvement. Among thousands of companies across Intel&rsquo s global network, only 41 suppliers were selected to receive the EPIC Supplier Award for achieving the highest standards of execution and strategic partnership. EPIC represents Intel&rsquo s core supplier performance pillars of Excellence, Partnership, Inclusion, and Continuous Improvement.

This recognition reflects AEM&rsquo s commitment to engineering innovation, operational reliability, and close collaboration with its customers. It further reinforces the Group&rsquo s position as a trusted partner to leading semiconductor manufacturers and highlights its ability to deliver high-performance solutions that enable the production of advanced semiconductor devices.

Samer Kabbani, Chief Executive Officer of AEM, said, &ldquo We are deeply honored to receive the Intel EPIC Supplier Award in recognition of AEM&rsquo s outstanding performance in 2025. I am incredibly proud of our global team, whose passion, innovation, and execution made this achievement possible. As artificial intelligence accelerates a generational leap in semiconductor performance, test architectures, power density, and thermal technologies are now foundational enablers of next-generation computing. We look forward to further expanding our partnership with Intel and IFS as we advance the future of AI-driven silicon.&rdquo

Read the full announcement: http://ms.spr.ly/6045QUn2f

tongphlp ( Date: 09-Apr-2026 08:45) Posted:

haha....can it fly to the moon instead? Let' s aim for 8.64 instead!

11:10 AM PDT · April 7, 2026

Image Credits:Intel(opens in a new window)

Intel signs on to Elon Musk&rsquo s Terafab chips project

Intel will join SpaceX and Tesla in an effort to build a new U.S. semiconductor factory in Texas, although the scope of its contributions are unclear.

&ldquo Our ability to design, fabricate, and package ultra-high-performance chips at scale will help accelerate Terafab&rsquo s aim to produce 1 TW/year of compute to power future advances in AI and robotics,&rdquo Intel said in a corporate post on X. Intel hasn&rsquo t shared any more information.

Elon Musk announced in March a team-up between the two tech companies he leads to develop chips for AI compute, satellites, and SpaceX&rsquo s mooted space data center and to support the possibility of autonomous Tesla vehicles and robots.

However, building a chip fab is one of the most difficult and expensive corporate infrastructure projects out there, typically requiring years of time and more than $20 billion to create a facility with a huge clean room for thousands of ultra-precise machines to carve silicon. It wasn&rsquo t obvious how SpaceX and Tesla, two companies with no experience in the sector, could team up to execute the project efficiently.

Now we have a better idea: Intel will do it. The company has been hunting for large anchor customers to support its foundry business, and now it has two. Still, if investors thought that Terafab would be a greenfield approach based on SpaceX&rsquo s and Tesla&rsquo s unique approach to engineering, that may not play out.

Once the leading U.S. silicon producer, Intel has seen rivals Nvidia and AMD take the lead in developing advanced processors and adopt the &ldquo fabless&rdquo business model where chip designers outsource the manufacturing of their semiconductors. Intel&rsquo s stock rose more than 3% on the news today. It was trading at $52.28, about 2.9% higher than its opening bell price, at 2 p.m. ET.

Intel declined to comment on the partnership, while SpaceX didn&rsquo t respond to TechCrunch&rsquo s query.

JurongW ( Date: 08-Apr-2026 16:37) Posted:

Thanks to POTUS for giving Iran a lifeline of 2 weeks, AEM is likely on its way to test the previous high of 4.68

Well done to AEM shareholders who have not sold this stock. |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

haha....can it fly to the moon instead? Let' s aim for 8.64 instead!

11:10 AM PDT · April 7, 2026

Image Credits:Intel(opens in a new window)

Intel signs on to Elon Musk&rsquo s Terafab chips project

Intel will join SpaceX and Tesla in an effort to build a new U.S. semiconductor factory in Texas, although the scope of its contributions are unclear.

&ldquo Our ability to design, fabricate, and package ultra-high-performance chips at scale will help accelerate Terafab&rsquo s aim to produce 1 TW/year of compute to power future advances in AI and robotics,&rdquo Intel said in a corporate post on X. Intel hasn&rsquo t shared any more information.

Elon Musk announced in March a team-up between the two tech companies he leads to develop chips for AI compute, satellites, and SpaceX&rsquo s mooted space data center and to support the possibility of autonomous Tesla vehicles and robots.

