|

Latest Posts By Sin_Cos_Tan

- Veteran

|

|

| 11-Jan-2024 17:36 |

Keppel

/

Keppel Corp

|

||||||||||||||||||||||||||||||||

|

|

11 January 2024 Industry leaders collaborate to develop integrated carbon capture, utilisation and sequestration and lower carbon hydrogen value chains Chevron Singapore Pte Ltd, Keppel, Pan-United Corporation, Surbana Jurong, Air Liquide Singapore, Osaka Gas Singapore, and Pavilion Energy (together Parties) have signed a Memorandum of Understanding (MOU) to collaborate on lower carbon opportunities to support Singapore&rsquo s aspiration of achieving net-zero emissions by 2050 https://www.keppel.com/en/media/media-releases-sgx-filings/industry-leaders-collaborate-to-develop-integrated-carbon-capture-utilisation-and-sequestration-and-lower-carbon-hydrogen-value-chains/ |

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 11-Jan-2024 17:20 |

Keppel

/

Keppel Corp

|

||||||||||||||||||||||||||||||||

|

|

IR calendar

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 10-Jan-2024 12:19 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

Now raise their TP to $ 6.91 https://forums.hardwarezone.com.sg/threads/prata-flipping-gif.6444341/#post-131860259

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 10-Jan-2024 10:34 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

See these analysts... like roti prata flipping master " Reduce" and ' ' Sell' calls on SIA by CIMB on 13/11/23 , TP : $5.47 Lol.... https://www.youtube.com/watch?v=-6apiOSs74E

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 07-Jan-2024 16:02 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

Singapore Airlines Passes United Airlines As Largest Boeing 787-10 OperatorSUMMARY

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 05-Jan-2024 11:37 |

DBS

/

DBS

|

||||||||||||||||||||||||||||||||

|

|

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 05-Jan-2024 11:23 |

DBS

/

DBS

|

||||||||||||||||||||||||||||||||

|

|

Looking for Higher Dividends? 4 Singapore Stocks That Look Poised to Pay Out More in 2024 DBS Group (SGX: D05) The blue-chip group reported a stellar set of earnings for the third quarter of 2023 (3Q 2023). For the first nine months of 2023 (9M 2023), total income jumped 27% year on year to S$15.2 billion. DBS paid out an interim dividend of S$0.48, 33% higher than the S$0.36 that was paid out a year ago. There could be higher payouts from the bank this year as interest rates look set to stay higher for longer. During its 2023 Investor Day, DBS communicated that it could increase its dividend by S$0.24 per year as a baseline, barring unforeseen circumstances. DYODD https://sg.finance.yahoo.com/news/looking-higher-dividends-4-singapore-100000383.html |

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 05-Jan-2024 09:49 |

DBS

/

DBS

|

||||||||||||||||||||||||||||||||

|

|

Another one from OCBC Investment Research - 银 行 股 方 面 , 华 侨 银 行 投 资 研 究 ( OCBC Investment Research) 推 荐 星 展 集 团 DBS和 大 华 银 行 UOB, 目 标 价 分 别 为 39元 和 32.50元

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 03-Jan-2024 16:51 |

DBS

/

DBS

|

||||||||||||||||||||||||||||||||

|

|

That said, Koh is also positive on DBS for its excellent execution and consistent good results. " Management estimated surplus capital at $3 billion or $1.20 per share based on optimal operating range for CET-1 CAR of 12.5% - 13.5%, Koh notes. He adds: " DBS could consider potential capital management exercise to return surplus capital to shareholders over three years given that Final Basel III Reforms are already finalised and would be implemented starting July 1." Koh has given DBS and OCBC " buy" calls with respective target prices of $41.65 and $16.85. https://sg.finance.yahoo.com/news/uob-kay-hian-downgrades-singapore-002036858.html |

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 02-Jan-2024 11:51 |

Keppel

/

Keppel Corp

|

||||||||||||||||||||||||||||||||

|

|

KC FINANCIAL CALENDAR

Upcoming events

2H & FY 2023 results announcement : Jan / Feb 2024 *

2H & FY 2022 results announcement : 2 Feb 2023

*Note: Dates are indicative and subject to change.