However, building a chip fab is one of the most difficult and expensive corporate infrastructure projects out there, typically requiring years of time and more than $20 billion to create a facility with a huge clean room for thousands of ultra-precise machines to carve silicon. It wasn&rsquo t obvious how SpaceX and Tesla, two companies with no experience in the sector, could team up to execute the project efficiently.

Now we have a better idea: Intel will do it. The company has been hunting for large anchor customers to support its foundry business, and now it has two. Still, if investors thought that Terafab would be a greenfield approach based on SpaceX&rsquo s and Tesla&rsquo s unique approach to engineering, that may not play out.

Once the leading U.S. silicon producer, Intel has seen rivals Nvidia and AMD take the lead in developing advanced processors and adopt the &ldquo fabless&rdquo business model where chip designers outsource the manufacturing of their semiconductors. Intel&rsquo s stock rose more than 3% on the news today. It was trading at $52.28, about 2.9% higher than its opening bell price, at 2 p.m. ET.

Intel declined to comment on the partnership, while SpaceX didn&rsquo t respond to TechCrunch&rsquo s query.

JurongW ( Date: 08-Apr-2026 16:37) Posted:

Thanks to POTUS for giving Iran a lifeline of 2 weeks, AEM is likely on its way to test the previous high of 4.68

Well done to AEM shareholders who have not sold this stock.

JurongW ( Date: 07-Apr-2026 13:57) Posted:

Consolidating and moving sideways between 4.10 and 4.38 in the interim.

Hard to call - Price could go either way.

|

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Leong Chan Teik

05 April 2026

AEM Holdings, a key player in semiconductor testing equipment, recently went on a non-deal roadshow in Kuala Lumpur, meeting 12 funds, according to a DBS Research report.

The report provides a comprehensive investment analysis of AEM, highlighting the company&rsquo s technological advantages, particularly its high-parallel and thermal management capabilities essential for AI and high-power chip testing. The report provides a comprehensive investment analysis of AEM, highlighting the company&rsquo s technological advantages, particularly its high-parallel and thermal management capabilities essential for AI and high-power chip testing.

Authored by analyst Amanda Tan, it shares insights into a new strategic partnership and provides reassuring updates on ongoing litigation.

AEM stock has gained a massive ~140% year-to-date (from $1.74 to $4.16). |

The Big Catalyst: The AEM and ASE Partnership

AEM has teamed up with ASE, which DBS is calling a strategic " win-win" partnership.

To understand why this is such a big deal, look at OSATs (Outsourced Semiconductor Assembly and Test).

OSATs are massive third-party facilities that chip designers hire to assemble and test their chips before they hit the market.

By partnering with ASE&mdash a giant in the OSAT space&mdash AEM is tapping into a massive network.

As the DBS report notes, " Partnering with ASE allows AEM to tap into a large outsourced testing network serving multiple chipmakers and hyperscalers, significantly widening its addressable market beyond its direct customers" .

Why did ASE approach AEM? The world is facing urgent AI testing capacity constraints.

Traditional testing is slow and takes up too much factory floor space.

AEM, however, specializes in high-parallel systems. This means their advanced machines can test dozens of individual devices simultaneously.

According to DBS, " AEM&rsquo s high-parallel systems enable testing of dozens of devices simultaneously, improving throughput and increasing productivity per square foot, a key constraint in high-density manufacturing hubs like Taiwan" .

Furthermore, " ASE approached AEM to deliver differentiated testing capabilities after limited progress with incumbents, reflecting strong demand for more efficient test solutions in AI-driven workloads" .

Financially, this creates excellent operating leverage, meaning that as AEM sells more equipment and volumes increase, their fixed costs are absorbed better.

The research note explains: " OSAT customers typically scale capacity alongside customer ramps, which can drive repeat orders and higher utilisation for AEM&rsquo s installed base. As volumes increase, fixed cost absorption improves, supporting margin expansion" .

What About the Patent Dispute?

If you heard the news about AEM' s patent dispute announced in October 2025, relax. This situation is very different from their earlier 2022/2023 legal issues.

The current dispute focuses heavily on wafer-level testing. In chipmaking, a " wafer" is the large, pizza-like silicon disc containing hundreds of chips before they are sliced apart.

DBS points out: " Latest issue relates to wafer-level testing outside AEM&rsquo s core focus. AEM primarily operates in packaged testing rather than wafer-level testing, limiting direct exposure to the disputed technology area" .

The takeaway here? " Financial impact expected to be limited. Legal and professional costs were incurred but are not expected to materially affect profitability or operational performance" .

-- DBS Research |

Moreover, " customer demand remains unaffected. Customers continue to prioritise product performance and testing capability, with no evidence of programme delays or order cancellations linked to the case" .

In the tech world, disputes like this are common and do not alter a company' s competitive edge.

DBS sees multiple tailwinds pushing AEM forward.

The report states: " Overall, with multiple tailwinds including constrained CPU-driven demand from its long-standing HPC customer, growing contributions from new customers, and the emerging ASE partnership catalyst, we see increasing confidence that AEM can meet or potentially exceed FY26 guidance, particularly as current guidance does not explicitly factor in contributions from the ASE&ndash AEM partnership" .

In fact, AEM' s revenue mix is shifting favorably.

DBS highlights: " Our assumptions imply a revenue mix shift towards new customers, with contributions of c.44% from new customers, 30% from CEI, and 26% from Intel in FY26, rising to 51%, 27%, and 22% respectively in FY27" .

Because of this, DBS has increasing confidence in AEM' s future profitability.

" In addition to a more favourable mix, this could also unlock operating leverage, providing further upside to our margin and earnings assumptions (8-13% below FY26/27 consensus estimates). We currently have a BUY call with TP SGD4.60" .

|

|

Good Post

Bad Post

|

x 0

x 0

|

shorters in abundance..

tongphlp ( Date: 02-Apr-2026 10:09) Posted:

always a pleasure to shot this

manipulation at its best |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

majority think so too...people are trying to kick him out of office

wavehunter ( Date: 07-Apr-2026 16:51) Posted:

I lost count how many times he extended the deadline for Iran to reopen the Straits of Hormuz.

So many times that Iran is already numb to his threat and treats him like a mad dog who only barks but has no bite.

So most likely he will TACO again - Trump Always Chicken Out. And say " talks are going very well. Iran wants to make

a deal. They are begging us to make a deal. They are saying they will do anything...anything at all....to just make a deal.

They are kissing my ass."

Shake head man.

He will go down in history as the worst US president the world has ever seen.

There wont be anyone worse than that.

This is a record that Trump will hold forever. Forever.

spore1 ( Date: 07-Apr-2026 16:04) Posted:

| We will know tmr whether any further escalations of the war. |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

all bodes well for Wilmar

Rightstock ( Date: 30-Mar-2026 10:40) Posted:

Now there is a shortage of oil and prices have gone up.

In the weeks ahead there will also shortage of sugar, palm oil and cooking oil.

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

companies doing SBB in Q1 2026

| Share Buybacks by Primary-listed Companies by way of Market Acquisition (1Q26) with total consideration > S$100,000 |