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 02-Jan-2024 09:01 |

Keppel

/

Keppel Corp

|

||||||||||||||||||||||||||||||||

|

|

Keppel delivers higher shareholder returns in 2023 amid transformation efforts Keppel has delivered total shareholder returns of 61.1 per cent for 2023, on the back of the company' s overhaul to be a global asset manager and operator that is more dynamic and asset-light in nature, said chief executive Loh Chin Hua in a New Year message to employees on Jan 1. The latest annual returns figure was higher than the company' s full-year returns of 49.3 per cent in 2022. Keppel exceeded the upper end of its asset monetisation goal range of $3 billion to $5 billion ahead of its end-2023 target. It also announced a further target of $10 billion to $12 billion in cumulative asset monetisation by end-2026. The group also continued to grow its funds under management, which amounted to more than $53 billion by the first half of 2023. https://www.straitstimes.com/business/keppel-delivers-higher-shareholder-returns-in-2023-amid-transformation-efforts |

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 29-Dec-2023 14:40 |

DBS

/

DBS

|

||||||||||||||||||||||||||||||||

|

|

May see Chinese New Year angpows! Huat arh... CNY-10/2/24 DBS full year announcement - 7/2/24 (4th Qtr dividend +Special dividend) Singapore' s 2024 Budget statement to be delivered in parliament on 16/2/24 (Lawrence Wong distributes Ang Pow) DYODD

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 29-Dec-2023 14:31 |

DBS

/

DBS

|

||||||||||||||||||||||||||||||||

|

|

Events and PresentationsEvent Calendar

My bad... it should be 7/2/24 FY 2022 full yr results was announceed on 13/2/23 https://www.dbs.com/investors/events-and-presentations/default.page

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 29-Dec-2023 10:44 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

重 现 疫 前 水 平 12月 飞 出 国 旅 游 人 次 或 破 百 万 根 据 移 民 与 关 卡 局 数 据 , 从 海 空 两 路 出 国 旅 行 的 居 民 人 数 在 11月 份 已 突 破 百 万 大 关 , 其 中 空 路 出 国 者 接 近 90万 人 , 已 高 于 2019年 和 2018年 同 月 的 人 数 。 https://www.zaobao.com.sg/finance/singapore/story20231228-1458753

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 28-Dec-2023 14:56 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

The answer is written on the wall. Let see her FY 2023-2024 year end results. Another 马 后 炮 ...LOL!

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 18-Dec-2023 09:59 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

NOVEMBER 2023 OPERATING RESULTS In November 2023, strong passenger demand heading into the year-end peak travel season saw the Singapore Airlines (SIA) Group post robust load factors across all route regions. The Group' s passenger traffic grew 17.6% compared to last year, outpacing capacity expansion of 15.1%. Consequently, the Group' s passenger load factor (PLF) saw an uptick of 1.9 percentage points year-on-year to reach 87.8%, with SIA and Scoot posting monthly PLFs of 86.9% and 90.8% respectively. The two airlines carried a combined total of 3.1 million passengers during the month, 28.6% higher than a year before. Cargo operations posted a load factor of 57.9%, or 1.9 percentage points higher year-onyear. Major retail holidays such as Black Friday and Single&rsquo s Day led to increased e-commerce flows, contributing to a rise in cargo loads by 5.8% year-on-year. This outpaced the capacity expansion of 2.2% from a year ago. During the month, SIA resumed services to Chongqing. At the end of November 2023, the Group' s passenger network covered 119 destinations in 35 countries and territories. SIA served 74 destinations, while Scoot served 68 destinations. The cargo network comprised 124 destinations in 37 countries and territories. https://www.singaporeair.com/saar5/pdf/Investor-Relations/Operating-Stats/opstats-nov23.pdf

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 12-Dec-2023 12:09 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

Record 4.7 billion passengers expected in 2024 as airline industry recovers https://www.channelnewsasia.com/business/airline-industry-recovery-2024-record-passengers-post-pandemic-profits-3969631  |

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 12-Dec-2023 11:54 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