Number of Shares/Units Purchased |

Buyback Consideration (incl stamp duties & clearing charges) S$ |

Avg price paid per share S$ |

| SINGAPORE TELECOMMUNICATIONS |

24,884,803 |

123,068,686 |

$4.95 |

| OVERSEA-CHINESE BANKING CORPORATION |

5,400,000 |

115,697,899 |

$21.43 |

| KEPPEL |

7,695,400 |

94,473,057 |

$12.28 |

| UNITED OVERSEAS BANK |

1,590,000 |

57,940,550 |

$36.44 |

| SINGAPORE TECHNOLOGIES ENGINEERING |

4,750,000 |

48,268,753 |

$10.16 |

| SATS |

9,554,200 |

34,968,032 |

$3.66 |

| SINGAPORE AIRLINES |

3,000,000 |

20,240,960 |

$6.75 |

| SINGAPORE EXCHANGE |

950,000 |

16,779,424 |

$17.66 |

| SEATRIUM |

4,220,000 |

9,909,591 |

$2.35 |

| THE HOUR GLASS |

3,312,800 |

7,487,408 |

$2.26 |

| HONG FOK CORPORATION |

5,346,700 |

4,532,324 |

$0.85 |

| VENTURE CORPORATION |

257,200 |

4,009,280 |

$15.59 |

| GENTING SINGAPORE |

5,400,000 |

3,632,514 |

$0.67 |

| CHUAN HUP HOLDINGS |

11,527,200 |

2,703,034 |

$0.23 |

| HONG LAI HUAT GROUP |

25,645,300 |

2,171,425 |

$0.08 |

| FIRST RESOURCES |

1,017,600 |

2,009,292 |

$1.97 |

| FOOD EMPIRE HOLDINGS |

644,700 |

1,654,700 |

$2.57 |

| A-SONIC AEROSPACE |

2,740,600 |

1,411,819 |

$0.52 |

| FRASER AND NEAVE |

865,200 |

1,250,435 |

$1.45 |

| GLOBAL INVESTMENTS |

6,745,900 |

863,142 |

$0.13 |

| COMFORTDELGRO CORPORATION |

501,400 |

726,948 |

$1.45 |

| HOCK LIAN SENG HOLDINGS |

1,660,500 |

691,612 |

$0.42 |

| KINGSMEN CREATIVES |

1,300,700 |

666,900 |

$0.51 |

| KIMLY |

1,371,400 |

538,682 |

$0.39 |

| 17LIVE GROUP |

460,000 |

505,978 |

$1.10 |

| PAN-UNITED CORPORATION |

330,000 |

451,842 |

$1.37 |

| ATTIKA GROUP |

1,123,700 |

439,246 |

$0.39 |

| VIBRANT GROUP |

2,500,000 |

389,736 |

$0.16 |

| INTRACO |

792,100 |

299,814 |

$0.38 |

| SIA ENGINEERING COMPANY |

83,600 |

259,429 |

$3.10 |

| KARIN TECHNOLOGY HLDGS |

876,500 |

233,676 |

$0.27 |

| OXLEY HOLDINGS |

1,592,600 |

129,661 |

$0.08 |

| CREDIT BUREAU ASIA |

89,700 |

113,170 |

$1.26 |

| TREK 2000 INTERNATIONAL |

995,400 |

101,708 |

$0.10 |

|

|

Good Post

Bad Post

|

x 0

x 0

|

on the contrary, it should be rising very soon

pnuklis ( Date: 07-Apr-2026 11:59) Posted:

Shorters are all over will drag it below 4

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Crippled or disbabled how? Must be inclusive - said our PM

JurongW ( Date: 06-Apr-2026 14:52) Posted:

Thanks for the timely reminder. I believe TP hears u loud and clear

ruanlai ( Date: 06-Apr-2026 14:39) Posted:

Run before you regret!

Dyodd |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

don' t trust DT, trust TV

patterns don' t lie..

JurongW ( Date: 06-Apr-2026 13:54) Posted:

tongphlp ( Date: 06-Apr-2026 13:35) Posted:

ruanlai, dun raun lai and create panic

unless u r D |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Dependent on :

1) DT

2) Nasdaq futures trend

3) Institutions who may still be on easter break

JurongW ( Date: 06-Apr-2026 13:51) Posted:

No sign of trend reversal yet.

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Look at ST Engr. Coming up fast and furious.

Venture? Going down the slippery slope. Strategic? Stupid!

tongphlp ( Date: 06-Apr-2026 13:40) Posted:

Vote for change of mgmt! Things only can get better.

Notice Of Annual General Meeting

| Announcement Title |

Annual General Meeting |

| Date & Time of Broadcast |

Apr 2, 2026 7:03 |

| Status |

New |

| Announcement Reference |

SG260402MEETQ85P |

| Submitted By (Co./ Ind. Name) |

Juliana Zhang |

| Designation |

Company Secretary |

| Financial Year End |

31/12/2025 |

| Event Narrative |

| Narrative Type |

Narrative Text |

| Additional Text |

Please refer to the following attachments:

1. Notice of Annual General Meeting

2. Proxy Form

3. Letter to Shareholders in relation to the Proposed Renewal of the Share Purchase Mandate |

| Event Dates |

| Meeting Date and Time |

24/04/2026 10:30:00 |

| Response Deadline Date |

21/04/2026 10:30:00 |

| Event Venue(s) |

| Place |

| Venue(s) |

Venue details |

| |

|

| Meeting Venue |

5006 Ang Mo Kio Avenue 5

#05-01, TECHplace II

Singapore 569873 |

Attachments

- Notice Of AGM (Size: 200,179 bytes)

- Proxy Form (Size: 62,704 bytes)

tongphlp ( Date: 02-Apr-2026 10:37) Posted:

let' s show the big guys how to shoot Venture down

ready. set. fire |

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

Vote for change of mgmt! Things only can get better.

Notice Of Annual General Meeting

| Announcement Title |

Annual General Meeting |

| Date & Time of Broadcast |

Apr 2, 2026 7:03 |

| Status |

New |

| Announcement Reference |

SG260402MEETQ85P |

| Submitted By (Co./ Ind. Name) |

Juliana Zhang |

| Designation |

Company Secretary |

| Financial Year End |

31/12/2025 |

| Event Narrative |

| Narrative Type |

Narrative Text |

| Additional Text |

Please refer to the following attachments:

1. Notice of Annual General Meeting

2. Proxy Form

3. Letter to Shareholders in relation to the Proposed Renewal of the Share Purchase Mandate |

| Event Dates |

| Meeting Date and Time |

24/04/2026 10:30:00 |

| Response Deadline Date |

21/04/2026 10:30:00 |

| Event Venue(s) |

| Place |

| Venue(s) |

Venue details |

| |

|

| Meeting Venue |

5006 Ang Mo Kio Avenue 5

#05-01, TECHplace II

Singapore 569873 |

Attachments

- Notice Of AGM (Size: 200,179 bytes)

- Proxy Form (Size: 62,704 bytes)

tongphlp ( Date: 02-Apr-2026 10:37) Posted:

let' s show the big guys how to shoot Venture down

ready. set. fire.

tongphlp ( Date: 30-Mar-2026 11:19) Posted:

has been 22 yrs....shd V reconsider to sell and create better and more attractive returns?

Singapore' s Venture Shows The Big Guys Another Way

The backup-drive manufacturer has margins that fill its huge rivals with envy

July 26, 2004 at 12:00 PM GMT+8

This article is for subscribers only.

At the height of the tech boom, emissaries from Flextronics, Solectron, Celestica, and other contract manufacturing giants were knocking on Wong Ngit Liong' s door, offering him enticing sums for his company, Venture Corp. The Singapore manufacturer enjoyed a solid reputation as the maker of Iomega Zip backup drives, Hewlett-Packard printers, and Agilent Technologies' testing and measurement gear. Wong watched as Singapore' s other contract manufacturers -- NatSteel Electronics, JIT Holdings, Li Xin Industries, and Omni Industries -- were acquired, one by one. But he rebuffed the offers. " The valuations were very tempting," recalls Wong, Venture' s CEO. " But we knew we could create more value for our stakeholders as an independent entity than as part of some global giant."

Wong' s stubbornness has paid off. Although his company remains far smaller than those that gobbled up his local rivals, Venture has been growing fast and enjoys margins of 7.6% -- the best in the business. Last year, Venture reported earnings of $140 million on sales of $1.85 billion, and analysts forecast a 25% increase in earnings this year. Today, Venture has 10,000 employees in 23 plants worldwide. And the company is rolling in cash: It has $500 million, and J.P. Morgan Chase & Co. expects that to grow to $800 million by the end of next year -- enough to make Venture a predator itself. But that' s not what Wong, a 61-year-old former HP manager, has in mind. " We don' t want to be the world' s biggest contract manufacturer," he says. " We just want to be the most profitable."

SHAREHOLDER CARE

While the biggest names in the business went on a three-year acquisition spree from 1999-2001, Wong focused on earnings. What sets Venture apart is its diverse, low-volume product mix, which allows the company to design most of the products it manufactures -- and charge higher prices. So, instead of simply churning out cell phones that offer margins of 2% to 3%, Wong won contracts to design and manufacture high-end office printers for the likes of HP at margins as high as 10%. Also, by eschewing takeovers, Venture has avoided the costly headaches of integrating the operations of acquired companies. " Wong is the Warren Buffett of contract manufacturing," says Russell Tan, an analyst at NRA Capital in Singapore. " He only cares about extracting the greatest value for his shareholders."

Get the Singapore Edition newsletter in your inbox.

Go beyond the headlines with insights into one of Asia' s most dynamic economies. Delivered weekly.

Wong has also been successful in diversifying Venture' s product line. That, he says, will provide a cushion when tech inevitably heads south again. Sales of printing and imaging equipment today make up 37% of Venture' s total sales, a proportion that is decreasing as Venture brings more products into the mix. The new products in the lineup include networking and communications gear, auto electronics, and medical equipment. Sales of those products could grow by more than 50% this year and next, according to J.P. Morgan. And Agilent is stepping up purchases of testing and measurement equipment.

Wong' s biggest challenge is expanding Venture' s footprint in China. In a country that accounts for one-third of Flextronics' global production, Venture' s three China factories make up just 5% of its capacity. But as his China order book grows, he plans to expand those plants and increase their production from $70 million last year to $1.2 billion by 2008. " The opportunity for us in China is tremendous, given the pipeline of existing and prospective customers," says Wong.