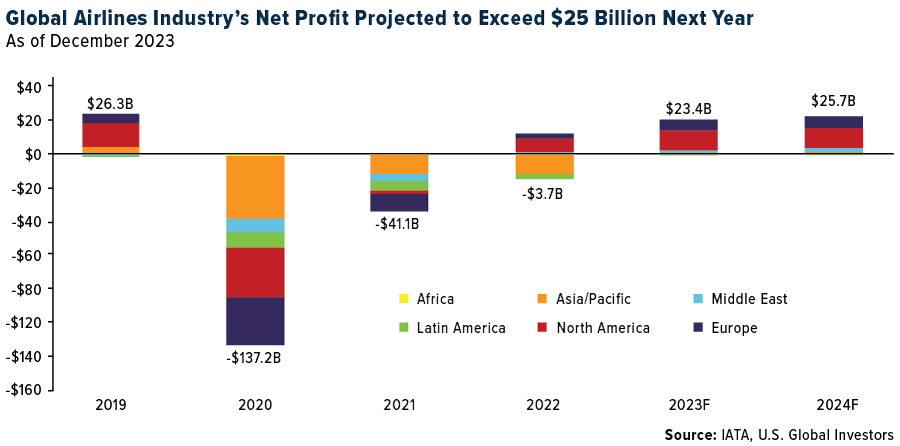

Airlines Set to Earn 2.7% Net Profit Margin on Record Revenues in 2024 https://www.iata.org/en/pressroom/2023-releases/2023-12-06-01/ IATA Forecasts Record Operating Profits in 2024 On a final, encouraging note, the International Air Transport Association (IATA) forecasts net profits of $25.7 billion for the global airline industry in 2024, with operating profits reaching a record $49.3 billion. This projection, coupled with an expected surge in passenger traffic, paints a picture of an industry on the cusp of a historic rebound. IATA 預 測 2024 年 營 運 利 潤 將 創 歷 史 新 高 最 後 令 人 鼓 舞 的 是 , 國 際 航 空 運 輸 協 會 (IATA) 預 測 2024 年 全 球 航 空 業 淨 利 將 達 到 257 億 美 元 , 營 業 利 潤 將 達 到 創 紀 錄 的 493 億 美 元 。 這 項 預 測 , 加 上 預 期 的 客 運 量 激 增 , 描 繪 了 一 個 產 業 正 處 於 歷 史 性 反 彈 的 風 口 浪 尖 的 景 象 。  |

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 23-Nov-2023 11:28 |

DBS

/

DBS

|

||||||||||||||||||||||||||||||||

|

|

由 于 美 国 联 邦 储 备 局 基 本 确 定 不 再 加 息 , 使 得 本 地 银 行 股 连 续 几 天 遭 到 抛 售 。 不 过 , 因 利 率 将 长 期 保 持 高 位 , 这 让 银 行 股 的 股 息 收 益 率 仍 可 达 5.8%至 6%, 吸 引 投 资 者 逢 低 买 入 。 银 河 --联 昌 证 券 ( CGS-CIMB) 市 场 策 略 师 蔡 伟 仁 也 认 为 , 超 跌 反 弹 是 指 数 上 涨 的 主 要 原 因 , 而 美 联 储 停 止 加 息 在 短 期 内 将 继 续 利 好 市 场 。 此 外 , 这 个 月 起 已 进 入 美 国 总 统 选 举 的 最 后 一 年 , 从 历 史 数 据 看 , 同 期 股 市 的 表 现 一 般 会 不 错 。 https://www.zaobao.com.sg/finance/singapore/story20231122-1451739 |

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| 16-Nov-2023 12:38 |

SIA

/

SIA revived

|

||||||||||||||||||||||||||||||||

|

|

SIA paid an interim dividend of 10 cents and final dividend of 28 cents for the FY2022/2023 . Total dividend 38 cents per share. Dividend yield 6.08% based on current price of $6.25 Please note that SIA financial year ended 31/3 DYODD

|

||||||||||||||||||||||||||||||||

| Good Post Bad Post | |||||||||||||||||||||||||||||||||

| First < Newer 301-320 of 688 Older> Last |