He might even find a way to spend some of that cash he has been building up -- for example, as a venture capital partner in startups that have innovative products. That way, as those companies expand, Venture will not only grow as a supplier but also will reap benefits as a shareholder. " Whatever we do, we' ll be very careful in how much we invest and where," he says. As always, Wong Ngit Liong plans to proceed with caution -- and profit.

By Assif Shameen in Singapore

|

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

ruanlai, dun raun lai and create panic

unless u r DT

ruanlai ( Date: 06-Apr-2026 13:29) Posted:

$4.32 uTurn now.

Pump and dump.

Tmr 12nn Iran hell day.

Oil will over 150.

Run road now, DYODD |

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

caveat: provided Trump keep his foul mouth shut.

tongphlp ( Date: 06-Apr-2026 12:14) Posted:

price movement seems +ve.

Should see upward movement for the later half. DYODD

JurongW ( Date: 05-Apr-2026 16:13) Posted:

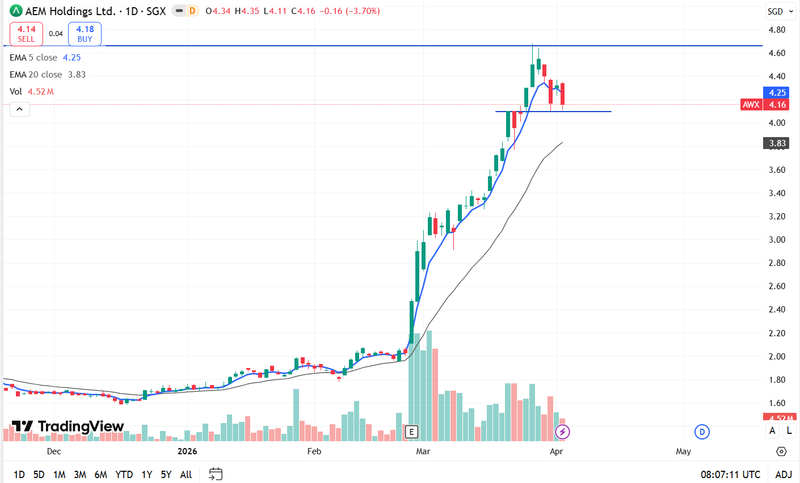

AEM is now pressing against its 4.10 keel, hold steady here and the sails may catch wind back to 4.60 break below, and the tide could drag toward 3.83

📊 Refined Analysis

- Support Anchor: The key support is now 4.10. Price closed at 4.16, so it&rsquo s hovering just above this line.

- Short-Term Bias: EMA 5 (4.25) is above EMA 20 (3.83), still showing a bullish structure, but price dipping below EMA 5 signals near-term weakness.

- Volume Context: 4.52M traded, showing strong activity during the pullback &mdash not a quiet drift, but active selling pressure.

⚖ ️ Scenario Mapping

- Bullish Pathway:

- If 4.10 holds, price could rebound toward 4.25&ndash 4.60.

- A bounce here would confirm 4.10 as a strong support zone.

- Bearish Pathway:

- A decisive break below 4.10 opens the door to 4.00 and then 3.83 (EMA 20).

- Sustained bearish sentiment after ex-dividend could accelerate this move.

✨ Interpretation

- The market is testing a critical anchor at 4.10.

- Holding above it keeps the bullish channel intact slipping below signals a deeper correction.

- Traders will be watching for confirmation candles around this level &mdash whether it stabilizes or cracks.

|

|

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

price movement seems +ve.

Should see upward movement for the later half. DYODD

JurongW ( Date: 05-Apr-2026 16:13) Posted:

AEM is now pressing against its 4.10 keel, hold steady here and the sails may catch wind back to 4.60 break below, and the tide could drag toward 3.83

📊 Refined Analysis

- Support Anchor: The key support is now 4.10. Price closed at 4.16, so it&rsquo s hovering just above this line.

- Short-Term Bias: EMA 5 (4.25) is above EMA 20 (3.83), still showing a bullish structure, but price dipping below EMA 5 signals near-term weakness.

- Volume Context: 4.52M traded, showing strong activity during the pullback &mdash not a quiet drift, but active selling pressure.

⚖ ️ Scenario Mapping

- Bullish Pathway:

- If 4.10 holds, price could rebound toward 4.25&ndash 4.60.

- A bounce here would confirm 4.10 as a strong support zone.

- Bearish Pathway:

- A decisive break below 4.10 opens the door to 4.00 and then 3.83 (EMA 20).

- Sustained bearish sentiment after ex-dividend could accelerate this move.

✨ Interpretation

- The market is testing a critical anchor at 4.10.

- Holding above it keeps the bullish channel intact slipping below signals a deeper correction.

- Traders will be watching for confirmation candles around this level &mdash whether it stabilizes or cracks.

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

writing has been on the wall...

playing for time

Joelton ( Date: 02-Apr-2026 08:03) Posted:

mm2 Asia proposed $15 mil share placement agreement with UOB Kay Hian lapses

Media entertainment and content company mm2 Asia says it has let a proposed placement of $15 million with UOB Kay Hian lapse after the terms of the placement agreement were not satisfied.

According to a filing made by mm2 Asia on April 1, the lapse and termination of the agreement is not expected to have a material adverse impact on the company&rsquo s consolidated net tangible assets per share and earnings per share for the financial year ending March 31, 2027.

mm2 Asia first entered into the agreement with its placement agent UOB Kay Hian on July 4, 2025. The placement round would have seen mm2 Asia issue 1.875 billion shares at 0.8 cents apiece. If successful, the placement shares would have made up 22.3% of the company&rsquo s enlarged issued and paid-up share capital.

In an earlier filing on Oct 3, mm2 Asia said it had extended the placement agreement&rsquo s cut-off date by six months to March 31 from Sep 30.

The placement agreement would have offered a lifeline to the cash-strapped company which has received multiple letters of demand for payment over the past few months. After deducting the placement fees, mm2 Asia planned to use $7.5 million of the proceeds to repay its debts and liabilities, and the remaining $6.5 million to finance general capital working purposes.

On March 9, mm2 Asia announced that it was pursuing a separate $15 million placement arrangement with Hildrics Asia Growth Fund VCC. As part of the deal, mm2 Asia will also be raising $10 million from existing shareholders via a rights issue. The VCC belongs to Hildrics Capital, an existing investor in businesses related to mm2 Asia.

mm2 Asia suspended trading of its shares on Nov 11 after its board assessed that it could not prove that it is able to continue as a going concern. Its shares last traded at 0.3 cents on Nov 10.

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

let' s show the big guys how to shoot Venture down

ready. set. fire.

tongphlp ( Date: 30-Mar-2026 11:19) Posted:

has been 22 yrs....shd V reconsider to sell and create better and more attractive returns?

Singapore' s Venture Shows The Big Guys Another Way

The backup-drive manufacturer has margins that fill its huge rivals with envy

July 26, 2004 at 12:00 PM GMT+8

This article is for subscribers only.

At the height of the tech boom, emissaries from Flextronics, Solectron, Celestica, and other contract manufacturing giants were knocking on Wong Ngit Liong' s door, offering him enticing sums for his company, Venture Corp. The Singapore manufacturer enjoyed a solid reputation as the maker of Iomega Zip backup drives, Hewlett-Packard printers, and Agilent Technologies' testing and measurement gear. Wong watched as Singapore' s other contract manufacturers -- NatSteel Electronics, JIT Holdings, Li Xin Industries, and Omni Industries -- were acquired, one by one. But he rebuffed the offers. " The valuations were very tempting," recalls Wong, Venture' s CEO. " But we knew we could create more value for our stakeholders as an independent entity than as part of some global giant."

Wong' s stubbornness has paid off. Although his company remains far smaller than those that gobbled up his local rivals, Venture has been growing fast and enjoys margins of 7.6% -- the best in the business. Last year, Venture reported earnings of $140 million on sales of $1.85 billion, and analysts forecast a 25% increase in earnings this year. Today, Venture has 10,000 employees in 23 plants worldwide. And the company is rolling in cash: It has $500 million, and J.P. Morgan Chase & Co. expects that to grow to $800 million by the end of next year -- enough to make Venture a predator itself. But that' s not what Wong, a 61-year-old former HP manager, has in mind. " We don' t want to be the world' s biggest contract manufacturer," he says. " We just want to be the most profitable."

SHAREHOLDER CARE

While the biggest names in the business went on a three-year acquisition spree from 1999-2001, Wong focused on earnings. What sets Venture apart is its diverse, low-volume product mix, which allows the company to design most of the products it manufactures -- and charge higher prices. So, instead of simply churning out cell phones that offer margins of 2% to 3%, Wong won contracts to design and manufacture high-end office printers for the likes of HP at margins as high as 10%. Also, by eschewing takeovers, Venture has avoided the costly headaches of integrating the operations of acquired companies. " Wong is the Warren Buffett of contract manufacturing," says Russell Tan, an analyst at NRA Capital in Singapore. " He only cares about extracting the greatest value for his shareholders."

Get the Singapore Edition newsletter in your inbox.

Go beyond the headlines with insights into one of Asia' s most dynamic economies. Delivered weekly.

Wong has also been successful in diversifying Venture' s product line. That, he says, will provide a cushion when tech inevitably heads south again. Sales of printing and imaging equipment today make up 37% of Venture' s total sales, a proportion that is decreasing as Venture brings more products into the mix. The new products in the lineup include networking and communications gear, auto electronics, and medical equipment. Sales of those products could grow by more than 50% this year and next, according to J.P. Morgan. And Agilent is stepping up purchases of testing and measurement equipment.

Wong' s biggest challenge is expanding Venture' s footprint in China. In a country that accounts for one-third of Flextronics' global production, Venture' s three China factories make up just 5% of its capacity. But as his China order book grows, he plans to expand those plants and increase their production from $70 million last year to $1.2 billion by 2008. " The opportunity for us in China is tremendous, given the pipeline of existing and prospective customers," says Wong.

He might even find a way to spend some of that cash he has been building up -- for example, as a venture capital partner in startups that have innovative products. That way, as those companies expand, Venture will not only grow as a supplier but also will reap benefits as a shareholder. " Whatever we do, we' ll be very careful in how much we invest and where," he says. As always, Wong Ngit Liong plans to proceed with caution -- and profit.

By Assif Shameen in Singapore

|

|

|

|

Good Post

Bad Post

|

x 0

x 0

|

send in the undertakers

Joelton ( Date: 02-Apr-2026 08:04) Posted:

Cathay Cineplexes operator mm2 Asia&rsquo s 1.9-billion share lifeline dead in the water

The placement was meant to raise S$14 million for debt repayment and other uses

[SINGAPORE] A S$14 million fundraising plan by beleaguered Cathay Cineplexes operator mm2 Asia : 1B0 0% to raise monies for debt repayment through a placement of some 1.9 billion shares has fallen through, the entertainment company said on Wednesday (Apr 1).

The placement agreement, which aimed to offer shares at a minimum of S$0.008 apiece, &ldquo has lapsed and terminated and is of no further effect&rdquo , mm2 Asia said. This is because conditions under the agreement were not satisfied by the extended cut-off date of Tuesday.

mm2 Asia does not expect the lapse and termination of the placement agreement to have material adverse impact on its consolidated net tangible assets per share and earnings per share for the financial year ending Mar 31, 2027.

This comes as the company on Mar 9 announced a separate share placement plan, alongside a rights issue, to raise funds for restructuring and working capital needs through a partnership with private equity fund, Hildrics Asia Growth Fund VCC.

In January, it received a S$200,000 payment demand, adding to a growing list of payment demands it has received throughout 2025. This was from solicitors representing Ace Financial Services, a Singapore-based accounting firm, in relation to alleged non-payment of the S$200,000 sum and interest and legal costs.

Proposed placement

The debt-saddled company had on Jul 4, 2025, entered the placement agreement with UOB Kay Hian, the placement agent, as part of &ldquo ongoing efforts to strengthen its financial position and to provide funding for the repayment of the group&rsquo s debts and outstanding liabilities&rdquo .

The failed placement was also meant to improve mm2 Asia&rsquo s cash flow and support its working capital requirements.

Under the scheme, it aimed to procure subscriptions for around 1.9 billion ordinary shares in its share capital, to raise net proceeds of around S$14 million. Of this, S$7.5 million was to be used for the repayment of debts and liabilities, while S$6.5 million would be allocated for general working capital purposes.

The placement price was to be set at either a minimum price of S$0.008 per share, or the volume-weighted average price (VWAP) per ordinary share of the company&rsquo s shares traded on the Singapore Exchange (SGX) over 30 consecutive days before the date shareholders approve the placement.

The minimum placement price represented a premium of around 14.3 per cent to the VWAP of S$0.007 for trades done on the SGX for the full market day on Jul 4, 2025.

If the placement had succeeded, the 1.9 billion placement shares would account for around 22.3 per cent of mm2 Asia&rsquo s enlarged share capital.

Shares of the company last closed at S$0.003 before the counter was suspended on Nov 11, 2025.

|

|

|

|

Good Post

Bad Post

|

|

|

|